If you’re considering ThrivePass and ThrivePass alternatives, you’re likely looking for the best way to run flexible employee lifestyle benefits like stipends and Lifestyle Spending Accounts (LSAs) without creating extra work for HR, Finance, and payroll.

ThrivePass is best known as a broad lifecycle benefits platform and sits in a category often described as curated benefits marketplaces: one place to manage multiple programs, marketplace vendors, and spending options under a single system. That may be appealing if you want to offer your people lifestyle benefits alongside COBRA and pre-tax accounts.

For other teams — especially midmarket and enterprise teams running more complex programs — that breadth becomes the friction. What looks like “one platform for everything” turns into:

- Manual payroll or reconciliation work behind the scenes

- Prefunding requirements that tie up budget

- A mix of programs (LSAs, rewards, COBRA, pre-tax accounts) that don’t operate cleanly together

- An employee benefits experience that’s difficult to explain and hard for employees to consistently use

In these scenarios, the evaluation usually isn’t just about finding ThrivePass alternatives with similar features, but about deciding whether the curated marketplace model itself is the right fit for how your team wants to run benefits. Because in practice, most alternatives differ less on feature lists and more on:

- How benefits are funded and delivered (card-first, reimbursement-first, or hybrid)

- How much operational work sits with your team

- How well the program holds up for Finance, payroll, and compliance

Those decisions affect how the program runs internally and show up directly in the employee experience. How a lifestyle benefits program is designed directly shapes whether employees like and use a benefit … or ignore it.

Among Compt customers in 2025, activation reached 95% and participation reached 93%, according to the 2026 Annual Lifestyle Benefits Benchmark Report.

TL;DR: The fastest way to choose a ThrivePass alternative

A broad benefits marketplace like ThrivePass may be the right choice if:

- You want lifestyle benefits bundled with other programs like COBRA administration or pre-tax accounts.

- You’re comfortable managing additional administrative complexity.

- You’re evaluating benefits infrastructure more broadly, not just LSAs and stipends.

Choose a focused reimbursement-first platform like Compt if:

- You want flexible stipends and LSAs without prefunding debit card balances or relying on merchant-category enforcement.

- You want IRS-compliant payroll handling and receipt-backed taxable vs. nontaxable classification.

- You want a platform that is built for lifestyle benefits, not a broad benefits marketplace where LSAs are just one module.

- You are comfortable asking employees to spend out-of-pocket first and then submit their receipts for reimbursement.

That tradeoff is what gives employees maximum vendor flexibility while providing employers with more control over cost, compliance, and program design.

Throughout this article, we’ll compare four ThrivePass alternatives: Compt, Espresa, Forma, and Benepass. Their G2 ratings are relatively close:

- Compt: 4.8/5

- Forma: 4.8/5

- Benepass: 4.8/5

- ThrivePass: 4.1/5

- Espresa: 4.1/5

Full disclosure: Compt is our platform. We’ll present each vendor evenly and be direct about tradeoffs so you can make an informed decision.

What ThrivePass is, and why some teams start exploring alternatives

ThrivePass positions itself as a lifecycle benefits platform. In addition to Lifestyle Spending Accounts and stipends, it supports programs like COBRA administration, pre-tax accounts, commuter benefits, tuition reimbursement, and other adjacent benefits workflows.

For some organizations, that breadth is appealing. If you want one vendor covering multiple categories of benefits administration, ThrivePass may be a good option for you.

But the expansive nature of ThrivePass’s offerings creates tradeoffs. Based on what we hear from teams evaluating ThrivePass alternatives, the friction usually shows up in a few specific places:

- Manual payroll and finance workflows don’t fully go away. The LSA itself may work fine, but payroll handling can still feel more manual than expected, especially when benefits are direct-deposited and tax handling sits outside a clean, integrated workflow.

- Prefunding and reserve balances create cash exposure. When funds need to sit in a third-party account, Finance loses visibility and control. That may be manageable early on, but it becomes harder to justify as teams and programs grow.

- Adjacent features like swag fulfillment can frustrate employees. Delays, cancellations, inventory gaps, or lack of tracking visibility don’t feel like isolated issues to employees; rather, they shape how people perceive the benefit as a whole.

- A broad platform is never the best LSA platform. If your actual goal is to run a clean, flexible LSA program, a platform built to do many other things will often introduce more complexity than you want or need.

“ThrivePass right now — not only would I say is very limited in what we’re able to offer to our employees, but it is very, very frustrating for our employees. I get the privilege of being on the administrative side, but also on the employee side. Sometimes, myself trying to submit reimbursements, I’m like, ‘I get what you’re going through when you tell me you’re frustrated’ — because they deny my reimbursement. So I get it when they’re complaining. We just want something that’s a little bit easier.”

— Compt client call, November 2025

How ThrivePass alternatives compare in 2026 (complete table)

When you evaluate ThrivePass alternatives, the biggest difference isn’t necessarily the vendor, but how the platform is structured and how employees actually spend.

Here’s how the leading approaches compare:

| Broad benefits suite (e.g., ThrivePass) | Reimbursement-first platform (e.g., Compt) | Hybrid platform (e.g., Forma, Espresa) | Card-first platform (e.g., Benepass) | |

|---|---|---|---|---|

| Platform scope | LSAs + COBRA + commuter + pre-tax + fulfillment-based benefits (e.g., rewards, swag) | LSAs and stipends, including rewards and recognition, company swag, professional development, and built-in employee discounts | LSAs plus engagement, marketplace, or wallet features | LSAs combined with pre-tax benefits in a wallet |

| Spending method | Mix of reimbursement, direct deposit, and marketplace or fulfillment-based experiences (varies by program) | Employee pays first, then submits receipt | Mix of card, marketplace, and reimbursement models | Swipe card at checkout |

| Vendor flexibility | Moderate; varies by program and fulfillment method | Fully vendor-agnostic; employees can purchase from any retailer that meets your program’s eligibility rules | Marketplace + partial flexibility | Limited by merchant category codes |

| Approval logic | Varies by program; often post-purchase or fulfillment-based | Receipt-level review before payroll | Depends on method used | Real-time approval at merchant |

| Tax handling | May require coordination across multiple program types | Receipt-backed, categorized before payroll | Mixed depending on configuration | Often applied at merchant/account level |

| Payroll workflow | Can involve manual steps or reconciliation across programs | Clean, exportable payroll files | Varies by setup | May require reconciliation for edge cases |

| Cash flow model | May require prefunding or reserves depending on program | Pay only for approved expenses; any unused benefits dollars remain with the company | Often includes prefunded components | Requires prefunding balances |

| Employee experience | Varies by benefit type (reimbursement, marketplace, or fulfillment-based experiences) | Consistent, vendor-free experience across categories | Can feel fragmented across multiple spending paths | Simple when it works; friction when the dreaded card declines happen |

| Global support | Varies by program and region | Multicurrency reimbursements; local vendor flexibility | Broad coverage but inconsistent UX | Depends on card network and regional acceptance |

| Pre-tax support (HSA/FSA) | Yes | No | Depends on platform | Yes |

| Best for … | Companies consolidating pre-tax benefits and adjacent programs (e.g., COBRA) alongside LSAs, and are comfortable with added complexity from card-based spending, prefunding requirements, and fulfillment-dependent experiences | Teams prioritizing flexible LSAs, high participation, and streamlined lifestyle benefits administration through reimbursements that avoid prefunding or card friction | Companies that want multiple spending methods but are comfortable managing added complexity across card, marketplace, and reimbursement workflows | Teams prioritizing a card-based wallet experience, even if it introduces limitations in vendor flexibility, global usability, and checkout reliability |

Not all consolidation is the same. Platforms like ThrivePass are designed to consolidate broader benefits administration, including pre-tax accounts and COBRA support, into a single system. That can be valuable if your goal is reducing vendor count across your entire benefits stack.

If your primary focus is running lifestyle benefits well, consolidation means bringing stipends and LSAs, commuter benefits, tuition reimbursement, rewards and recognition, company swag, and similar programs into one flexible, vendor-agnostic system with a consistent employee experience and a simple, integrated payroll workflow.

The right model depends on your goals. A broader theme we often hear from clients is that when a platform tries to do too many things at once, the day-to-day experience for employees as well as HR and Benefits teams becomes harder to manage.

“I am forced to use ThrivePass as the administrator of my company’s HSA/FSA. … I would go out of my way to anti-recommend this platform for any benefits manager.”

— ThrivePass G2 review

Alternative #1: Compt — Reimbursement-first, vendor-agnostic lifestyle benefits

Compt is a reimbursement-first lifestyle benefits platform and one of the strongest ThrivePass alternatives for companies that want to consolidate flexible stipends, Lifestyle Spending Accounts (LSAs), and related lifestyle programs without adding unnecessary operational complexity.

Unlike broad benefits suites, Compt is built specifically for lifestyle benefits administration. That means companies can run stipends, LSAs, professional development, commuter benefits, tuition reimbursement, wellness and family support (including fertility support), rewards and recognition, company swag, and employee discounts in one platform — without also paying for infrastructure tied to COBRA, HSAs, FSAs, or other pre-tax administration they may not need.

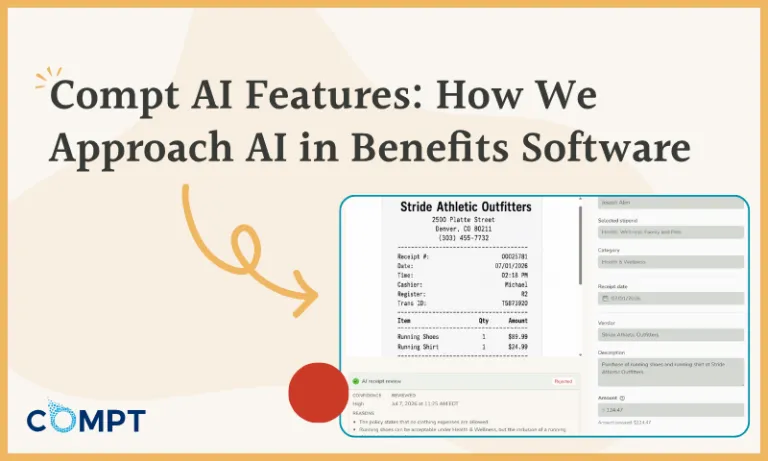

That focus matters because it creates one consistent experience for both employees and admins. Instead of switching between cards, marketplaces, and separate fulfillment flows depending on the program, employees use the same reimbursement-first workflow across lifestyle benefits. They can spend with any vendor that fits your company’s eligible categories, then submit a receipt for reimbursement in a simple, mobile-friendly flow.

HR and Finance receive receipt-backed documentation, clear taxable vs. nontaxable classification based on eligible expense categories, and exportable payroll reporting without juggling multiple benefits systems or prefunded balances.

Take a look at how it works:

What is Compt best for?

Compt is best for organizations that want to run flexible lifestyle benefits with less administrative work, an integrated payroll workflow, and more employee choice.

It is especially well-suited for distributed or global teams, midmarket companies consolidating multiple lifestyle benefits into one LSA, and HR and Finance teams that want to avoid prefunding balances or managing more platform complexity than necessary.

“Before implementing Compt, my team was fielding a lot of eligibility questions about our perks program and spent hours processing stipend requests. Compt brought structure: employees got clarity on what they could use, Finance got real-time visibility into spend, and HR got meaningful time back (often 10+ hours a month). Compt just worked, and that’s exactly what all of your HR tech stack should do.”

— Turiya Gray, Senior Partner & Fractional Chief People Officer at FXG Partners, in “HR Tech Stack for Midsize Companies: What I’d Build at 200–300 Employees”

Why teams choose Compt over broad suite-style platforms

The biggest difference is focus. ThrivePass is designed to cover a wide range of benefits workflows. Compt is designed to make lifestyle benefits run simply and well.

That shows up in a few important ways.

First, with Compt, there is no prefunding requirement for LSAs and stipends. Rather than parking employee-benefit funds in a third-party account, employers control their cash until approved reimbursements are processed through payroll.

Second, payroll and tax handling stay clean. Every expense is reviewed at the receipt level, categorized before payroll, and documented with an audit trail. That reduces the manual reconciliation work that often creeps back in when employee lifestyle benefits are handled across multiple modules or workflows.

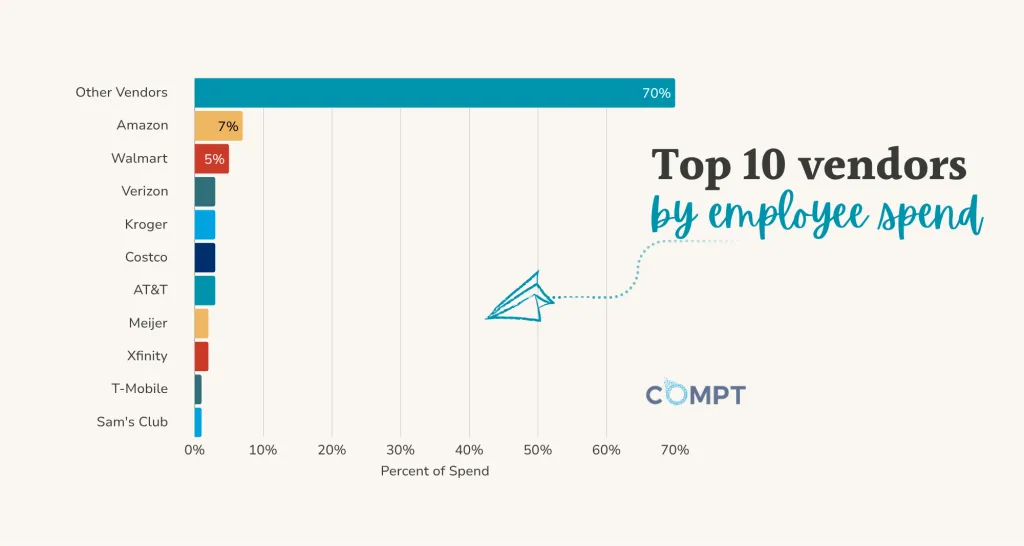

Third, employees are not boxed into a marketplace or fulfillment flow. They can spend where they already shop, including at local and niche vendors, which tends to create a more flexible and intuitive experience — and higher participation — over time. In 2025, 70% of stipend and LSA spending happened outside of major retailers, and programs built around this level of flexibility consistently see participation rates above 90%, as shown in our 2026 Annual Lifestyle Benefits Benchmark Report.

Because reimbursements are only paid on approved expenses, benefit spend is driven by actual claims rather than enrollment. Companies aren’t funding accounts or paying for unused seats — they’re paying only for what employees actually submit and use.

What you trade off by choosing Compt

The tradeoff is straightforward: employees do need to upload receipts.

For most companies, that is a worthwhile exchange for built-in IRS compliance, fewer point-of-sale problems, and more vendor flexibility. But if your top priority is a benefits suite that includes pre-tax administration or COBRA alongside LSAs, ThrivePass or another broad platform may still be a better fit.

When Compt is a strong fit

Choose Compt if your team wants to consolidate lifestyle benefits, not all benefits administration. Compt is a particularly strong fit if you want flexible stipend programs, mobile receipt upload, clear eligible expense categories, a straightforward payroll workflow, and a consistent employee experience across benefits.

“Compt gives my employer the ability to offer a fantastic benefit, providing me with $100 each quarter as a bonus to spend on something special for myself, my family, or even my pet. I also have the option to use this bonus toward paying my student loans, which is a great added perk. It is so easy and clear how to upload your purchase for reimbursements. I honestly can’t find any faults; the process is straightforward and truly impressive.”

— Compt G2 review

Alternative #2: Espresa — Marketplace-first platform with engagement layer

Espresa is a lifestyle benefits platform that combines LSAs with a mix of marketplace, card-based spending, and community features. Like ThrivePass, it sits in the curated marketplace category, where benefits, vendors, and engagement tools are bundled into a single platform.

What is Espresa best for?

Espresa is best for organizations that want to position lifestyle benefits as part of a larger employee engagement and culture program. It can be a strong fit for companies that:

- Want lifestyle benefits to live inside a highly visible, engagement-driven experience.

- Are investing in programs like ERGs, wellness challenges, and employee communities.

- Prefer a structured, marketplace-style environment over fully flexible spending.

Espresa’s strengths

The biggest advantage of Espresa is the integrated engagement layer. Benefits don’t exist in isolation; they’re part of a system that includes:

- Curated vendor marketplace

- Recognition and rewards programs

- Social, community, and engagement features

For organizations focused on visibility and culture, this can make benefits feel more cohesive and easier to promote internally.

What you trade off

Because Espresa uses a hybrid model (marketplace, card, and reimbursement), tradeoffs show up in both flexibility and operations:

- Vendor flexibility is more limited than with reimbursement-first platforms like Compt.

- Employees will need to navigate multiple spending paths depending on the benefit.

- The experience can feel inconsistent depending on how each benefit is delivered.

Like most hybrid platforms, this also introduces additional setup and administrative complexity over time, especially as programs expand across categories or geographies.

When Espresa makes sense

Espresa may be a fit if your goal is to combine lifestyle benefits with culture tools and you’re comfortable with a more structured, less flexible, marketplace-driven experience that reportedly falls short on the technical user experience and customer support options.

“Often the redemption of recognition rewards from points to gift cards does not process properly. Points are deducted from the Espresa account but subsequent links to gift card details, such as the gift card number and pin, are not provided or do not work. This has happened when ordering gift cards for Ebay and for Amazon. There is no live Customer Support to address issues, which must be reported within 3 business days.”

— Espresa G2 review

Alternative #3: Forma — Hybrid platform with multiple spending methods

Forma is a flexible benefits platform that combines LSAs with a mix of card-based spending, marketplace options, and reimbursements. Like Espresa, it’s best described as a hybrid model, where multiple spending methods coexist within the same system.

What is Forma best for?

Forma is best for companies that are comfortable managing multiple systems within one platform. It can be a strong fit for teams that:

- Want to offer card-based spending alongside reimbursements.

- Prefer optional marketplace experiences.

- Need flexibility across different benefit types.

Forma’s strengths

The main appeal of Forma is its flexibility in how benefits are delivered, rather than a single, unified experience. Organizations can mix and match:

- Card-based spending for convenience

- Marketplace experiences for certain categories

- Reimbursements for more controlled use cases

This makes Forma feel highly configurable, but it also means employees and admins are often interacting with different systems depending on the benefit.

What you trade off

That flexibility comes with a different kind of complexity than marketplace-first platforms like ThrivePass. Because Forma supports multiple spending methods:

- Admins need to manage multiple workflows across programs.

- Employees need to learn when to use a card, submit a claim, or use the marketplace.

- Card-based components can introduce merchant restrictions and declined transactions.

From a Finance perspective, hybrid models can also make tax handling less standardized and payroll reconciliation more complex across programs. Over time, this makes it harder to maintain a single, predictable system for both employees and HR and Finance teams.

When Forma makes sense

Forma may be a fit if your organization is comfortable managing the added complexity that comes with a hybrid model.

“The reimbursement process was really clunky unless you are strictly buying from the Forma store, which is limiting because you buy something thinking that you can get reimbursed for it with Forma, and then they reject it. That’s kind of frustrating. I also had an experience where my company’s contract/list of approved items specifically listed that you could buy clothing or other items for your dependents, but when I tried to get athletic clothing for my child, they rejected it. I still don’t understand why.”

— Forma G2 review

Alternative #4: Benepass — Card-first platform with wallet-style experience

Benepass is a lifestyle benefits platform built around a card-first model, where employees access benefits through a digital wallet and spend using a prepaid card. It emphasizes a real-time spending experience at the point of purchase.

What is Benepass best for?

Benepass is best for organizations that prioritize a card-based experience and want employees to access benefits without submitting receipts. It can be a strong fit for teams that:

- Want a wallet-style benefits experience.

- Prefer real-time transactions over reimbursements.

- Value perceived simplicity at checkout.

Benepass’s strengths

The main advantage of Benepass is ease of use at the point of sale. Employees can:

- Swipe a card instead of submitting their receipts.

- Access benefits through a single wallet interface.

- Use funds immediately without waiting for reimbursement.

For some teams, that immediacy improves perceived usability.

What you trade off

Card-based systems come with structural limitations tied to how transactions are approved. Because spending is typically governed by merchant category codes:

- Vendor flexibility is more limited.

- Legitimate purchases can be declined or incorrectly approved.

- Employees may experience checkout friction when transactions fail.

From a Finance standpoint, programs typically require prefunding balances, which impacts cash flow and visibility, and edge cases often require manual reconciliation or exception handling.

When Benepass makes sense

Benepass may be a fit if your priority is a card-based, real-time experience, and you’re comfortable with tradeoffs in flexibility, global usability, and financial control and cash flow.

“I don’t like Benepass. … Benepass doesn’t solve problems for me; it creates issues that didn’t exist before by misunderstanding our company policies and coverage, leading to denied reimbursements and lost benefits.”

— Benepass G2 review

Which ThrivePass alternative is right for your team?

Choose Compt if you want vendor-agnostic LSAs, reimbursement-first spending, predictable cash flow, and payroll-ready tax handling without prefunding balances or managing multiple benefits workflows. It’s especially strong for teams that want one platform for lifestyle benefits, without buying into a broader benefits admin suite.

Choose Espresa if you’re looking for a broader engagement and culture platform that includes lifestyle benefits alongside ERG support, wellness challenges, and a curated marketplace with no markups.

Choose Forma if you want multiple spending methods (card, marketplace, and reimbursements) and are comfortable managing the added complexity of a hybrid model.

Choose Benepass if you prefer a card-first, wallet-style experience and want employees to access benefits at the point of purchase without submitting receipts.

Ultimately, choose a broad benefits suite like ThrivePass if your goal is consolidating lifestyle benefits with compliance-heavy programs like COBRA or pre-tax accounts under one vendor, and you’re OK with the usability tradeoffs.

Why HR and Finance teams choose Compt after evaluating ThrivePass alternatives

When teams move away from ThrivePass-style platforms, it’s usually for three reasons: reducing operational complexity for admins, eliminating prefunding or cash exposure, and refining a fragmented or unsatisfactory employee experience.

Compt solves those issues by focusing specifically on how lifestyle benefits are delivered. With a reimbursement-first model, you:

- Pay only for approved expenses — no prefunded balances or reserve accounts.

- Get receipt-backed tax classification before payroll runs.

- Give employees vendor freedom without marketplace restrictions or fulfillment delays.

- Run stipends and LSAs through one consistent workflow across all categories.

- Manage approvals, reporting, and payroll exports in one streamlined system.

Unlike broad benefits suites, Compt is designed specifically for streamlined lifestyle benefits administration. That focus creates a consistent experience across employee benefits programs like wellness stipends, LSAs, professional development, rewards and recognition, commuter benefits, employee discounts, and company swag — without layering on infrastructure tied to COBRA, pre-tax accounts, or other adjacent systems you may not need.

Ultimately, the right choice depends on what you’re optimizing for. If your priority is consolidating multiple types of benefits administration into a single vendor, a broad platform like ThrivePass may be the right fit.

But if your goal is to run flexible lifestyle benefits with less administrative overhead and higher employee participation, a more focused, reimbursement-first platform will typically offer a simpler and more predictable experience. Compt was built by a three-time CFO and two-time COO specifically for teams looking for flexible, vendor-agnostic lifestyle benefits with predictable cash flow and receipt-backed IRS compliance.

If you’re evaluating ThrivePass alternatives, request a Compt demo to see how reimbursement-first lifestyle benefits work in practice.

FAQs: ThrivePass alternatives for stipends and LSAs

The most common ThrivePass alternatives include Compt, Forma, Espresa, and Benepass. The right choice for you depends on how each platform delivers benefits.

Here’s how these platforms compare based on G2 ratings:

Compt: 4.8/5

Forma: 4.8/5

Benepass: 4.8/5

ThrivePass: 4.1/5

Espresa: 4.1/5

Compt is a reimbursement-first platform designed specifically for lifestyle benefits, including LSAs, stipends, and related programs like professional development, commuter benefits, tuition reimbursement, recognition, and company swag. Forma and Espresa operate as hybrid platforms, combining card-based spending, marketplaces, and reimbursements. Benepass is a card-first platform built around a wallet-style experience.

ThrivePass itself sits in a different category: a broader benefits suite that includes LSAs alongside COBRA, pre-tax accounts, and other administrative programs.

In practice, the decision comes down to whether you want a focused lifestyle benefits platform or a broader benefits infrastructure that includes LSAs as one component.

How do ThrivePass vs. Compt vs. Forma vs. Benepass compare?

These platforms differ primarily in structure. ThrivePass is a lifecycle benefits platform that bundles LSAs with COBRA administration, pre-tax accounts, and other adjacent programs. Compt is a reimbursement-first platform designed specifically for lifestyle benefits, including LSAs, stipends, and related programs like professional development, commuter benefits, tuition reimbursement, recognition, and company swag, that integrates directly with payroll. Forma offers a hybrid model with card, marketplace, and reimbursement options. Benepass centers on a card-first wallet experience with real-time approvals at checkout.

Those structural differences affect how employees spend (card vs. reimbursement vs .marketplace), how eligibility is enforced (merchant-level vs. receipt-level), and how cleanly expenses flow into payroll.

This shift toward simpler, more focused platforms isn’t theoretical. According to Compt’s 2026 Annual Lifestyle Benefits Benchmark Report, 64% of employers offered an all-inclusive LSA in 2025, reflecting a distinct move away from fragmented benefits programs toward consolidated, flexible models.

In most evaluations, the deciding factor is which model creates the least friction for your employees and HR and Finance teams.

What’s the difference between a benefits marketplace and a reimbursement-first platform?

A benefits marketplace provides a curated set of vendors or services that employees can choose from, often paired with discounts or pre-negotiated offerings.

A reimbursement-first platform allows employees to spend with any vendor that fits employer-defined categories, then submit receipts for approval and reimbursement. Marketplace models can feel more guided, but they inherently limit choice.

Reimbursement-first models prioritize flexibility and align more closely with how employees actually spend in real life. That difference shows up in real usage. Benchmark data shows that all-inclusive LSAs reach 93% participation, with similarly high engagement for everyday categories like wellness (85%) and cell/internet (88%). When lifestyle benefits align with how employees already spend, participation follows.

Should we use a broad benefits suite or a focused LSA platform?

It depends on what you’re trying to solve. A broad benefits suite like ThrivePass is designed to consolidate multiple programs, such as COBRA, commuter benefits, pre-tax accounts, and LSAs, under one vendor. That can simplify procurement and vendor management if you’re looking to centralize your entire benefits stack.

Compt is a reimbursement-first platform built to run lifestyle benefits, such as stipends, LSAs, and related programs, cleanly and efficiently. It covers multiple benefit types, including commuter benefits and tuition reimbursement, within the same LSA and stipend experience that prioritizes flexibility, ease of use, and streamlined payroll workflows.

If your primary goal is consolidating benefits administration across categories, a suite may make sense. If your goal is improving how lifestyle benefits actually run day to day, a more focused platform is often the better fit.

Many companies are already moving in this direction, consolidating multiple stipends into a single LSA that supports multiple categories under one structure. The result is broader participation and more predictable administration.

This consolidation dynamic matters for another reason, too. Many midsized HR teams have accumulated a patchwork of benefits vendors over time, each with its own contracts, billing cycles, integrations, and employee portals. The administrative burden alone has become a real cost center, and CFOs are taking note.

When companies can replace multiple underperforming point solutions with one flexible platform — and only pay for what employees actually use — it fundamentally changes the conversation. Instead of adding another fixed line item, reimbursement-based lifestyle benefits become a pay-for-utilization model rather than a pay-for-enrollment model, which is especially compelling as benefits budgets come under greater scrutiny.

What’s the difference between card-based, marketplace, and reimbursement benefits platforms?

These models differ in how employees access and use their benefits.

Card-based platforms allow employees to pay directly at checkout, with transactions approved or declined in real time based on merchant category rules.

Marketplace platforms offer curated vendors or services that employees can select from, sometimes alongside other spending methods.

Reimbursement platforms allow employees to spend first and submit receipts for review before payroll runs.

Hybrid platforms combine these approaches, which increases flexibility but also introduces more complexity.

Each model optimizes for something different:

-Card-based: Immediacy at checkout

-Marketplace: Curated experience

-Reimbursement: Employee flexibility and IRS compliance

In practice, employees tend to prioritize benefits that support everyday needs. Compt’s 2026 Annual Lifestyle Benefits Benchmark Report found that nearly 1 in 10 stipend dollars is spent on groceries and household essentials, reinforcing that flexibility matters more than predefined vendor options.

Should we administer LSAs through reimbursement or a card?

Reimbursement-based LSAs provide receipt-backed documentation and clearer taxable and nontaxable classification, and eliminate the need to prefund balances. Employees make purchases and submit receipts, and approved expenses are processed through payroll.

Card-based LSAs offer real-time approvals and a familiar payment experience. Employees can swipe a card instead of submitting receipts, but transactions are governed by merchant category rules and prefunded balances. They can also introduce the need for manual reconciliation at tax time.

Funding structure also plays a role. Benchmark data shows utilization can vary significantly depending on how programs are delivered. For example, in 2025, quarterly-funded programs reached 85% utilization compared to 52% for monthly programs, highlighting how design choices impact outcomes.

Organizations that prioritize predictable cash flow, audit readiness, overall IRS compliance, and fewer edge cases often prefer reimbursement-first models.

See our full comparison of debit cards vs. reimbursement-based LSAs for a deeper breakdown.

How do benefits platforms impact payroll and tax handling?

Benefits platforms vary significantly in how they handle tax classification and payroll integration.

In some models, tax handling happens after the fact, requiring Finance teams to reconcile taxable and nontaxable expenses across programs or reports. This is more common in platforms where multiple benefit types or spending methods coexist.

In a reimbursement-first model like Compt, tax treatment is applied at the receipt level before payroll runs. Expenses are categorized and documented as they’re submitted, which allows for cleaner payroll exports and reporting.

For Finance teams, the difference shows up in how much manual reconciliation is required (and how confident they are in the data going into payroll). Across programs, one pattern is consistent: employees direct spending toward categories that are easy to understand and widely applicable, regardless of tax treatment.

Do lifestyle benefits platforms require prefunding?

Whether lifestyle benefits require prefunding depends on the model.

Card-based platforms typically require employers to prefund balances so employees can spend at the point of purchase. Hybrid platforms often include prefunded components as well.

Reimbursement-first platforms do not require prefunding. Employers reimburse only approved expenses, which means unused allocations remain with the company. For Finance teams, this difference positively affects cash flow, working capital, and financial visibility, especially as companies and benefits programs scale.

It also shifts how companies think about benefits spend more broadly. Reimbursement-first programs like Compt follow a pay-for-utilization model, where employers only pay for approved expenses employees actually incur rather than funding accounts upfront or paying for unused seats.

On average, employers fund lifestyle benefits at controlled levels. Median all-inclusive LSA funding is around $1,200 per employee annually in 2025, though actual ranges vary widely based on company size and structure.

What are the best ThrivePass alternatives for global teams?

Platforms like Compt, Forma, Espresa, and Benepass are all evaluated in global contexts, but for global teams, the key consideration is how lifestyle benefits translate across currencies, vendors, and regions.

A reimbursement-first platform like Compt tends to scale more smoothly internationally because employees can spend with local vendors and submit expenses in their local currency, while Finance maintains centralized reporting.

In 2025, 20% of Compt customers supported employees outside the U.S. across 62 countries, with most using a consistent LSA structure to maintain parity across regions. Among international customers in Compt’s database, 57% anchor their benefits strategy with an all-inclusive LSA.

Card-based and marketplace-driven models can work globally, but the experience may vary depending on merchant acceptance, currency conversion timing, and regional vendor availability.

Has anyone used ThrivePass or similar platforms? What are the pros and cons?

Experiences tend to reflect the platform model more than the vendor itself. Broad benefits suites like ThrivePass are often valued for consolidating multiple programs under one vendor. However, teams find that managing different benefit types within the same platform introduces complexity when workflows vary across programs.

Hybrid and marketplace platforms are often appreciated for offering multiple ways to engage with benefits, but can require more guidance and configuration to maintain consistency.

A reimbursement-first platform like Compt is typically described as more flexible and easier to reconcile because expenses are reviewed and categorized before payroll. Companies are increasingly prioritizing participation over raw utilization as the primary success metric, focusing on whether employees actually use the benefit at all, not just how much of the budget is spent.

What is better: a benefits marketplace, debit card, or reimbursement model?

Each model optimizes for a different outcome, but the more useful question is which one aligns with how your employees actually use benefits. The best model is the one that your employees understand, trust, and consistently use, and programs that reduce friction tend to see higher participation.

Marketplace systems provide curated options and can feel structured, but limit where employees can spend.

Debit cards prioritize immediacy, but rely on merchant category enforcement, which can introduce friction when transactions don’t align cleanly with eligibility rules.

Reimbursement-first models prioritize flexibility, compliance, and consistency across programs by allowing employees to spend where they already shop and submit receipts within defined categories.

This is also why many companies are shifting toward models that tie spend directly to usage. A pay-for-utilization approach, rather than paying for access or enrollment, aligns benefits budgets more closely with actual employee value, which is becoming increasingly important as costs rise. Among the options, the reimbursement model is the only one that does this.

The benchmark data consistently points in one direction: benefits work best when they align with real-life spending. Programs built around flexible LSAs achieve 93% participation and high utilization across employee types, including hourly and international workers.