GLP-1 medications have quickly become one of the most complicated conversations happening in employee benefits in 2026. Employees want them. Physicians are prescribing them more frequently. And insurers are tightening coverage rules as demand continues to climb.

According to FAIR Health’s 2025 analysis of more than 51 billion commercial insurance claims, the share of adults prescribed a GLP-1 medication increased from 0.9% in 2019 to 4% in 2024. Survey data suggests the broader impact may be even larger: a 2025 KFF Health Tracking Poll found that about 1 in 8 U.S. adults (12%) report currently taking a GLP-1 drug for weight loss, diabetes, or another chronic condition.

Many insurance plans only cover these medications for diabetes indications. Others require strict prior authorization rules, BMI thresholds, or lifestyle program participation before coverage is approved. Medicare still carries a statutory exclusion for weight-loss medications, and Medicaid coverage varies by state.

Even where coverage technically exists, employees often face high out-of-pocket costs. In nationally representative polling by KFF, 54% of people who had taken a GLP-1 medication said it was difficult to afford.

For HR and Total Rewards teams, this creates a familiar tension: employees want support for a medication that can improve health outcomes, but expanding GLP-1 coverage through the medical plan can introduce unpredictable pharmacy costs and additional compliance complexity.

So companies are asking a practical question:

Is there a way to support employees who rely on GLP-1 medications without expanding the medical plan?

Increasingly, companies are experimenting with flexible lifestyle benefits like Lifestyle Spending Accounts (LSAs) and wellness stipends as one possible answer.

These programs don’t replace medical coverage. Instead, they complement it by giving employees a controlled allowance they can use toward eligible wellness expenses, which may include GLP-1 medications, while keeping spending capped and making benefits easier to administer.

What GLP-1 weight-loss coverage means in employee benefits

Before diving into the “how” of employee benefits program design, it helps to clarify the terminology.

In benefits conversations, GLP-1 weight-loss coverage usually refers to employer programs that help offset the cost of medications such as Wegovy, Ozempic, or Zepbound when they are prescribed for weight management.

Traditionally, those costs would be handled through the employer’s health plan or pharmacy benefit manager. But GLP-1 medications are expensive enough to significantly affect pharmacy spending.

Medicare Part D claims for GLP-1 drugs grew from 4.8 million in 2019 to 21.8 million in 2024, according to KFF analysis. Over the same period, gross spending rose fivefold, reaching $27.5 billion. Medicaid programs have seen similar growth, with prescriptions increasing sevenfold between 2019 and 2024.

With demand rising this quickly, many employers are hesitant to expand medical coverage without guardrails — which is why flexible lifestyle benefits are emerging as a practical alternative. Instead of creating a new health plan benefit, employers provide a defined reimbursement allowance employees can use across wellness-related expenses.

That approach keeps the benefit predictable for employers while still giving employees meaningful support.

Why employers are looking beyond traditional GLP-1 coverage

GLP-1 medications are effective for many patients — but they are also expensive. Retail prices often exceed $1,000 per month, and even after rebates, estimated net prices for some GLP-1 weight-management therapies still reach $7,400 to $9,190 per patient per year.

For employers considering full coverage under a medical plan, even modest adoption can affect their benefits budget. Modeling based on employer health policy research and ICER pricing benchmarks suggests that if 3–5% of employees use GLP-1 medications, incremental pharmacy spending could increase by roughly $20–$33 per employee per month across the entire workforce, depending on negotiated drug prices and adherence rates.

That expense is one reason many insurers and employers rely on strict eligibility criteria, including:

- BMI thresholds

- Documented comorbidities

- Prior authorization requirements

- Step therapy

- Response-based continuation rules

These guardrails certainly reduce costs, but they also create uneven employee access.

Flexible lifestyle benefits offer a different tradeoff. Instead of covering the medication itself through the health plan, employers offer a fixed allowance employees can apply toward wellness expenses, including GLP-1 medications if company policy allows.

In practice, many employers structure this support through taxable lifestyle benefits such as wellness stipends or Lifestyle Spending Accounts (LSAs), which allow companies to provide partial reimbursement for GLP-1 prescriptions while keeping employer costs capped and avoiding the regulatory complexity associated with expanding pharmacy benefits.

Why flexibility matters for employees

Behind the policy discussions are real people trying to maintain progress in their health journeys.

A former colleague once told me how much a GLP-1 medication had helped her improve her health over several months. Then, earlier this year, her employer changed their coverage policy. When the health plan stopped covering the medication for weight management, the treatment that had been working for her was financially out of reach.

Nothing about her health or the treatment plan had changed — only the coverage.

Stories like this are becoming increasingly common as insurers and employers tighten eligibility rules for GLP-1 medications, and that instability is one reason some employers are exploring flexible lifestyle benefits to complement traditional health coverage.

Instead of tying support for a specific medication to the health plan, employers can offer a defined allowance employees can apply toward wellness-related expenses, including weight management. The employer still maintains a predictable budget, while employees gain more flexibility in how they use the benefit.

Flexible reimbursement benefits also give employees more control over how they access support. Health needs can be personal, and many employees prefer submitting expenses privately through a benefits platform rather than navigating a highly visible process through managers or specialized vendor programs.

Using mental health as an example, Deloitte found that only 52% of Gen Z workers feel comfortable speaking openly with their manager about mental health challenges, with 27% worrying that managers would be judgmental and possibly discriminate, as reported by workforce analyst Mervyn Dinnen.

For employers, that structure creates a practical middle ground: employees get flexibility and discretion, while HR and Finance teams maintain oversight of program design and spending.

Three ways employers support GLP-1 costs today

Companies that want to support GLP-1 costs through lifestyle benefits generally take one of three approaches with Compt. Each option offers different levels of flexibility, structure, and administrative complexity.

Option A: Lifestyle Spending Accounts (LSAs)

A Lifestyle Spending Account (LSA) is one of the most flexible ways employers support GLP-1 weight-loss coverage without expanding their medical plan.

Common LSA categories include:

- Wellness

- Food

- Family

- Financial wellness

- Personal development

- Experiences

- Tech

- Home

Employees submit receipts for eligible expenses and receive reimbursement through the benefits platform. Within this structure, GLP-1 medications used for weight management can be included as an eligible expense under categories such as wellness or a dedicated category for weight management.

Many employers prefer LSAs because they consolidate multiple benefits into one program. Instead of offering a wellness stipend, professional development stipend, and family benefit individually, employers can bundle those programs into one flexible allowance.

LSAs are structured as taxable lifestyle benefits rather than medical plans, which means they generally avoid the ERISA requirements associated with employer-sponsored health coverage.

For HR and Finance teams, LSAs also provide centralized reporting and visibility into how employees actually use the benefit. Participation, spending patterns, and category trends can all be tracked in one place, making it easy to evaluate whether the program is meeting employee needs.

In Compt’s 2026 Annual Lifestyle Benefits Benchmark Report, all-inclusive LSAs were the most common stipend structure, with 64% of participating companies offering one, reflecting employers’ preference for flexible, multicategory benefits programs.

Option B: Wellness stipends

Another common approach is offering GLP-1 support through a wellness stipend. A wellness stipend uses the same reimbursement model as an LSA but is limited to wellness-related expenses. With Compt, employers can configure eligible wellness purchases and reimbursement rules within the platform.

Employees might use the benefit for:

- Gym memberships

- Fitness equipment

- Nutrition programs

- Supplements

- Mental health apps

- GLP-1 medications used for weight management

Because the benefit is narrower in scope than an LSA, wellness stipends are often easier for organizations to launch quickly.

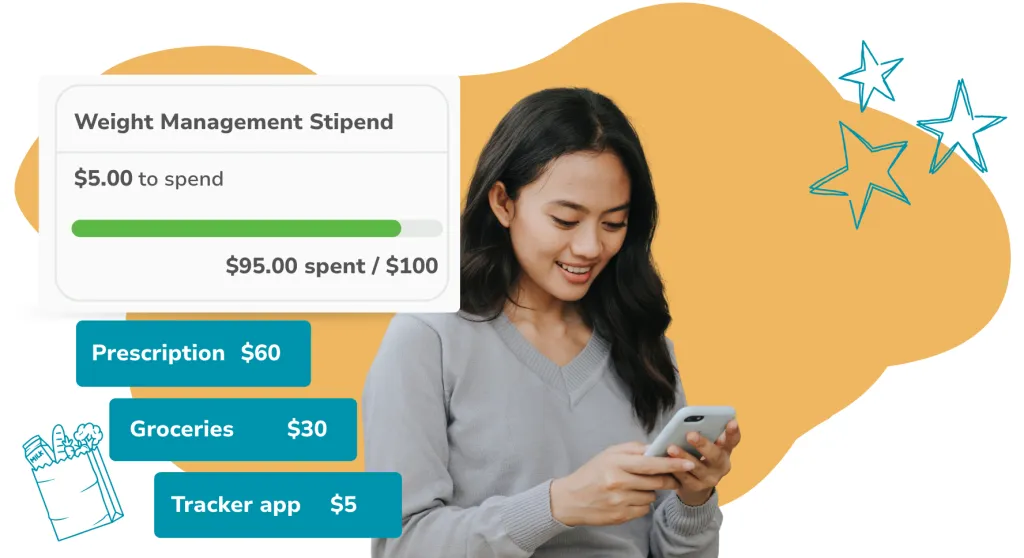

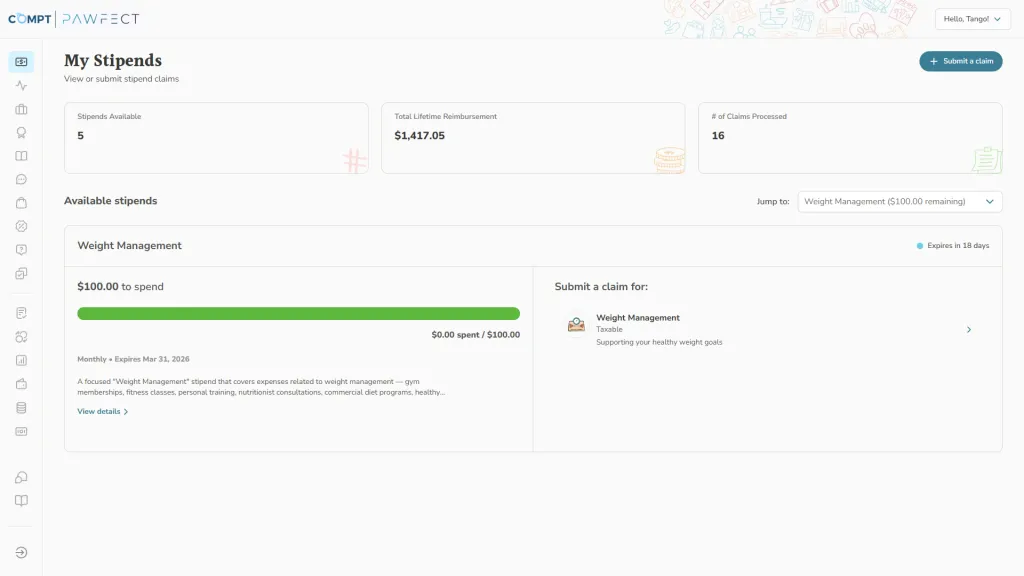

Option C: Weight-management stipends

Some employers choose a more targeted structure: a dedicated weight-management stipend. These programs still function as lifestyle benefits, but eligible expenses are focused specifically on weight management.

Examples may include:

- GLP-1 medications

- Nutrition coaching

- Metabolic health programs

- Weight-management services

- Fitness programs

This structure sends a clear signal about the company’s focus on metabolic health and support of weight management. Because the benefit is designed for employees actively seeking help in this area, utilization typically comes from a smaller subset of the workforce, which can lead to lower overall program spending compared with broader wellness stipends or LSAs that are relevant to nearly everyone.

However, this structure also requires careful design to ensure the benefit remains a lifestyle reimbursement program rather than a regulated health plan. Because the benefit is closely tied to health outcomes, some companies consult benefits counsel to ensure compliance.

Comparing the three approaches to GLP-1 weight-loss coverage

| Feature | Lifestyle Spending Account (LSA) | Wellness stipend | Weight-management stipend |

|---|---|---|---|

| Scope | Broad multicategory lifestyle benefit | Wellness expenses only | Weight-management expenses only |

| GLP-1 eligibility | Typically allowed if wellness is an included LSA category | Allowed as a wellness expense | Core eligible expense |

| Flexibility for employees | Very high | Moderate | Low |

| Employer cost control | Fixed allowance | Fixed allowance | Fixed allowance |

| Compliance posture | Taxable lifestyle benefit | Taxable lifestyle benefit | Taxable lifestyle benefit |

| Administration | Centralized benefit platform with reimbursement workflow | Reimbursement workflow | Reimbursement workflow |

| Time to launch | Fast | Very fast | Fast |

| Best fit | Companies consolidating multiple benefits | Companies offering wellness support | Companies targeting metabolic health or weight management specifically |

How LSAs compare to wellness stipends for GLP-1 coverage

The main difference between a Lifestyle Spending Account (LSA) and a wellness stipend is scope. A wellness stipend is limited to health-related expenses such as fitness, nutrition programs, or GLP-1 medications used for weight management.

An LSA allows employers to combine multiple benefits into one allowance, covering categories such as wellness, food, family, financial wellness, and personal development. For employers exploring GLP-1 reimbursement, LSAs often provide greater flexibility because the benefit can support weight management while still covering other lifestyle needs within the same program.

What about dedicated GLP-1 health benefits?

Some organizations explore offering GLP-1 reimbursement through a formal health plan or HRA. In those cases, the employer must establish plan documentation and comply with regulations such as ERISA, HIPAA, and COBRA.

Compt’s platform can support the technology side of these programs, including claims submission and balance tracking, but you as the employer would remain responsible for plan design, claims decisions, and compliance. Because of this complexity, many companies start with lifestyle benefits before considering a dedicated health plan.

How employers control GLP-1 benefit costs

One of the biggest concerns around GLP-1 benefits is cost. Lifestyle benefits help solve this by allowing employers to control spending through program design rather than relying on open-ended medical coverage.

Common cost-control strategies include:

- Fixed allowance caps: Employers set an annual or quarterly budget per employee, ensuring total program costs remain predictable.

- Quarterly funding: Instead of funding the entire allowance upfront, many organizations fund stipends quarterly to reduce financial exposure. This helps employers plan for recurring expenses.

- Flexible benefit categories: Allowing employees to spend their LSA or stipend allowance across multiple wellness needs naturally distributes demand rather than concentrating spending on one expense.

- Participation monitoring: Compt provides reporting that helps HR and Finance teams understand participation trends and adjust program design if needed.

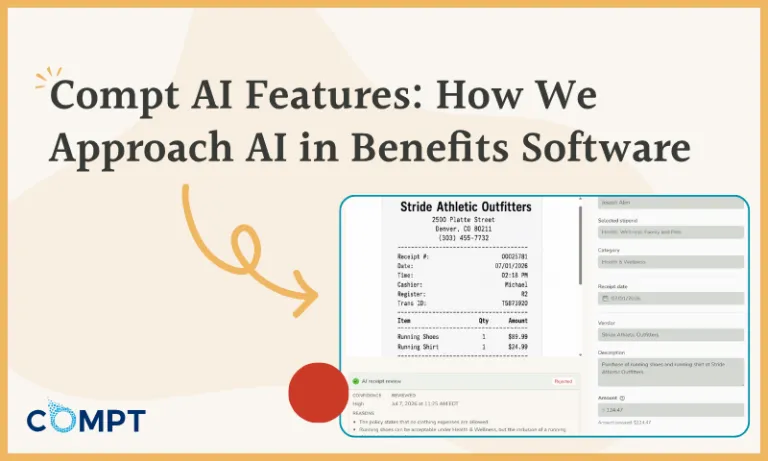

Offering GLP-1 support with Compt

As GLP-1 demand continues to grow, more HR, Total Rewards, and Finance leaders are looking for ways to support employees without dramatically increasing healthcare costs.

Compt helps organizations design and manage lifestyle benefits programs that make this possible. With Compt, employers can launch:

- Lifestyle Spending Accounts

- Wellness stipends

- Weight-management stipends

- And other stipends across many different benefits categories

Employees submit their receipts through Compt, while HR teams can see exactly how the benefit is being used and Finance teams keep a clear handle on budget and reporting. Instead of introducing another point solution or expanding the medical plan, organizations can support GLP-1 and other wellness needs through one flexible lifestyle benefits program.

Ready to see how it works? Request a demo of Compt today.

Need buy-in first? Download our GLP-1 one-pager to share with your team.

FAQs: GLP-1 weight-loss coverage with LSAs and stipends

Lifestyle Spending Accounts (LSAs) typically use a reimbursement model. Employees submit receipts for eligible purchases through the benefits platform, and approved expenses are reimbursed up to the employee’s available allowance.

When employers choose to allow GLP-1 medications as an eligible expense, the reimbursement usually falls under a broader category such as wellness or weight management included within the LSA. The employer defines the rules for eligibility and reimbursement, while the Compt platform manages receipt submission, approval workflows, and reporting.

Because LSAs are flexible by design, they allow companies to support GLP-1 costs alongside many other lifestyle benefits within a single program.

What kind of employee uptake should we expect if we let people use their wellness wallet for GLP-1 weight loss programs?

Actual utilization varies widely depending on eligibility rules, employee demographics, and how the benefit is structured. However, health policy modeling suggests that if even 3–5% of employees begin using GLP-1 medications through employer coverage, the financial impact can be extensive.

Employer-focused cost modeling based on ICER pricing benchmarks estimates that this level of adoption could increase pharmacy spending by roughly $20–$33 per employee per month across the entire workforce when GLP-1 medications are covered directly through the medical plan.

Because stipends and LSAs operate with fixed reimbursement caps, many employers find that lifestyle benefits provide a way to offer partial support without introducing open-ended cost exposure.

Could a Lifestyle Spending Account legally reimburse employees for GLP-1 weight-loss prescriptions like Wegovy, or does that have to run through the pharmacy benefit?

In many cases, employers can reimburse GLP-1 prescriptions through a lifestyle benefit such as an LSA or wellness stipend if the program is structured as a taxable reimbursement rather than a medical benefit.

These reimbursements are typically processed as lifestyle expenses instead of pharmacy claims. The employer sets the eligible expense rules, and employees submit receipts through the benefits platform.

Because the reimbursement is treated as taxable income rather than a health plan benefit, it generally does not need to run through the pharmacy benefit manager or the employer’s medical plan.

We’re expanding our wellness stipend — any best practices on capping reimbursements for GLP-1 drugs so costs don’t explode but employees still see support?

Most employers control costs by structuring the stipend as a fixed allowance rather than reimbursing the full cost of medication. For example, a company might provide a $1,000 to $2,000 annual wellness allowance that employees can apply toward a range of health-related expenses; the median per-employee annual wellness stipend in 2025 was $735, with some companies offering up to $36,000, per Compt’s 2026 Annual Lifestyle Benefits Benchmark Report.

This approach allows employees to use part of their allowance for GLP-1 medications if they choose, while still keeping total program costs predictable and reasonable for the employer.

Many organizations also distribute funding quarterly and allow the stipend to cover multiple wellness expenses so that spending is naturally distributed rather than concentrated on a single category.

Our HR team is debating whether to add coverage for GLP-1 weight loss meds like Ozempic to our wellness stipend—what do we need to think about cost, tax, and utilization-wise?

When evaluating GLP-1 support through a stipend or LSA, employers typically consider three main factors: cost predictability, tax treatment, and expected employee utilization.

Most lifestyle benefit reimbursements are treated as taxable income, which simplifies program administration compared to regulated medical plans. Employers also control costs by setting a fixed reimbursement allowance rather than covering the full cost of the medication.

Utilization will vary based on eligibility rules and employee demographics, but many organizations choose to position GLP-1 reimbursement within a broader wellness program so employees can apply the benefit to multiple health-related expenses.

What reporting and documentation do HR teams need when approving GLP-1 prescription reimbursements through a global lifestyle benefits wallet?

Most reimbursement programs, including Compt, require employees to submit documentation such as receipts or proof of purchase through the benefits platform. The platform then records the expense, reimbursement amount, and category classification.

For HR and Finance teams, reporting typically includes participation rates, reimbursement totals, and category-level spending trends. These insights help employers understand how employees are using the benefit and whether program design adjustments are needed.

Platforms like Compt centralize this reporting so organizations can manage lifestyle benefits consistently across distributed and global teams.

How are other hybrid tech companies fitting GLP-1 coverage into their taxable wellness allowances without triggering extra ERISA requirements?

Many companies are approaching GLP-1 support through taxable lifestyle benefits rather than expanding their medical plans. Programs such as wellness stipends or Lifestyle Spending Accounts (LSAs) provide employees with a fixed reimbursement allowance that can be used for eligible wellness expenses.

Because these programs are structured as taxable reimbursements instead of employer-sponsored health plans, they typically fall outside the ERISA requirements that govern traditional group health coverage. Employers define the eligible expense categories and reimbursement rules while keeping the benefit separate from the medical plan.

This approach allows companies to support employee wellness goals while maintaining a predictable benefits budget and avoiding the regulatory complexity that comes with expanding pharmacy benefits.