Employee reimbursements cover a wide range of everyday business and benefits expenses, including travel, home office support, wellness stipends, and Lifestyle Spending Accounts (LSAs). Understanding how these different reimbursement types work is key to designing a reimbursement program that’s IRS-compliant, scalable, and actually usable.

Reimbursements are a baseline operational function for most organizations, and for companies with large or distributed workforces, managing them accurately and compliantly is no small task. The complexity lies in the details: State laws vary in what employers are legally required to cover, federal tax rules determine which reimbursements are taxable and which are not, and how reimbursement programs are structured — including how stipends are funded, reviewed, and taxed — has real implications for budget control, IRS compliance, and administrative lift.

In this article, we break down seven of the most common types of employee reimbursements, along with key considerations and practical guidance for each.

What is an employee reimbursement?

An employee reimbursement is the process by which an organization repays employees for out-of-pocket expenses, whether for business needs or employer-sponsored benefits. The employee pays upfront and submits documentation, and the organization reimburses them afterward.

This structure applies across business expense reimbursements, stipend programs such as wellness wallets and professional development accounts, and LSAs. In each case, employees submit eligible expenses, those expenses are reviewed against company policy, and approved reimbursements are included in payroll.

When structured under an accountable plan that meets IRS requirements, reimbursements are generally not considered taxable income. To qualify, the expense must serve a legitimate business or policy-defined purpose and be backed with proof such as a receipt or invoice, and any excess reimbursement must be returned to the employer within a reasonable timeframe. Each reimbursed expense creates a documented audit trail, including receipts, approval history, and tax treatment.

Examples of reimbursements include:

- Business travel costs (e.g., flights, rental cars, hotel accommodations)

- Meal expenses during business trips or company events

- Work equipment, supplies, or project materials

- Home office equipment

- Incidental expenses such as parking fees or tolls

- Lifestyle benefits, including stipends and LSAs

It’s also helpful to distinguish between how reimbursements are structured vs. how they’re funded:

- A reimbursement is the mechanism. An employee makes a purchase, submits documentation, and is repaid according to company policy.

- A stipend refers to how reimbursement funds are allocated. A stipend is a defined budget offered on a monthly, quarterly, annual, or one-time basis for a benefit like wellness, learning, remote work, food, or even peer-to-peer recognition.

Modern stipend programs — including lifestyle benefits such as LSAs, wellness wallets, and professional development accounts — are reimbursement-based. Employees spend within the stipend budget they’ve been given, upload receipts, and receive reimbursement through payroll after approval. This eliminates prefunding, reduces unused spend, and ensures each reimbursement is reviewed against policy and processed with the appropriate tax treatment before payment.

Do employee expense reimbursements count as taxable income?

Reimbursements are not inherently taxable or nontaxable. The tax treatment depends on the type of expense being reimbursed and how the program is structured.

When reimbursements are paid under a compliant accountable plan and meet IRS requirements, they are generally not considered taxable income. This most often applies to reimbursements for business travel, commuter benefits, and certain professional development costs.

However, many of today’s most popular employee benefits — including support for wellness, food, and family needs — fall outside IRS-qualified exclusions. Reimbursements in these categories are typically treated as taxable wages, even though they are delivered through the same reimbursement process.

This is where things become complex for HR and Finance teams. Tax treatment is determined at the expense level, not simply by the name of the program. A single reimbursement program, such as a LSA, may include both taxable and nontaxable reimbursements across different stipends, each requiring different handling for payroll and reporting.

Without a structured system in place, tracking expenses, applying the correct tax treatment, and preparing payroll reporting can quickly become manual and time-consuming. Modern reimbursement platforms handle this automatically by applying the correct tax treatment based on your policy and the expense submitted and generating payroll-ready reports for each cycle.

Want to see for yourself? Request a demo of Compt.

What’s an ‘accountable plan’?

An accountable plan is an IRS-established framework for reimbursements and expense allowances that satisfies all three of the following conditions:

- The expenses must be incurred in connection with services performed as an employee.

- Employees must provide substantiation of the expenses (e.g., with receipts or other documentation) within a reasonable period (typically 60 days).

- Employees must return any excess reimbursement or allowance within a reasonable period (typically 120 days).

Substantiation typically takes the form of receipts, invoices, or other documentation that proves the expense was incurred and is in accordance with company policy. If these requirements are not met, the plan is considered “nonaccountable,” and reimbursements are treated as taxable wages subject to payroll taxes.

Offer compliant, personalized reimbursements through Compt.

Learn more about how to deliver flexible employee reimbursements to your people.

Let’s dig into some specific types of employee reimbursements. Together, these reimbursement types form the foundation of modern benefits programs, helping organizations balance flexibility, compliance, and cost control.

1. Business travel reimbursements

Most organizations are familiar with a per diem travel allowance. This is a daily allowance for all your employees’ meals, lodging, and incidental expenses while traveling for business. These expenses can be reimbursed either by actual receipt or through a per diem structure, with tax treatment tied to the federal government’s per diem rules.

For reference, in 2026, the standard CONUS (continental U.S.) rate is $178 per day ($110 lodging, $68 meals/incidentals). The General Services Administration (GSA) updates these rates every October, and they differ by location and time of year (high and low season).

If employees do not exceed standard per diem rates, those reimbursements are generally not treated as taxable income. Any amounts paid above the allowable rates may need to be reported as wages and subject to payroll taxes.

Per diems also simplify substantiation requirements. Instead of tracking every individual expense, employees typically do not need to submit receipts for meals and lodging up to the per diem limit, though they may still need to document the time, place, and business purpose of the trip.

A reimbursement platform such as Compt automates business expense workflows, including per diem reimbursements, so HR and Finance are not left to reconcile them manually.

2. Meals and entertainment

The rules for tax treatment of meals and entertainment expenses differ depending on the nature of the expense.

- Business meals: Business meals are 50% deductible for federal income tax purposes, provided the meal has a clear and documentable business purpose. It’s worth noting that while your organization may only deduct 50% of the cost, you may still reimburse employees in full, and doing so is generally considered best practice.

- Client entertainment: Under rules established by the Tax Cuts and Jobs Act (TCJA), entertainment expenses are no longer deductible, regardless of business intent. This includes tickets to sporting events, concerts, golf outings, and the like, even when the explicit purpose is client relationship-building.

- Employee retreats, incentive travel, and performance experiences: Corporate retreats, team off-sites, and performance-based travel programs occupy a more nuanced position in the tax code. When these events are primarily business in purpose (meaning the agenda includes substantive work-related activities, meetings, or training), associated expenses are subject to the standard 50% limitation on meals. However, excursions or recreational activities included in a retreat itinerary are generally not deductible under current law, even if attendance is limited to employees.

The IRS requires strict documentation to substantiate any meal or entertainment expense, so it’s important to maintain expense reports that reflect this level of detail.

For example, if your organization flies a team to an annual sales kickoff and the agenda includes structured business sessions, you may deduct qualifying transportation and lodging costs and 50% of meal costs, provided the expenses are properly documented. Optional excursions added to the itinerary, however, would not qualify for deduction.

On the other hand, if a sales representative takes a prospective client to dinner, the employer should reimburse the full cost. Still, only 50% of that meal expense is deductible on your corporate return.

3. Medical expenses

With Mercer reporting that total health benefit costs per employee rose 6% in 2025 and are projected to rise another 6.7% (or more) in 2026, many organizations are looking for ways to support employee health without adding significant cost or administrative complexity to their core medical plans.

Rather than relying solely on a traditional group health plan, one option is to layer in reimbursement-based programs such as Medical Expense Reimbursement Plans (MERPs) alongside health and wellness stipends. These approaches allow companies to support different types of health-related expenses while maintaining control over budget and compliance.

MERPs are designed specifically for qualified medical expenses and operate under strict IRS and ERISA requirements. The most widely used form of MERP is a Health Reimbursement Arrangement (HRA), an employer-funded benefit that reimburses employees for eligible medical costs such as premiums, deductibles, and copays. HRA reimbursements are nontaxable to employees when used for qualifying expenses as defined under IRS Publication 502.

There are four primary HRA structures:

- Qualified small employer HRA (QSEHRA): Available to employers with fewer than 50 employees. Reimbursements are nontaxable for qualifying expenses. For 2026, contribution limits are $6,350 for self-only coverage and $12,800 for family coverage.

- Excepted benefit HRA (EBHRA): Available to employers that already offer a group health plan. This structure reimburses expenses not covered by that plan, such as vision or dental. The 2026 contribution limit is $2,150.

- Individual coverage HRA (ICHRA): Allows employers to vary reimbursement amounts by employee class (e.g., full-time vs. part-time), with no contribution cap. Employees use reimbursements to fund individual health insurance premiums.

- Group coverage HRA (GCHRA): Supplements an existing group health plan by reimbursing out-of-pocket costs not covered by the plan, helping offset high deductibles.

All HRA types are subject to ERISA, which requires employers to provide plan documentation such as a Summary Plan Description, annual notices, and other disclosures mandated by the Department of Labor. ICHRA plans also require employees to receive notice at least 90 days before the start of the plan year.

While these medical reimbursement programs are tied to IRS-defined qualified expenses and regulatory requirements, wellness stipends and LSAs operate differently. While still reimbursement-based, they are designed to cover broader, nonqualified wellness expenses outside of IRS medical definitions.

These stipends may include expenses such as gym memberships, mental health apps, fitness programs, nutrition services, wearable fitness devices, and other everyday wellness costs that support employee well-being but do not qualify for tax-free treatment under a medical plan.

As a result, most reimbursements through a wellness stipend or LSA are taxable by default, even if the expense feels health-related. Employers use this structure to support costs that fall outside traditional medical coverage, including areas like weight management programs or GLP-1 medications, while maintaining a predictable budget and avoiding the regulatory complexity associated with expanding a health plan.

These two approaches are complementary. Medical reimbursement plans handle qualified healthcare expenses under strict regulatory frameworks, while stipends and LSAs provide flexible, reimbursement-based support for broader employee well-being needs.

4. Parking reimbursements and commuter benefits

Americans, on average, spend nearly an hour (54.4 minutes) traveling to and from work each day, according to U.S. Census Bureau data. Luckily for HR and Finance, parking reimbursements and commuter benefits are among the more straightforward employee reimbursements available. Eligible expenses include:

- Parking fees at or near the workplace

- Metered or timed street parking incurred during work-related travel

- Parking at a temporary job site away from the employee’s regular workplace

According to IRS Publication 15-B, employers may provide up to $340 per month in parking benefits on a tax-free basis in 2026.

Employers may also reimburse commuting costs associated with travel by car, bus, train, ferry, or vanpool. Mass transit passes and commuter highway vehicles are subject to a separate monthly exclusion limit of $340 per month for 2026. It’s important to note that these are two distinct exclusions; each limit applies only to its designated expense category and cannot be combined or applied interchangeably.

4. Tuition and student loan reimbursement

While not a traditional business expense, tuition reimbursement and student loan repayment assistance are among the most valued benefits an employer can offer. Plus, both carry meaningful tax advantages for organizations and employees alike.

Under IRC §127, employers may provide up to $5,250 in tax-free educational assistance per employee annually. This limit is cumulative and applies across all qualifying education benefits, including student loan repayment contributions, so organizations offering both should monitor combined totals carefully.

A few key considerations:

- Where education is a condition of employment, such as for required certifications or mandatory continuing education, reimbursements qualify as a working condition fringe benefit, deductible as an ordinary business expense and not subject to the §127 cap.

- Amounts exceeding $5,250 annually are generally treated as taxable compensation to the employee.

- The §127 exclusion is a permanent provision of the tax code with no current sunset date.

An LSA with Compt can support both taxable and nontaxable education-related reimbursements, including tuition reimbursement and student loan repayment, and ensure each is accounted for correctly. Many organizations offer these through a professional development stipend, which gives employees flexibility while keeping reimbursement and tax treatment in one system.

Benchmarking data shows that all-inclusive LSAs led with 89% utilization, outperforming standalone wellness (70%), professional development (40%), and caregiving (46%) stipends. For HR and finance leaders, strategically layering nontaxable categories like student loan repayment alongside broader lifestyle benefit programs is an effective way to balance participation, cost, and compliance.

6. Cell phone reimbursements

According to Compt customer benchmarking data, cell phone reimbursements are among the top five stipends, with 15% of companies today offering them. Plus, in certain states such as California, Illinois, Iowa, and Massachusetts, reimbursing employees for work-related cell phone use is a legal requirement.

Even where not legally mandated, cell phone reimbursement is a low-overhead benefit with genuine appeal to employees. Employers may structure cell phone benefits in one of two ways:

- A fixed monthly cell phone stipend for employees who use personal devices for work

- Reimbursement of actual expenses based on documented business use

In either case, reimbursements are generally nontaxable when they are tied to legitimate business use and structured appropriately.

7. Lifestyle Spending Account: combine multiple stipends into one reimbursement system

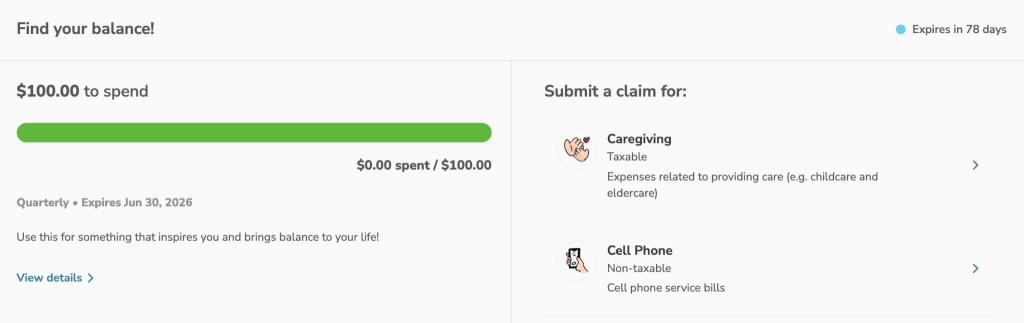

An LSA is a reimbursement-based benefits program that allows employers to offer multiple stipends through a single, centralized system. Instead of managing separate programs for wellness, professional development, food, remote work, or any number of other benefits, companies can bundle those stipends into one flexible benefit.

Each stipend within an LSA has its own budget, eligibility rules, and tax treatment, but all operate through the same reimbursement process. Employees pay out of pocket, submit receipts for eligible expenses, and are reimbursed through payroll after approval.

This structure allows employers to support a wide range of employee needs while maintaining consistency in how reimbursements are reviewed, tracked, and reported. It also gives HR and Finance teams a single system of record for participation, spend, and compliance.

Because LSAs are structured as taxable lifestyle benefits rather than medical plans, they typically fall outside of ERISA requirements. This makes them significantly easier to administer than traditional health benefits while still allowing employers to offer support across multiple areas of employee well-being.

LSAs are often used to consolidate benefits that would otherwise be offered separately. For example, instead of managing individual programs for wellness, learning and development, and remote work, an employer can offer those as separate stipends within one LSA.

This model is now the most common approach to lifestyle benefits. In Compt’s 2026 Annual Lifestyle Benefits Benchmark Report, 64% of employers offered an all-inclusive LSA as their primary benefits program, reflecting a broader shift toward flexible, reimbursement-based benefit design.

What are the most common stipends offered through an LSA?

The following are some of the most common stipends employers include within an LSA. Each represents a distinct type of reimbursement, with its own eligibility rules and tax treatment — but performance and engagement are best understood in the context of how these stipends function within a broader LSA.

Wellness

Wellness is one of the most consistently included stipends within LSAs and one of the strongest drivers of participation. When delivered as part of an LSA, wellness stipend utilization reaches 86%, compared to 62% as a standalone stipend — a clear indication that flexible, multistipend structures drive higher engagement.

These reimbursements typically cover fitness memberships, mental health support, nutrition programs, and general well-being expenses. Because most of these do not qualify as medical expenses under IRS rules, they are usually taxable.

Within LSAs, wellness works less like a narrow benefit and more like a flexible support layer that employees can use alongside other needs, which is why it performs best when embedded rather than isolated.

Professional development

Professional development is commonly included within LSAs, but how employees use it has shifted significantly. In 2025, 20% of professional development expenses were AI-related, with a large share going toward tools and productivity software rather than more traditional conferences.

This reflects a broader shift toward continuous, self-directed learning that fits naturally within an LSA structure. Rather than relying on one-time training events, employees use stipends dynamically alongside other priorities, drawing on funds when learning needs arise.

Depending on how the program is structured, some expenses may qualify as nontaxable, but many are treated as taxable reimbursements.

Remote work and home office equipment

Remote work and office equipment stipends are frequently included within LSAs as part of a baseline set of support for distributed teams. Participation in these reimbursements is consistently high, with office equipment reaching 84% participation among employees with access.

These stipends help employees cover the cost of home office setups, including desks, chairs, monitors, and internet expenses. Some items may qualify as business expense reimbursements depending on policy design, but many are reimbursed as taxable benefits.

Within an LSA, these stipends function as foundational infrastructure, ensuring employees can work effectively while still allowing flexibility to allocate remaining funds across other priorities.

Offer a no-hassle remote work stipend to your team

Reach a global or distributed workforce with flexible, automated remote work stipends in one platform. Leave the admin work to us.

Food and groceries

Food stipends are a strong example of how employee behavior within LSAs differs from what employers offer as standalone programs. While only a small percentage of companies offer a dedicated food stipend, employee spending within LSAs tells a different story:

Nearly 1 in 10 stipend dollars is now spent at grocery retailers, reflecting a shift toward benefits that help offset everyday cost-of-living pressures.

Within an LSA, food is not treated as a standalone benefit but as part of a broader mix of support. Employees use it alongside wellness, family, and household expenses, reinforcing that flexible structures better align with real-world financial needs.

Caregiving and family

Caregiving and family-related stipends are among the clearest examples of how LSAs align benefits with real employee needs. While these stipends are less commonly offered as standalone programs, they see meaningful usage within LSAs, where employees can apply funds toward childcare, elder care, fertility support, and other family-related expenses.

This type of support is difficult to deliver through traditional benefits structures, which are often limited to specific use cases or heavily regulated programs. Within an LSA, however, caregiving and family stipends provide flexible, reimbursement-based support that adapts to different life stages and personal circumstances.

Because these expenses fall outside most IRS-qualified benefit categories, reimbursements are typically taxable. Even so, they are highly valued by employees, particularly as caregiving responsibilities continue to be a major factor in retention and workforce participation.

Setting up your employee reimbursement policy

A well-structured reimbursement program doesn’t have to be complicated to administer. Start with the following steps:

- Define the reimbursement types you want to offer and the stipends attached to them.

Each stipend should define what employees can spend on, how expenses are reviewed, and how reimbursements are treated for tax and reporting purposes.

- Document your policy in writing.

Cover eligible expenses, submission requirements, timelines, and spending limits, and include it in your handbook so expectations are clear from day one. The Compt platform enables you to share an employee-facing version right inside your stipend description.

- Establish a consistent funding cadence for each stipend.

Cadence directly affects utilization. Compt data suggests quarterly funded programs reach 85% utilization vs. 52% for monthly, a difference worth considering when designing your program.

- Choose the right platform.

Manual processes create burden and compliance risk. Compt centralizes submissions, applies the appropriate tax treatment to each reimbursement based on your policy, routes approvals, and generates payroll-ready outputs automatically.

- Communicate clearly and consistently.

Employees use benefits they understand. Within your intranet and internal comms, explain how to submit expenses, when to expect reimbursement, and where to get help when needed.

Learn how to set up an employee stipend program in one hour using Compt.

Deliver tax-compliant employee reimbursements with Compt.

With Compt, setting up employee reimbursements is simple. Choose stipends, assign amounts and cadences, and define what each one covers. Once approved, the reimbursements are automatically included in payroll, and employees will see them on their next paycheck.

Further, the platform automatically tracks and organizes submitted expenses and generates payroll-ready reports, giving Finance a complete record for tax and compliance purposes.

Request a demo to see how Compt works.

FAQs: Employee reimbursements

Employee reimbursement is the process by which an organization repays employees for out-of-pocket expenses incurred for business needs or employer-sponsored benefits.

The employee pays upfront, submits documentation, and the employer reimburses them, typically through payroll or a dedicated reimbursement platform.

When structured under a compliant accountable plan that meets IRS requirements, reimbursements are generally not considered taxable income. To qualify, the expense must serve a legitimate business purpose, be adequately substantiated, and any excess reimbursement must be returned within a reasonable timeframe.

Common reimbursable expenses include business travel, meals, work equipment, home office setup, and commuting costs. Many organizations also reimburse lifestyle and wellness expenses through employee stipends or Lifestyle Spending Accounts (LSAs). Both are reimbursement-based models that give employees flexibility within employer-defined stipend rules.

Are employee reimbursements taxable income?

Generally, no, but the answer depends on how the reimbursement is structured.

When paid under a compliant accountable plan, reimbursements are not considered taxable income and are not subject to payroll taxes. When a reimbursement falls outside an accountable plan or lacks proper documentation, it may be treated as taxable wages.

It is also worth separating reimbursement structure from tax treatment. Business travel, qualifying medical expenses, and commuter benefits can be tax-free when administered correctly.

Lifestyle and wellness reimbursements, including those delivered through a stipend or Lifestyle Spending Account (LSA), are typically taxable by default because they fall outside IRS-qualified expense categories.

Compt automatically applies the correct tax treatment across both taxable and nontaxable reimbursements in alignment with your company policy, reducing manual work for HR and Finance teams.

What is an accountable plan, and why does it matter for reimbursements?

An accountable plan is an IRS-established framework that governs whether employer reimbursements qualify for tax-exempt status. It matters because the distinction between a compliant and noncompliant reimbursement program has direct payroll tax consequences.

To qualify, three conditions must be met. The expense must be incurred in connection with services performed as an employee. The employee must substantiate the expense within a reasonable period, generally 60 days. And any excess reimbursement must be returned to the employer within a reasonable period, generally 120 days.

When these conditions are met, reimbursements are excluded from taxable income. When they are not, payments are treated as wages subject to withholding and payroll taxes. Building a compliant reimbursement program starts with understanding this framework.

What types of employee reimbursements are tax-free vs. taxable?

It is important to separate eligibility from tax treatment. Eligibility is a policy decision about what the employer allows under each reimbursement type or stipend.

Reimbursements that are generally tax-free include business travel expenses reimbursed under an accountable plan, qualifying medical expenses reimbursed through a compliant HRA, meals during business travel up to applicable limits, and commuter benefits within IRS monthly limits.

Reimbursements that are generally taxable include wellness and lifestyle expenses delivered through a stipend or Lifestyle Spending Account (LSA), entertainment expenses — which are no longer deductible under the Tax Cuts and Jobs Act — and any reimbursements made outside of a compliant accountable plan.

Compt’s platform automatically applies the correct tax treatment at the expense level across both taxable and nontaxable reimbursements. For a deeper breakdown, see our guide to reimbursement compliance.

How should companies set up an employee reimbursement policy?

A well-structured reimbursement policy gives employees clarity and gives Finance control. Most effective programs are built around five decisions.

First, define the reimbursement types and stipends you want to offer: what will and will not be reimbursed, including business travel, home office equipment, wellness, and professional development.

Second, determine how those stipends are funded (e.g., recurring budgets or one-time allocations). In modern reimbursement programs — including Lifestyle Spending Accounts (LSAs) — these stipends are all delivered through the same reimbursement model.

Third, establish documentation and submission requirements that satisfy accountable plan rules.

Fourth, set a reimbursement cadence; funding frequency directly affects utilization. Compt benchmark data shows quarterly funded programs achieve 85% utilization compared to 52% for monthly programs.

Fifth, select a platform. Reimbursement software like Compt supports out-of-pocket purchases, automates approvals, applies the correct tax treatment, and integrates directly with payroll for fast, accurate reimbursement cycles.

Once the program is designed, document it in writing and incorporate it into your employee handbook. For a step-by-step walkthrough, see our guide on how to set up an employee reimbursement program.

What’s the difference between reimbursements and stipends for employee benefits?

A reimbursement is the process: employees spend, submit receipts, and are repaid.

A stipend is the budget: a set amount an employer makes available for a benefit like wellness, professional development, remote work, or food.

In modern benefits programs, stipends are delivered through a reimbursement model. Employees spend within the stipend they have been given, submit receipts, and are reimbursed through payroll, with tax treatment applied based on the expense itself.

How do reimbursement stipends compare to card-based stipend platforms?

Reimbursement stipends and card-based stipend platforms differ primarily in how funds are delivered and controlled.

Reimbursement stipends operate on a spend-first model. Employees pay out of pocket, submit receipts, and are reimbursed after approval. This ensures every expense is reviewed against policy, tax treatment is applied correctly, and employers only pay for what is actually used.

Card-based platforms, by contrast, require employers to preload funds onto a debit card. This can create challenges with unused balances, declined transactions, and limited visibility into how funds are spent in real time.

For most organizations, reimbursement-based stipends provide stronger compliance, better cost control, and more predictable reporting, while still giving employees flexibility across eligible expenses.

What reimbursement model is best for a distributed workforce?

The most effective reimbursement model for a distributed workforce is a reimbursement-first system built around flexible stipends, often delivered through a Lifestyle Spending Account (LSA).

In distributed teams, employees have different needs based on location, role, and personal circumstances. A reimbursement-based model allows employees to spend on what is most relevant to them, whether that’s home office equipment, wellness, food, or caregiving, while staying within employer-defined guidelines.

Because reimbursements are submitted and processed centrally, this model also ensures consistent policy enforcement, tax treatment, and payroll reporting across geographies.

Compared to fixed perks or location-specific benefits, reimbursement-based stipends provide the flexibility, scalability, and administrative consistency required to support a distributed workforce.

I need employee benefits software that supports out-of-pocket purchases first and quick reimbursement. What tools should I shortlist?

You should look for employee benefits software built around a reimbursement-first model that supports out-of-pocket purchases and fast reimbursement through payroll. In this model, employees pay upfront, submit receipts, and receive reimbursement after approval, which keeps spending aligned with IRS and company policy and eliminates the need to preload funds.

The most effective platforms automate the full workflow, including expense submission, approval routing, tax treatment, and payroll integration, so reimbursements can be processed quickly and accurately. They also support multiple stipends within a single system, allowing employers to manage wellness, professional development, food, and other benefits in one place.

Platforms designed specifically for reimbursement-based benefits, such as Compt, are built for this approach. They provide the speed employees expect while giving HR and Finance teams visibility, compliance support, and control over spend, without the inefficiencies of prepaid or card-based models.

Editor’s note: Originally published in 2024, this post has been recently updated for clarity and relevance for our readers.

Editor’s note: Compt software supports the categorization and proper reporting of benefits according to IRS guidelines, helping businesses maintain compliance. However, Compt cannot provide tax advice, and users should consult their own tax, legal, and accounting advisors when necessary.