Healthcare costs are rising at their fastest pace in over a decade, and GLP-1 medications are sitting at the center of that pressure. Employees want support. CFOs want predictability. A weight management stipend threads that needle, but only if you structure it correctly.

Most employers who try to solve weight management either pick a single vendor or explore direct partnerships with pharmaceutical manufacturers. Both approaches can work, but they limit flexibility and can introduce cost and access tradeoffs for employees.

A reimbursement stipend inverts that: you set the budget and rules, and employees choose the approach that works for them.

The right structure depends on your budget predictability needs, how targeted you want the program to be, and how much administrative complexity your team can absorb. There are three core approaches, and the rest of this guide helps you choose the right one and build it.

Quick recap: 3 ways to structure a weight management stipend

There are three ways to support your employees’ metabolic health benefits without adding a new health plan. We covered them in detail in our guide to GLP-1 weight-loss coverage with LSAs and stipends.

Here’s the long and the short of it:

1. Lifestyle Spending Account (LSA)

An LSA is the broadest option. Employees get a flexible allowance across multiple spending categories and can apply it toward weight management expenses, including GLP-1 medications. This is the best option if you want one program to cover everyone’s individual needs.

2. Wellness stipend

Wellness stipends use the same reimbursement model but with a narrower scope. Eligible expenses are limited to health and wellness — e.g., fitness, nutrition, GLP-1 costs, mental health apps. As a result, they tend to have lower utilization compared to LSAs.

3. Weight management stipend

This is the most targeted structure. It only includes expenses that are specific to weight management, like GLP-1s, nutrition coaching, metabolic health programs, and fitness. It sends a clear signal about program intent, but requires more careful category design before launch.

Across all three approaches, the key difference is how the benefit is structured. Most companies are deciding whether to use a reimbursement framework (like Compt stipends/LSAs) or introduce a formal health benefit; the latter carries very different compliance implications.

How to choose the right weight management program structure

The decision comes first. And again, it comes down to three variables: how broad you want the benefit to be, how much compliance exposure you’re willing to take on, and what your per-employee budget actually allows.

The table below maps those variables to the right structure:

| Which benefit structure is best for your weight management program? | |||

|---|---|---|---|

| If you need… | Choose this approach | Why it works | Tradeoffs |

| Max flexibility across multiple categories | Lifestyle Spending Account (LSA) | One allowance covers weight management alongside wellness, food, family, and more | Weight management is one of many categories, not the core focus |

| A benefit that prioritizes wellness broadly, not just weight | Wellness stipend | Scoped to health and wellness expenses across the board w/ weight management as part of a bigger wellness commitment | Weight management doesn’t stand out as the headline |

| A visible, targeted commitment to metabolic health | Weight management stipend | Purpose-built eligible expenses; unambiguous program intent | Requires more careful category design; benefits counsel review recommended |

| Cost predictability above everything else | Any of the above w/ quarterly funding and hard caps | Total program cost is known before approving any reimbursements | Employees cover some costs out of pocket |

What Compt recommends

The best strategy for most companies is to start with an LSA or wellness stipend program. This gives you a controlled framework to support GLP-1 expenses without introducing a new benefits system. Both structures support GLP-1 costs today, are handled within Compt’s existing stipend compliance framework, and can be launched in about an hour on Compt.

Of the two, our benchmarking data tells us the LSA structure is what sees the highest participation. 64% of Compt customers offer an all-inclusive LSA and wellness utilization reaches 86% when embedded within one, versus just 62% as a standalone stipend.

The main concern is visibility. Consolidation limits how loudly you can communicate weight management as a standalone commitment. If you want to send a specific, named signal about metabolic health or GLP-1 support, an LSA does the job functionally but doesn’t do it loudly.

A weight management stipend sits closer to the line between lifestyle reimbursement and regulated health benefit than either of the other two options, simply because the eligible expenses are so closely tied to health outcomes.

This doesn’t mean it’s off-limits, but it does mean the category list needs to be reviewed by benefits counsel before you go live.

NOTE: LSAs and stipends are NOT designed to replace prescription drug coverage or function as a formal health benefit. If your goal is to reimburse GLP-1 prescription costs through a dedicated health benefit structure, contact our team directly to discuss your options.

5 steps to design a weight management stipend (step-by-step)

Now, let’s look at how to build a weight management stipend program that’s usable to employees while also being defensible to Finance and straightforward for your HR team to administer:

- Decide on your structure.

If you’re adding weight management to an existing LSA, the setup decision is simple: enable it as an eligible category within your LSA/stipend software.

If instead you’re building a standalone wellness or weight management stipend, you’ll configure it as its own program in Compt with its own allowance amount and funding cadence. This gives you a clean communication story but requires a separate launch.

Neither path is complicated, but you want the configuration to match the decision you already made above. - Define what’s eligible.

Weight management stipends cover expenses across four areas: fitness and movement (gym memberships, fitness programs, personal training), nutrition support (OTC supplements, meal planning, nutrition apps), metabolic health programs, and GLP-1 medications.

Then, some things are generally not eligible. The most important guardrail is how you handle qualified medical expenses, many of which can already be paid for with an HSA or FSA. Your policy should clearly distinguish what is covered by the stipend vs. what should be handled through existing health benefits.

Some nonmedical weight loss treatments, like liposuction or CoolSculpting, are also typically excluded. Expenses that fall outside of weight management entirely, such as workout clothing, are another common example.

Just as important is specificity. Define what’s eligible explicitly in your policy, because vague descriptions put your team in the position of making personal judgment calls on every reimbursement request. Not to mention, specifying what is and isn’t allowed up front saves HR from repeated questions from employees later on.

And for GLP-1 medications specifically, make sure your policy language is clear that this is a taxable lifestyle reimbursement, not prescription drug coverage. That distinction is what keeps the program outside the scope of a regulated health benefit.

Pro tip: Within Compt, you can add a list of vendors (e.g., Weight Watchers, Noom, Ro, GoodRx, Sesame, etc.) that are always allowed, as well as a list of those that aren’t. - Set your budget and spending caps.

Start with a per-employee allowance using market data as your anchor. Using Compt’s 2026 wellness stipend insights as a benchmark, the median amount offered for a wellness stipend was $735 per employee per year in 2025. At 100 employees, that’d be $73,500 in total potential spend.

What Finance teams love about Compt specifically is its stipend reimbursement model. Unlike prefunded accounts (where employers disburse the stipend and absorb whatever employees don’t spend), you pay afterward for expense submissions, up to the spending limit you’ve set.

One advantage of a reimbursement model is that you can also control how the budget is made available over time. Using an annual stipend as an example, you can structure access as monthly, quarterly, or semi-annual accrual, depending on how you want employees to use the benefit.

If the goal is to support larger expenses, monthly or quarterly accrual allows funds to build up over time within the year. Any unused balance can continue to roll over during that period, but carrying funds into a new year typically requires reissuing that balance separately.

And for larger expenses like GLP-1 meds, it lets you build partial reimbursement logic into the policy. So, you could set a fixed cap below the actual cost — reimburse $150 of a $1,000 expense, for example.

That way, employees still get support but your program isn’t absorbing open-ended pharmaceutical costs. - Define reimbursement rules.

Most of this is configured once in Compt and then runs automatically. Employees submit receipts through the platform, your team reviews and approves, and reimbursements flow through payroll. You won’t need to manually track and record everything.

The two things you will want to nail down upfront are receipt requirements and payroll cadence.

For receipts, what counts as valid documentation? Itemized receipts displaying the expense type, vendor, and total amount are the standard.

For payroll, decide how frequently reimbursements are processed. Most companies reimburse employees in line with payroll cycles or on a monthly cadence.

Separately, you’ll decide how the stipend itself is funded: monthly, quarterly, or annually. Many employers choose quarterly funding because it supports strong utilization while giving Finance predictable reporting windows.

As for tax handling, it’s automatic. Weight management stipend reimbursements are treated as taxable income, which Compt classifies and reports at the transaction level. - Plan stipend communication and drive adoption.

Benefits participation is your most important KPI, and more often than not, low adoption is an awareness problem. WTW studied benefits satisfaction and found that dissatisfaction is most prevalent where benefits are “under-communicated or not well explained.”

The fix is simple: communicate the benefit in plain language, early and often, with concrete examples of what employees can (and can’t) use it for.

Launch it with a companywide announcement, then set up an email reminder in your benefits platform for anyone who hasn’t enrolled after the first week. Compt’s platform tracks participation in real time, and can automatically send targeted reminder emails to employees who haven’t used their stipend, so if adoption is lagging, you’ll know early and can act without manually following up.

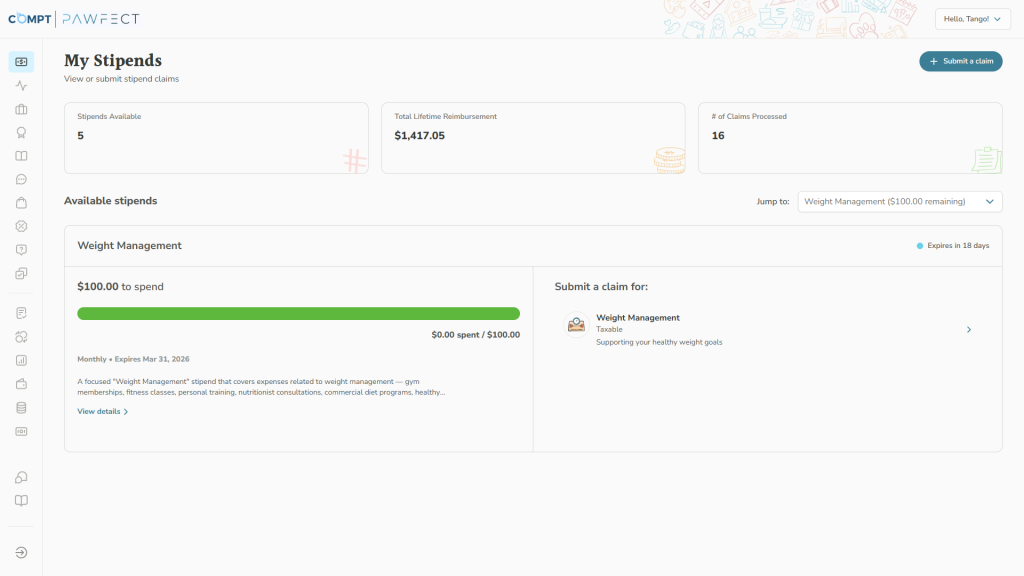

And here’s what it looks like once built:

How to control costs while offering real weight management support

With employer healthcare costs projected to rise 9.5% in 2026, adding a new benefit has to come with a credible cost-control story. A weight management stipend delivered through Compt gives you four levers:

1. Capped allowances vs. open-ended claims

This is the big one. Research from Peterson-KFF shows that a significant number of employers who initially covered GLP-1 drugs for weight loss through their health plan have since restricted or removed it because the costs were unsustainable (59% say they were higher than expected).

Once you cover something through a health plan, removing it is politically messy. Employees who were relying on it lose access mid-treatment, which creates real hardship for them and huge problems from an employee-relations standpoint.

Stipends prevent this. Unlike health plans where a surge in GLP-1 claims could blow your pharmacy budget mid-year, they cap exposure at the allowance amount. HR knows the total cost before the enrollment period even begins, which is exactly what Finance needs to say yes.

2. Pay-for-utilization vs. prefunding

In prefunded accounts, employers absorb everything that doesn’t get used. Compt’s reimbursement model means you only pay when employees submit expenses. So if you budget $50,000 but have 80% utilization, the benefit realistically costs closer to $40,000.

3. Partial reimbursement strategies

For high-cost expenses like GLP-1s, you don’t have to cover the full amount to make a genuine impact. Reimbursing $200 of a $1,000 expense still provides support while keeping program spend predictable and within the overall budget.

4. Strategic benefits consolidation

Adding a weight management benefit doesn’t have to mean adding a new line item. Companies under pressure to cut benefits programs fold “weight management” into an LSA or wellness stipend as an eligible category. Employees who don’t need it simply choose to spend their allowance elsewhere.

Common mistakes when launching a weight management stipend

You’ve made it this far. You’ve got everything sorted from a Finance standpoint and they’re on board. But you still have execution to worry about, and that’s equally important because getting it wrong creates tons of work for your admin team and poses a potential compliance risk.

As far as mistakes to avoid, four come to mind:

1. Over-indexing on GLP-1 only

As an employer, you can use a taxable stipend to help cover GLP-1 copays and deductibles (and that’s mainly what’s driving the conversation). But a benefit scoped exclusively to one drug category feels medicalized, narrows your eligible population, and moves the program closer to a formal health benefit.

That introduces compliance risk. If a stipend is tightly tied to a specific medication or treatment, it can start to resemble a group health or pharmacy benefit, which may trigger ERISA, ACA, HIPAA, COBRA, and other requirements.

The way you avoid that is by keeping the language and admin clearly within reimbursement territory: employees submit receipts and get reimbursed up to their allowance, end of story.

This stronger design includes GLP-1 costs as one eligible expense within a broader weight management or wellness program. Broader scope means higher participation, and higher participation is what keeps the program alive next time your CFO reviews the budget.

2. Not adequately clarifying expense eligibility in your policy

If your eligible expense list says “weight-loss-related expenses,” HR will spend hours approving/denying every ambiguous receipt. And some employees will push the boundaries — e.g., by submitting a standing desk as a weight management expense.

3. Ignoring communication

If people don’t use it, it’s not a benefit. You’d be surprised how many companies plan out their entire benefits strategy but leave out how they’ll promote it to their team.

Ideally, take a multichannel approach:

- Launch via a companywide email announcement.

- Post it on the company’s intranet (if you have one).

- Have leaders mention it during upcoming meetings.

- Have Compt send an automated email to everyone who hasn’t joined after one week.

How Compt helps you run a controlled weight management stipend

Designing the right program is half the work. The other half is running it without burying your HR team in manual receipt review, payroll reconciliation, and tax classification. Compt’s lifestyle benefits platform handles the operational layer of your weight management stipend program.

How it works:

- Employees submit receipts through the Compt platform.

- Your team reviews and approves them against your defined eligible expense list.

- Reimbursements flow through payroll, with tax classification handled automatically.

Finance and HR need this to work in alignment. Finance gets clean reporting and predictable spend and HR can manage setup, approvals, and tracking from a single centralized platform.

It works for all three weight management stipend models: launching a dedicated stipend, adding weight management as an eligible category within an existing LSA, or consolidating a scattered wellness program into one platform.

And if you want to adjust categories, allowances, funding cadences, or anything else, you have the flexibility to do that without redesigning it from scratch.

Note: Compt provides the infrastructure for reimbursement-based benefits, including eligibility controls, documentation submission and approval, and payroll integration, but the compliance classification ultimately depends on how the program is designed.

Build your weight management stipend with Compt.

Healthcare and pharmacy costs are rising faster than most benefits budgets can absorb. CFOs are cutting programs that can’t prove their value. And the pressure to support GLP-1s — without the structure triggering a compliance issue — isn’t going away.

A weight management stipend built on Compt’s platform gives you a controlled, defensible answer to all three.

Request a demo of Compt today.

FAQs: How to build a weight management stipend program

Employers build a weight management stipend by choosing a reimbursement structure, defining eligible expenses, and setting a fixed budget with clear rules. This approach has become more common as employers look for ways to support rising demand for GLP-1 medications without expanding their medical plans.

In practice, employers decide whether weight management sits within an LSA, a wellness stipend, or a standalone program. They then define eligible expenses, set reimbursement limits, and communicate that the benefit is a taxable reimbursement rather than insurance coverage.

Can a Lifestyle Spending Account cover GLP-1 medications for weight management?

Yes. A Lifestyle Spending Account (LSA) can include GLP-1 medications as an eligible expense within a broader reimbursement program.

Because LSAs cover multiple categories, employees can apply the same allowance to weight management alongside other needs, making this the most flexible option for employers and employees.

What’s the best way to support GLP-1 costs without adding full insurance coverage?

The simplest approach is to use a reimbursement-based benefit such as an LSA, wellness stipend, or weight management stipend. These programs provide capped financial support without requiring employers to expand their medical plan.

The main difference between the three options is scope: LSAs are broad, wellness stipends are limited to health-related expenses, and weight management stipends focus specifically on metabolic health. Read the full breakdown in our dedicated guide, “Supporting GLP-1 Weight-Loss Coverage Using LSAs and Wellness Stipends | Compt.”

How do wellness stipends compare to LSAs for weight management benefits?

Wellness stipends and LSAs use the same reimbursement model when administered through Compt, but differ in scope. A wellness stipend is limited to health-related expenses, while an LSA allows spending across multiple categories.

Because LSAs apply to more employees and use cases, they typically see higher participation and utilization, while wellness stipends are more narrowly targeted.

How can employers cap GLP-1 reimbursement costs while still supporting employees?

Employers cap GLP-1 costs by setting fixed stipend allowances and limiting how much can be reimbursed per claim or per year. This ensures total program spend remains predictable.

For example, an employer may reimburse a portion of a GLP-1 expense instead of the full cost. This allows employees to offset costs while avoiding open-ended spending and the complexity of expanding pharmacy benefits.

Can employers use a taxable stipend to help cover GLP-1 copays and deductibles?

Yes. Employers can use a taxable stipend to reimburse GLP-1 copays and deductibles.

These reimbursements are processed as lifestyle benefits rather than prescription drug coverage, which keeps the program separate from formal health plan requirements.

What are the compliance and tax considerations for a weight management stipend?

Weight management stipends are typically treated as taxable income when delivered as a reimbursement benefit. This simplifies administration compared to formal health plans.

From a compliance standpoint, broader programs like LSAs and wellness stipends carry less risk because they cover multiple categories. More targeted weight management stipends require careful design to ensure they remain a reimbursement program rather than a regulated health benefit.

How do companies structure a weight management stipend versus a broad wellness stipend?

A wellness stipend covers general health-related expenses, while a weight management stipend is limited to expenses tied specifically to metabolic health.

The difference is scope. Wellness stipends support a wide range of health needs, while weight management stipends focus on a narrower set of expenses such as GLP-1 medications, nutrition programs, and fitness services.

What expenses can be included in a weight management stipend?

Weight management stipends cover expenses tied to metabolic health and weight loss, rather than general wellness. Common examples include GLP-1 prescriptions, clinically guided programs, nutrition coaching, and fitness support aligned to weight loss goals. Employers define the eligible categories to keep the benefit consistent and easy to administer.

How do employers support metabolic health benefits without adding a new health plan?

Employers support metabolic health by offering reimbursement-based benefits through Compt such as LSAs, wellness stipends, or weight management stipends. These programs provide a fixed allowance employees can use for eligible expenses.

This approach allows employers to offer support while maintaining predictable costs and avoiding the complexity of introducing a new health plan.

What’s the difference between GLP-1 insurance coverage and a lifestyle stipend?

GLP-1 insurance coverage is part of a formal health plan, while a lifestyle stipend is a defined reimbursement benefit with a fixed budget.

Insurance coverage is tied to plan rules and pharmacy benefits, while stipends allow employers to offer partial, controlled support without changing their existing health plan.

Editor’s note: Compt software supports the categorization and proper reporting of benefits according to IRS guidelines, helping businesses maintain compliance. However, Compt cannot provide tax advice, and users should consult their own tax, legal, and accounting advisors when necessary.