If you’re considering Benepass, you’re likely working to solve a very real problem: how to give employees access to flexible lifestyle benefits like stipends and Lifestyle Spending Accounts (LSAs) without creating a second job for HR or a reconciliation nightmare for Finance.

Benepass is best known for a card-first experience: employees swipe the card at a point-of-sale register or online, and the platform approves or declines transactions based on merchant rules. For some teams, that convenience is the point. For others, it’s where the friction begins: card declines at the wrong moment, confusion about what is and isn’t eligible, and edge cases that still end up as questions in HR’s inbox.

This guide walks through the top Benepass alternatives and competitors for LSAs and employee stipend software in 2026 and helps you choose based on decision criteria such as:

- Spending model: card-first, reimbursement-first, or hybrid

- Employee experience: flexibility vs. “will this card work here?”

- Finance controls: taxable vs. nontaxable handling, audit trail, payroll exports

- Global reality: multicurrency support and cross-border compliance expectations

Before we get started, let’s ground this evaluation in what high-performing lifestyle benefits programs optimize for in 2026: participation and utilization. Among Compt customers in 2025, activation reached 95% and participation among active users reached 93%, according to our 2026 Annual Lifestyle Benefits Benchmark Report. That same report found 64% of employers now run their lifestyle benefits through a single, all-inclusive LSA rather than scattered standalone stipends — consolidation has become the default operating model for many companies.

That data is specific to Compt, but it reinforces the point: the platform model you choose can directly impact whether employees actually use the benefit.

TL;DR: The fastest way to choose a lifestyle benefits platform

Choose a Benepass-style platform (card-first with integrated pre-tax accounts) if:

- You want a single wallet experience that consolidates pre-tax accounts (like HSA/FSA) and post-tax lifestyle benefits onto a card.

- You prefer real-time transaction approvals at checkout and are comfortable with merchant-category enforcement.

- You’re looking for deeper integration between lifestyle perks and healthcare savings infrastructure.

Choose a reimbursement-first platform like Compt (vendor-agnostic lifestyle benefits) if:

- You want to offer flexible stipends and LSAs that employees can use with any vendor, without point-of-sale declines.

- You want clear, traceable IRS compliance built right in, including receipt-backed substantiation and clear taxable vs. nontaxable classification before payroll runs.

- You want to avoid prefunding large card balances and instead pay only for approved reimbursements.

Throughout this article, we’ll compare Benepass to four alternatives: Compt, Forma, ThrivePass, and Espresa.

Full disclosure: Compt is our platform. We’ll present each vendor evenly and be direct about tradeoffs so you can make an informed decision.

What Benepass is, and why some teams start exploring alternatives

Benepass is known for its card-first model that combines pre-tax accounts (such as HSAs, FSAs, and commuter benefits) with post-tax stipends and LSAs into a single wallet experience. Employees receive a physical or virtual card and use it to make purchases at checkout, whether in person or online, and transactions are approved or declined in real time based on merchant category rules and employer eligibility policies.

For many organizations that choose this path, that simplicity is the appeal: employees get one card, one login, and one consolidated view of all their benefits. Bam. Easy-peasy.

But the very mechanics that make these card-first programs feel convenient also introduce friction as companies scale and/or expand globally.

Here are the most common reasons teams begin evaluating Benepass alternatives:

1. Merchant-category enforcement doesn’t always match real-world purchases.

Card-based systems typically approve transactions at the merchant category code (MCC) level, not the item level. That means a purchase at a grocery store is treated the same whether it’s protein powder or a bottle of wine. When you’re trying to align spend tightly to policy intent or distinguish taxable from nontaxable categories, this limitation means HR and Finance teams likely need to spend time manually reviewing edge cases.

“One challenge we’ve run into is that the spending categories can sometimes be too broad, which makes it difficult to allow certain services or products without approving an entire category. We’ve also occasionally found, through monthly audits, that some purchases were approved outside of the intended eligible categories.”

— Benepass G2 review

2. Prefunding creates cash exposure.

Card-first programs require employers to prefund benefit allocations. That capital sits in the program until employees spend it. If you have a large employee headcount or high monthly benefits allocation, that translates into significant working capital tied up in advance, rather than paid out only when expenses are approved and processed.

3. Cards cause point-of-sale friction.

Real-time approvals are fast—until they aren’t. Card declines can happen for merchant-code mismatches, insufficient funds, category restrictions, or fraud checks. Even when card declines are rare, they tend to happen in visible moments, which can create a frustrating employee experience.

“It wasn’t written on the app which places are allowed. I don’t want my card to decline at the cash register. If only there was a way to find out beforehand. Also, if the card declines, then I need to remove items I originally planned to purchase.”

— Benepass G2 review

4. The global experience is inconsistent and varies by region.

Card-based and marketplace-driven benefit models often work best in the country in which they’re built. As companies expand globally, nuances like currency conversion timing, local merchant acceptance, affiliate partnerships, and postal-code verification can create noticeable friction for international employees.

In Benepass G2 reviews, users outside the U.S. have noted:

- Currency conversion timing that doesn’t align neatly with reimbursement expectations

- Limited affiliate or discount coverage in certain regions

- Merchant or billing address mismatches when using cards internationally

These aren’t universal problems, but they do surface more often in distributed workforces that rely LSA debit cards.

5. Benepass is expanding into pre-tax and HSA infrastructure.

In January 2026, Benepass rolled out an integrated HSA investing experience with a $125 investment minimum and no hidden fees. More than 25% of Benepass HSA account holders now invest their balances, compared to roughly 7–10% at traditional HSA providers. This indicates a continued push toward becoming a broader pre-tax and financial wellness infrastructure platform, rather than focusing exclusively on flexible LSAs and lifestyle stipends. (Benepass’s HSA banking runs through a third-party bank partner, because Benepass itself is a fintech rather than a bank or investment adviser. That’s a standard structure for this type of product, but worth flagging for Finance due diligence.)

For organizations that want pre-tax investing and post-tax stipends consolidated on one platform, that’s a real differentiator. For those whose primary goal is running flexible LSAs and stipends cleanly, it introduces additional complexity — and it’s worth noting Compt doesn’t offer HSA, FSA, or HRA accounts at all. That’s not a missing feature; HSA/FSA administration is a fundamentally different regulatory and banking function than reimbursing flexible lifestyle spend, and most companies already have it covered through their health plan broker or a dedicated HSA custodian.

Most Compt customers run that stack alongside Compt rather than looking for one vendor to do both.

What does Benepass actually cost?

Benepass doesn’t publish pricing, but third-party contract-data sources (Vendr) put its platform fee around $4–$12 per employee per month, scaling with company size and contract length, with no transaction fees on employee spending.

For context: a 200-employee company offering $100/month in combined stipends would pay roughly $9,600–$28,800/year in platform fees on top of $240,000 in benefit funding, or about $250K–$270K total annually.

One HR leader evaluating both platforms told us Benepass quoted their sub-100-employee organization $15K before the stipend budget was even factored in — a steep ask when you’re still building the internal case for launching an LSA at all.

How card-first and reimbursement-first platforms compare in 2026 (complete table)

When you evaluate Benepass alternatives, the most important distinction isn’t the brand, but the architecture. Most lifestyle benefits platforms fall into one of three structural models:

- Card-first (wallet model)

- Reimbursement-first (vendor-agnostic model)

- Hybrid (card + marketplace + reimbursement)

Here’s how they all compare:

| Evaluation factor | Card-first model (e.g., Benepass-style) | Reimbursement-first model (e.g., Compt-style) | Hybrid model |

|---|---|---|---|

| Spending method | Swipe a physical/virtual card at checkout | Employee pays first, then submits receipt for reimbursement | Combination of card, marketplace, and reimbursements |

| Vendor flexibility | Limited by merchant category codes (MCC) and card acceptance | Any vendor that fits employer-defined categories | Marketplace vendors pre-approved; card + reimbursements vary |

| Approval logic | Approved/declined in real time at merchant level | Reviewed at receipt level before reimbursement | Depends on which method is used |

| Tax treatment | Often applied at account or merchant level; edge cases may require reconciliation | Receipt-backed substantiation before payroll export; clear taxable vs. nontaxable classification | Mixed depending on method |

| Cash flow model | Typically requires prefunding allocated balances | Pay only for approved expenses; unused allocations remain with employer (i.e., you save money when benefits go unused) | Often requires prefunding for card component |

| Point-of-sale experience | Instant approval, but potential for embarrassing and inconvenient card declines | No declines at checkout; reimbursement happens after submission | Card may decline; marketplace rarely does |

| Global support | Dependent on card network acceptance and currency conversion timing | Reimbursements processed in local currency with centralized reporting; employees can choose local vendors | Varies by configuration |

| Pre-tax account support | Yes | No | Often yes, but depends on the vendor |

| Best for … | Teams prioritizing card convenience and pre-tax + post-tax wallet integration | Teams prioritizing vendor freedom, tax clarity, predictable spend, and lifestyle benefits without a pre-tax component | Enterprises that want maximum options |

What this means

- Card-first platforms optimize for checkout convenience and consolidated wallet infrastructure, often including pre-tax accounts like HSAs and FSAs.

- Reimbursement-first platforms optimize for vendor flexibility, receipt-level IRS compliance, and predictable cash exposure. They’re often the best choice for minimizing administrative headaches while providing employees with the most choice in how they use their benefits.

- Hybrid models attempt to combine both, which increases flexibility (and complexity right along with it).

In practice, reducing friction (like declines, vendor restrictions, and unclear eligibility) tends to increase participation because employees trust they can use the benefit without surprises.

“Compt increased engagement with this benefit so that employees knew the value and applied it to the areas of their lives they preferred.”

— Compt G2 review

Compt vs. Benepass and other LSA alternatives at a glance

| Compt | Benepass | Forma | Espresa | ThrivePass | |

|---|---|---|---|---|---|

| Model | Reimbursement-first | Card-first + pre-tax | Hybrid (card + marketplace + reimbursement) | Hybrid (card + marketplace, engagement suite) | Marketplace/card + lifecycle benefits |

| Best for company size | SMB through enterprise | Midsize to enterprise | Midmarket (200+) to large enterprise | Global enterprise | Midmarket, PEOs |

| Global reach | Global, multicurrency reimbursement | Card-network dependent | 110+ countries | Global enterprise focus | Primarily U.S.-centric |

| Pre-tax/HSA support | No | Yes — expanded HSA investing in 2025–2026 | Yes (HSA, FSA, HRA) | No | Yes (FSA, HSA, HRA) |

| Notable 2026 change | Added Employee Discounts; SNHU pay-after-completion partnership; 2026 midyear benchmark report forthcoming | HSA investing push: 25%+ of holders now invest vs. 7–10% industry average | Named to TIME’s 2026 Top WorkTech Companies list | Released 2026 LSA trends report | N/A |

Quick checklist for choosing a Benepass alternative

Before evaluating individual vendors, clarify what matters most to your HR and Finance team:

- Spending model: Do you prefer card-first spending, reimbursement-first flexibility, or a hybrid approach?

- Vendor freedom: Will employees be limited by merchant codes or curated marketplaces, or can they use any vendor that fits policy?

- Tax handling: Can the platform clearly separate taxable vs. nontaxable categories before payroll runs?

- Cash flow exposure: Are you comfortable prefunding balances, or do you want to pay only for approved expenses?

- Global support: If you operate internationally, does the platform support multicurrency reimbursements and localized administration?

- Admin lift: Can HR and Finance run the program without spreadsheets or manual reconciliation?

Once you’re clear on these priorities, the vendor differences become much easier to evaluate.

Let’s dig in.

Alternative #1: Compt — Reimbursement-first, vendor-agnostic lifestyle benefits

What is Compt best for?

Compt is best for organizations that want to run flexible Lifestyle Spending Accounts (LSAs) and stipends without prefunding cards, managing merchant-code restrictions, or manually reconciling taxable vs. nontaxable spend at payroll.

It’s particularly well suited for:

- Distributed or global teams (75+ countries supported)

- HR teams that want minimal monthly admin lift

- Finance teams that require receipt-backed audit trails

- Companies consolidating multiple stipends into one LSA structure

- Employers prioritizing vendor flexibility for their people over marketplace control

Compt does not issue a benefits debit card. Instead, it operates on a reimbursement-first model.

That architectural difference drives the experience for both your people and your HR and Finance team.

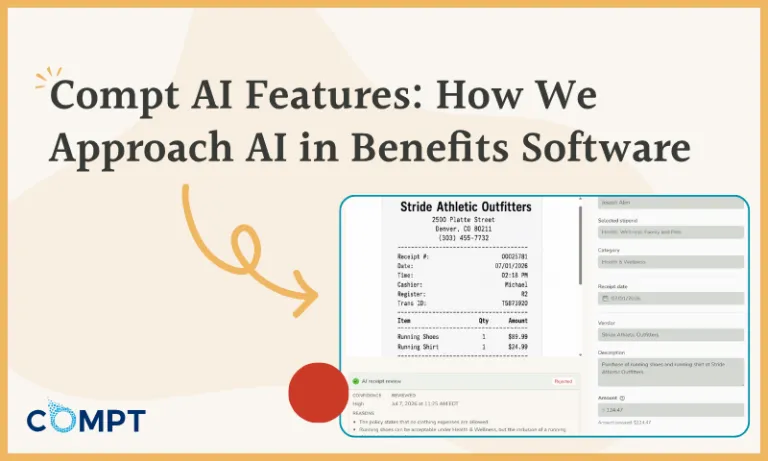

How Compt works

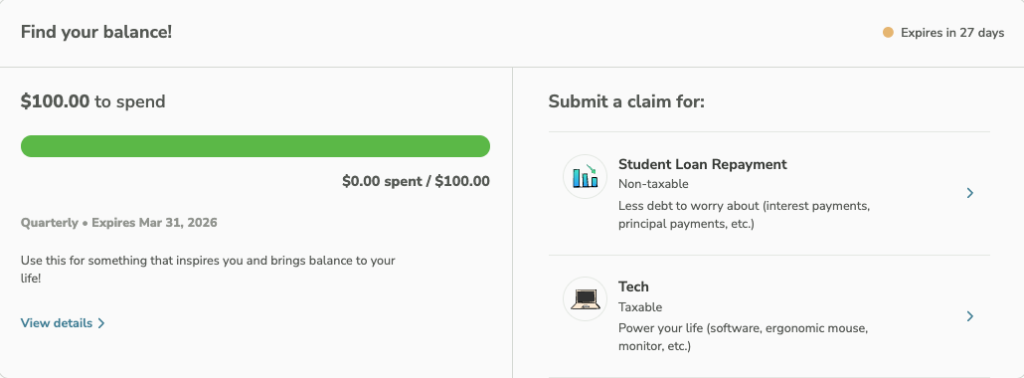

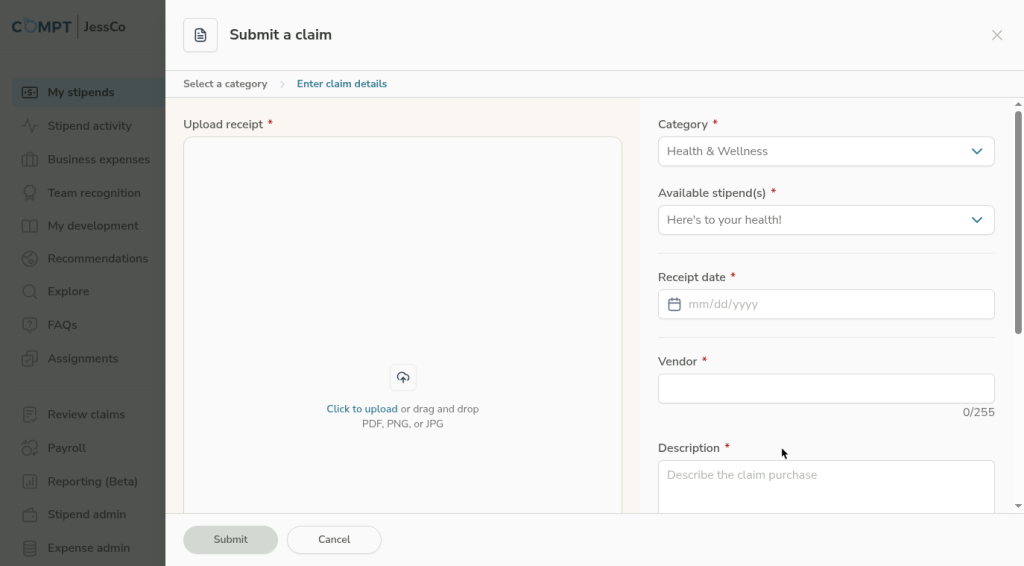

With Compt, your employees can use their lifestyle benefits with any vendor that fits your employer-defined categories. They simply select the appropriate LSA or stipend category, upload their receipt, fill in a few quick details, and submit.

If your employee’s purchase:

- Fits policy

- Falls within their available stipend balance

- Matches your category rules

Then it moves through approvals and you can easily export it before you run payroll.

Here’s how it works from the administrative point of view:

Key differentiators from Benepass

1. No prefunding

As we’ve noted, card-first programs require allocated funds to sit in an account before they’re spent.

Compt does not hold employer funds. You pay only for approved reimbursements when payroll runs. Any unused allocations remain with the employer, which means you actually save money on lifestyle benefits you offer that your employees opt not to use.

For large teams or large monthly benefits allocations, this materially reduces your working capital exposure.

2. Receipt-level tax classification

Each stipend category is configured with tax treatment (taxable or nontaxable). Employees see this classification at submission, which improves their ability to make decisions about their spending rooted in their own personal finances.

An example: With my quarterly Compt LSA, I have 20 categories available, and I always choose “student loan repayment” because it’s nontaxable. There are other dedicated stipends for wellness and office equipment with which I can be reimbursed for purchases in taxable categories, so why increase my taxable income here when I have other options?

With Compt, because every expense is receipt-backed:

- Taxable vs. nontaxable spend is separated before payroll export.

- Audit trails include timestamps, approvals, and documentation.

- Payroll files are formatted by tax treatment and easily exportable.

This eliminates the need for manual reconciliation at the end of the year.

3. Global, multicurrency reimbursements

Compt supports employees in 75+ countries. Within the Compt platform, employees see balances in their local currency, reimbursements are processed in their local currency, and Finance still receives centralized reporting.

Employees are also free to make local purchases from vendors they’re familiar with instead of being locked into a pre-approved vendor list for which there may be no options close to home.

For distributed teams, this avoids the friction of card acceptance limits, billing address mismatches, and currency conversion timing issues. It’s also simple to create user groups and define currencies and policies by each, so if an employee moves to another country, it’s easy to move them to the related group.

4. Configurable, flexible stipends and LSAs

Compt admins can create:

- Recurring stipends (monthly, quarterly, annual)

- One-time stipends or spot bonuses

- Consolidated, all-inclusive LSAs

- Role- or location-based eligibility groups

And remember those 20 LSA categories I mentioned above? Your options include, but are not limited to:

- Health and wellness

- Professional development

- Family care

- Remote work

- Commuter benefits

- Charitable giving

- Company swag

- Rewards and recognition

- Employee discounts

- Pets

- A full 28 stipend categories to design into your benefits structure

And one of the coolest parts? Eligibility syncs with your HRIS integrations to automate new hire inclusion and terminations.

5. Approval and reporting workflow

Compt admins have access to:

- Bulk approval queues

- Status tracking (Open, In Review, Approved, Processed)

- Payroll exports grouped by tax treatment

- Audit-ready reports with receipt documentation

- Real-time dashboards showing participation and utilization

According to our 2025 benchmark data, 99% of submitted expenses on the Compt platform were approved in the first half of the year, which reflects overall category clarity and employee understanding.

What you trade off by choosing Compt

There’s no way around it: Reimbursement-first models require employees to upload receipts.

For most teams using Compt, this takes minutes and employees don’t mind. That said, we recognize that eliminating receipt submission is a priority for some organizations. We’re not for everyone!

This single tradeoff is the core difference between reimbursement-first and card-first models.

“As someone who uses Compt, I find the process of submitting my reimbursements for stipends to be very user-friendly. I also appreciate that the platform gives companies an intuitive way to demonstrate how much they value their employees.”

— Compt G2 review

Online ratings

Compt is rated 4.8 out of 5 stars on G2.

When Compt is a strong fit

Choose Compt if:

- You want vendor flexibility without merchant-code restrictions.

- You want clear IRS-aligned reporting before payroll runs.

- You want to avoid prefunding card balances.

- You operate globally and need multicurrency reimbursements.

- You want to consolidate stipends into a single LSA.

If your priority is consolidating pre-tax accounts (HSA/FSA) and post-tax stipends into a single wallet-style debit card, a card-first platform like Benepass may be better aligned.

Alternative #2: Espresa — Engagement platform with built-in lifestyle benefits

What is Espresa best for?

Espresa is ideal for organizations looking to combine Lifestyle Spending Accounts with broader employee engagement tools like challenges and community groups inside a single platform.

Espresa positions itself as a “culture and total well-being” platform that includes LSAs alongside employee resource groups (ERGs), social recognition, well-being challenges, and rewards programs.

Rather than focusing on stipend and reimbursement infrastructure and creating a world-class experience there, Espresa embeds lifestyle benefits within a larger engagement suite. This option is considered a hybrid model because it features an LSA debit card, curated vendor marketplace (with no markups), and reimbursement within a broad engagement ecosystem.

Espresa’s strengths

- Integrated recognition, challenges, and community features

- Marketplace-style redemption options alongside reimbursements

- Consolidated engagement reporting across programs

- Zero-markup marketplace positioning for rewards

For teams that want lifestyle benefits tightly connected to culture programming, this unified structure can simplify your approach and the employee experience.

Tradeoffs to consider with Espresa

- Broad engagement platforms introduce unnecessary administrative complexity if your primary goal is running LSAs cleanly and at scale.

- Marketplace-driven elements limit vendor flexibility compared to fully vendor-agnostic reimbursement models.

- Card-based components may encounter declines at POS checkout.

- Teams focused on moving away from spreadsheets to built-in tax classification and payroll automation will likely find the engagement features more expansive than necessary.

When Espresa makes sense

Espresa is an option when your priority is building a culture and engagement hub that includes lifestyle benefits as one component of a larger strategy next to wellness challenges and ERG support.

Alternative #3: ThrivePass — Lifecycle benefits platform with LSA capabilities

What is ThrivePass best for?

ThrivePass is a broader benefits administration suite that may be ideal for organizations that want lifestyle spending-style benefits alongside broader benefit administration services, such as COBRA and pre-tax accounts.

ThrivePass positions itself as a “lifecycle benefits” platform. In addition to lifestyle spending accounts and stipends, it supports programs like COBRA administration, commuter benefits, tuition reimbursement, and other compliance-heavy offerings.

ThrivePass’s strengths

- Benefits suite that goes beyond LSAs

- COBRA administration expertise and transition tools

- Attractive to PEOs and midmarket companies managing complex benefit transitions

- Ability to consolidate multiple adjacent programs into one vendor

If your goal is reducing vendor count across several benefit types, not just lifestyle benefits such as stipends and LSAs, then ThrivePass can simplify procurement and contracting.

Tradeoffs to consider

- If your primary goal is running flexible LSAs efficiently, then broader suites like ThrivePass introduce complexity.

- The employee experience varies depending on which modules are activated.

- Reimbursement timelines and workflow friction are sometimes cited in online reviews when multiple programs intersect.

- Administrative workflows may require more onboarding compared to stipend-first platforms.

When ThrivePass makes sense

Consider ThrivePass when your organization wants to bundle lifestyle benefits with other compliance-driven programs like COBRA administration.

Alternative #4: Forma — Hybrid global wallet with marketplace and reimbursement options

What is Forma best for?

Forma is typically evaluated by larger or global organizations that want multiple ways for employees to spend benefits, including a debit card, reimbursements, and a curated vendor marketplace, within a single configurable wallet system.

It operates as a hybrid model (card + marketplace + reimbursement), supports employees in 110+ countries, and is often positioned as an enterprise-ready lifestyle benefits platform that also includes pre-tax accounts like HSAs, FSAs, HRAs, and commuter benefits.

Forma’s strengths

- Multiple spending methods (card, marketplace, reimbursement)

- Extensive global coverage (110+ countries)

- Configurable “wallets” and pooled funds

- Support for both pre-tax and post-tax benefit types

- May be attractive to larger enterprises with complex benefit structures

For organizations that want optionality and are comfortable managing several spending paths at once, this flexibility can be appealing.

Tradeoffs to consider

- Card-based components still rely on merchant-category enforcement and may result in checkout declines depending on merchant coding and eligibility rules.

- Marketplace models limit vendor flexibility compared to fully vendor-agnostic reimbursement programs.

- Managing multiple spending methods introduces administrative complexity.

- Employees often need guidance on when to use the card, submit a claim, or shop within the marketplace.

Hybrid models offer flexibility, but they also require extremely clear governance and communication. Your lifestyle benefits can be excellent and still fail if employees can’t figure out how to use them or frequently experience frustration when they try.

When Forma makes sense

Consider Forma if you want global coverage, a marketplace experience, and multiple spending methods in a single platform, particularly in more complex enterprise environments.

Which Benepass alternative is right for your team?

- Choose Compt if you want vendor-agnostic LSAs, reimbursement-first spending, predictable cash flow, and payroll-ready tax handling without prefunded cards.

- Choose Espresa if you’re looking for a broader culture and engagement platform that includes lifestyle benefits alongside community programs and well-being challenges.

- Choose ThrivePass if your goal is consolidating lifestyle benefits with compliance-heavy programs like COBRA or pre-tax accounts under one vendor.

- Choose Forma if you want multiple spending methods (card, marketplace, and reimbursements) and are comfortable managing a complicated hybrid model across a larger or global workforce.

Why HR and Finance teams choose Compt after evaluating Benepass alternatives

When teams move away from Benepass-style card programs, it’s usually for three reasons: prefunding exposure, merchant-code friction, or tax reconciliation headaches.

Compt solves those issues by removing the card entirely.

With a reimbursement-first model, you:

- Pay only for approved expenses — no prefunded balances.

- Get receipt-backed, payroll-ready tax classification

- Give employees vendor freedom without checkout declines.

- Run LSAs globally with multicurrency reimbursements.

- Manage approvals, reporting, and exports in one streamlined system that can handle stipends, LSAs, recognition and rewards, business expense management, company swag, and even employee discounts.

Compt is also less expensive and more cost-effective than Benepass, per recent calls our team has had with companies evaluating both Benepass and Compt in 2026.

Ultimately, the right choice depends on what you’re optimizing for. If your priority is a consolidated wallet that combines pre-tax and post-tax benefits on a debit card, a card-first platform like Benepass may be the right fit. But if you’re focused on simplifying administration, minimizing prefunding exposure, and running reimbursement-first LSAs with clean, payroll-ready tax handling, a more focused stipend-first platform will likely offer a more streamlined experience.

Compt was built by a three-time CFO and a two-time COO specifically for teams looking for flexible, vendor-agnostic lifestyle benefits with predictable cash flow and receipt-backed IRS compliance.

If you’re evaluating Benepass alternatives, request a Compt demo to see how tax-compliant, reimbursement-first lifestyle benefits work in practice.

FAQ: Benepass alternatives for stipends and LSAs

Compt, Forma, and Benepass approach lifestyle benefits from three different structural angles, and that ends up shaping everything else.

Benepass centers on a card-first wallet model, often paired with pre-tax accounts, where transactions are approved or declined in real time. Forma offers a hybrid model that combines card spending, marketplace purchasing, and reimbursements, which can appeal to larger organizations that want multiple spending paths inside one configurable system. Compt operates on a reimbursement-first model that is vendor-agnostic and purpose-built for flexible LSAs and stipends without prefunded debit cards.

In terms of coverage, Forma is known for broad global reach and advertises support in 110+ countries. Compt supports employees in 75+ countries with multicurrency reimbursements and centralized reporting. Card-based models can work globally, but real-world experience may vary depending on merchant acceptance, billing address matching, and currency conversion timing — G2 users cite many issues with using their LSA debit cards outside the U.S.

Pricing is typically custom across all three vendors. The bigger financial conversation, however, is often about total cost to launch. In one recent evaluation call, an HR leader shared that Benepass quoted their organization under 100 employees $15K before factoring in the actual stipend budget. When you’re still making the internal ROI case for launching an LSA at all, adding a five-figure platform fee can be difficult to justify.

Reimbursement-first programs like Compt also avoid prefunding card balances, which changes the working capital conversation in a way Finance teams tend to appreciate immediately.

What are the main differences between the leading LSA stipend platforms (Compt vs. Forma vs. Benepass, etc.) in terms of features, flexibility, and fees?

The main differences show up in how employees spend, how eligibility is enforced, and how cleanly expenses flow into payroll.

Benepass emphasizes debit card spending with approvals happening at checkout based on merchant category rules. Forma combines card, marketplace, and reimbursement options inside a configurable wallet system. Compt allows employees to spend with any vendor that fits employer-defined categories and submit receipts for review before payroll runs.

Flexibility tends to be highest in vendor-agnostic reimbursement models because employees are not limited by merchant coding or curated catalogs. Card-first and marketplace-driven systems introduce guardrails that feel streamlined in theory but create edge cases in practice.

Fees vary by configuration and headcount, but card-based models often add prefunding balances and card fees, which increases cash exposure compared to reimbursement-first platforms that reimburse only approved claims.

Does Compt do pre-tax accounts like HSA or FSA?

No. Compt doesn’t offer HSA, FSA, or HRA accounts. That’s not a missing feature — HSA/FSA administration is a fundamentally different regulatory and banking function than reimbursing flexible lifestyle spend, and most companies already have it covered through their health plan broker or a dedicated HSA custodian.

Benepass has leaned further into this space recently: it rolled out an integrated HSA investing experience in January 2026 with a $125 investment minimum, and more than 25% of Benepass HSA holders now invest their balances, compared to roughly 7–10% at traditional HSA providers. If consolidating pre-tax investing and post-tax stipends on one platform is your priority, that’s a genuine reason to lean toward Benepass. If you want flexible, vendor-agnostic LSAs without a card, most Compt customers simply run Compt alongside whatever HSA/FSA provider they already have.

Forma vs Compt vs Benepass comparison?

These platforms represent three distinct philosophies about how lifestyle benefits should work.

Benepass focuses on consolidated wallet convenience, especially for organizations that want pre-tax and post-tax benefits living on one card. Forma emphasizes optionality, giving employees multiple spending methods within a single system. Compt focuses on simplicity and flexibility by allowing employees to spend where they already shop and submitting receipts within clearly defined stipend categories.

If your priority is card consolidation, Benepass may align. If you want multiple configurable spending paths and enterprise-level flexibility, Forma may be a fit.

If you care most about vendor freedom, predictable cash flow, and payroll-ready tax handling without prefunded balances, Compt is purpose-built for that reality.

Compt vs. Benepass: which is better for flexible stipends?

For pure LSA and stipend administration, Compt wins on vendor flexibility, predictable cash flow, and global reimbursements. Benepass wins when you want pre-tax accounts and post-tax stipends consolidated on one card, or when checkout convenience matters more than vendor freedom. On cost, Compt customers evaluating both platforms have generally found Compt to be the less expensive option, particularly for smaller organizations, while Benepass’s platform-fee-plus-implementation structure adds up fast.

Ultimately, it comes down to architecture. Benepass is card-first: employees swipe a card, transactions approve or decline in real time against merchant-category rules, and the platform also handles pre-tax accounts like HSAs and FSAs. Compt is reimbursement-first: employees submit receipts against any vendor that fits policy, nothing gets declined at checkout, and there’s no prefunding.

Has anyone used Benepass or Compt for lifestyle benefits? What was your experience — any pros, cons, or issues we should know about?

Experiences tend to reflect the platform model more than the brand name.

Card-first platforms are often praised for the simplicity of swiping a card, but only when transactions approve cleanly. The common friction points tend to involve merchant category restrictions, declines at checkout, and inconsistencies for distributed and global teams. Reimbursement-first platforms are typically described as flexible and easier to reconcile because every expense is receipt-backed and categorized before payroll, which helps support IRS-aligned reporting.

The tradeoff with reimbursement is the receipt submission step. Most organizations find that small step worthwhile because it reduces compliance risk and eliminates checkout friction. If you want direct user sentiment, Compt maintains a 4.8 out of 5 star rating on G2, where customers consistently mention ease of use and administrative simplicity.

What are some good alternatives to Benepass for managing global Lifestyle Spending Accounts?

Common alternatives to Benepass include Compt, Forma, Espresa, and ThrivePass, depending on what you mean by “global.”

If global means supporting employees who spend locally in different currencies while maintaining centralized reporting, reimbursement-first platforms often scale more smoothly. Compt supports employees in 75+ countries with multicurrency reimbursements and does not rely on card acceptance networks or curated vendor coverage in each region.

Hybrid platforms like Forma may appeal to larger enterprises that want both global reach and multiple spending methods. The right choice depends on whether you prioritize debit card consolidation or vendor-agnostic flexibility across borders.

How does reimbursement stipends compare to card-based stipend platforms?

Card-based stipend platforms attempt to solve eligibility in real time at checkout. Transactions are approved or declined based on merchant category codes and predefined rules. When coding aligns, the experience feels seamless. When it does not, friction appears at the point of sale.

Reimbursement stipends shift the review process to after the purchase. Employees spend with vendors that fit policy and submit receipts for approval before payroll runs. This eliminates checkout declines and allows for clearer taxable vs. nontaxable classification.

The decision ultimately comes down to whether your organization prefers real-time swiping convenience or broader vendor flexibility with receipt-level compliance control.

Should we administer LSAs via reimbursement or card?

Reimbursement-based LSAs provide receipt-backed substantiation and clearer taxable and nontaxable separation before payroll, and eliminate the need to prefund balances. Employers reimburse approved claims rather than advancing funds.

Card-based LSAs offer real-time transaction approvals and a consolidated wellness wallet experience, often alongside pre-tax accounts. They typically require prefunding and rely on merchant category enforcement.

Organizations that prioritize predictable cash flow, audit readiness, and reduced administrative cleanup often prefer reimbursement-first models like Compt. Organizations focused on wallet consolidation may lean toward card-based options.

How to avoid card declines in stipend programs?

Card declines typically result from merchant category mismatches, insufficient prefunded balances, or eligibility rules that do not perfectly align with how merchants are coded.

Reducing declines involves clearly communicating eligible categories, auditing frequently declined merchants, refining configurations, and ensuring balances are funded correctly. However, because approvals occur at the merchant level rather than the item level, some edge cases are difficult to eliminate.

Reimbursement-first models remove this point-of-sale friction entirely because expenses are reviewed after purchase rather than approved at checkout.

Our LSA debit card is frequently declined; how can we reduce declines?

Frequent LSA debit card declines often indicate a structural mismatch between policy design and merchant coding. You can reduce friction by tightening category definitions, reviewing declined transaction patterns, clarifying billing address requirements for distributed teams, and improving employee education around LSA-eligible purchases.

Even with these adjustments, declines may persist because payment networks classify merchants broadly. If checkout friction continues to erode employee trust in the program, consider evaluating reimbursement-first platforms like Compt to eliminate point-of-sale approvals altogether.

Is a Lifestyle Spending Account platform better than giving everyone a corporate card for home-office and wellness expenses?

In most cases, yes. Corporate cards are designed for business expense management, not structured employee benefits administration. They often lack category-level governance, taxable vs. nontaxable clarity, and payroll-ready exports tied to benefit policies.

A Lifestyle Spending Account platform like Compt is built to manage eligibility groups, classify expenses appropriately, generate audit trails, and track participation and utilization. If your goal is delivering structured, policy-driven benefits rather than loosely managed reimbursements, an LSA platform provides far more control and visibility than issuing corporate cards for personal wellness or home-office expenses.

What is better: a perk marketplace, debit card, or a reimbursement model?

Each model optimizes for a different outcome, but in 2026 the more useful question is which model aligns with how your employees actually spend.

Marketplace-only systems provide curated vendor catalogs and negotiated discounts. They can feel polished, but they inherently limit choice. Compt customer benchmark data shows that employees spend across tens of thousands of unique vendors globally, with roughly 70% of stipend dollars flowing to local, regional, independent, or niche businesses rather than centralized marketplaces. When benefits force employees into a catalog, engagement often drops.

Debit cards prioritize immediacy, but merchant-category enforcement creates friction and edge cases. Reimbursement-first models prioritize flexibility and compliance by allowing employees to spend where they already shop and submit receipts within defined categories. This approach consistently drives strong participation because it mirrors real-life spending behavior.

What has evolved recently is the ability to combine flexibility with savings. With Compt’s embedded Employee Discounts powered by PerkSpot, employees keep full vendor freedom while optionally accessing negotiated deals. Discounts are discoverable and layered into the same system of record, rather than requiring a separate portal or additional vendor relationship. That combination allows organizations to stretch benefit dollars further without increasing budgets or adding administrative complexity.

For teams focused on participation, utilization, and consolidation, a reimbursement-first model with optional embedded discounts is often the most balanced and future-ready approach.