These days, any company that’s even remotely competitive offers employee benefits. A benefits package is with a doubt essential to an engaged workforce and happy employees. But it’s a little more complicated than just ‘giving employees stuff to make them happy.’

Depending on what kind of benefits you want to offer your employees, you can offer two main types: pre-tax and post-tax.

Pre-tax deductions offer immediate tax savings for the employee. That’s because any money put aside from their paycheck before taxes are taken out will result in a lower taxable income, potentially helping them be in a lower tax bracket and not have to pay as much on overall taxes.

Post-tax deductions don’t provide immediate tax relief for your employees. Instead, these benefits won’t be taxed when they use them in the future.

Pre-tax and post-tax deductions have their pros and cons. In this article, we’ll give you the ins and outs of each.

What are pre-tax benefits?

Pre-tax benefits are deductions an employer sets aside before calculating payroll taxes. With pre-tax deductions, employees pay lower taxes yearly because their taxable income is lower.

For example, if an employee set aside $100 for a pre-tax 401(k) plan, they only have to report $900 of their earnings as taxable income. So, instead of paying taxes on the full $1,000, they only have to pay taxes on $900.

Pre-tax deductions reduce income tax liability for employers and their employees in the near future.

However, employees sometimes owe taxes when they use the benefit they ‘prepaid’ for. For instance, the abovementioned 401(k) plan is taxed when the employee withdraws it in retirement.

Not all pre-tax deductions can be withheld entirely from federal income tax. Social Security, federal unemployment, and Medicare taxes still apply to adoption assistance and other childcare benefits.

Depending on the state, state and local taxes may also apply to pre-tax benefits. It is the employer’s responsibility to stay current with state and local tax laws.

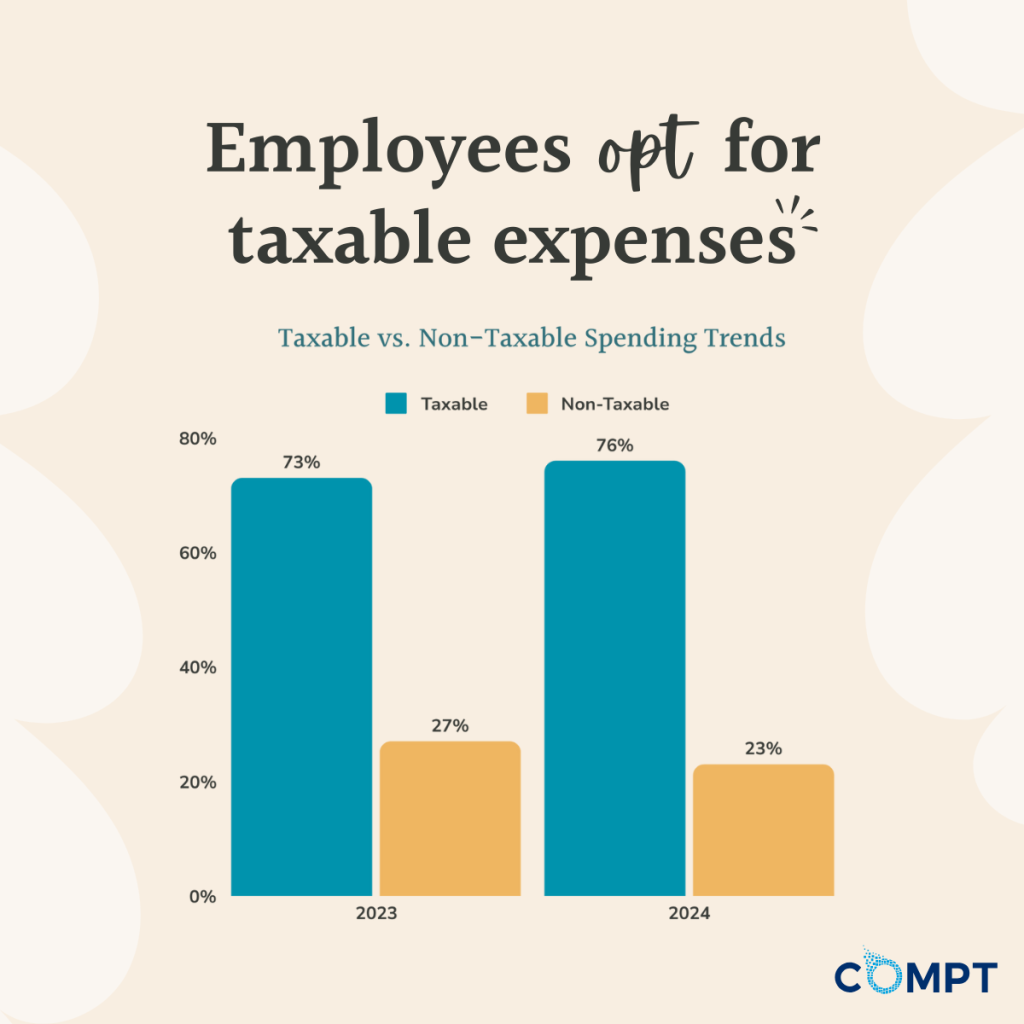

It’s something we keep a close eye on at Compt, where we specialize in building our software to be tax-compliant. In our latest Lifestyle Benefits Benchmark Report, we cotinually see that employees are opting for taxable expenses over non-taxable spending.

Types of Pre-Tax Benefits

For the most part, pre-tax benefits are the ones everyone’s heard of. The most common include health plans, retirement plans, disability insurance, and commuter benefits.

Health Plan Contributions

In 2024, 54% of U.S. firms offered health benefits to their employees. That puts health plan contributions among the most common pre-tax deductions. When employers set aside money for employee health plan premiums, they deduct those funds from total taxable income. Then, they’re paid to the health insurance provider (or savings account) directly.

Types of health plan contributions include:

- Employer-sponsored health plans: Employers provide health coverage to employees and their dependents. Standard employer-sponsored health plans include group, dental, and vision insurance. Typically, employers and employees split the cost of pre-tax premiums.

- Health savings account (HSA): Employees spend employer-provided funds on medical expenses for themselves and their families. Employers can set up a pre-tax HSA for employees who enroll in high-deductible health plans. In 2025, annual HSA contribution limits are rising to $4,300 (self-only coverage) and $8,550 (family coverage). To be eligible to contribute to an HSA, you must be enrolled in a High-Deductible Health Plan (HDHP). For 2025, the IRS defines an HDHP as a plan with a minimum annual deductible of $1,650 (self-only coverage) or $3,300 (family coverage) AND $8,300 (self-only coverage) or $16,600 (family coverage).

- Flexible spending account (FSA): Employees own the pre-tax funds set aside in an FSA. They can use this money to pay for dependent care expenses or qualified out-of-pocket medical expenses, like copays and prescriptions.

Psst: See more about the 2025 tax changes to fringe and lifestyle benefits in our updated blog.

Pre-Tax Retirement Plan Contributions

Employers offer retirement plans so employees can save up for their golden years. Employees make pre-tax contributions to their retirement plans, which they can withdraw money from when they’re older (59 1/2 for most plans).

Common retirement accounts with pre-tax payroll deductions include:

- Traditional IRAs

- Most 401(k)s

- 457s

- 403(b)s

Employer contributions are also available for retirement plans. They can match employee contributions up to a certain percentage of their salary. Vanguard data shows the most common match amount is 50%, up to 6% of the employee’s salary.

Using that as an example, if an employer matches 50% of an employee’s contributions and the employee makes $100,000/year, they’d get $500 for every $1,000 they contribute, up to $6,000 in total matched contributions.

Disability Insurance Contributions

Roughly 70 million U.S. adults have a disability. That’s about one-quarter of the entire adult population, and an even bigger proportion of the working-age population.

Disability insurance covers up to 60% of a worker’s salary (on average) if they become disabled and can’t work. Employers can set aside pre-tax dollars for disability insurance, which covers the cost of premiums.

There are two types of disability insurance:

- Short-term disability insurance: Employees receive a portion of their salary if they can’t work for weeks or months due to an illness or injury.

- Long-term disability insurance: Employees with disabilities for longer than 90 days receive monthly payments for a prolonged period, determined by the employer’s policy.

Note: Employees who wind up ill or injured after enrolling in pre-tax disability insurance will owe taxes on their monthly payments.

Commuter Benefits

Employers offer commuter benefits to support their in-office and hybrid employees’ daily commute to work. They’re some of the best benefits you can offer your employees – they stretch their dollar while they get to and from the office and provide alternative commuting options while reducing payroll taxes for the business.

Pre-tax benefits commuting programs cover include:

- Train, bus, and ferry passes

- Highway tolls

- Parking fees

- Carpooling/vanpooling expenses

With these benefits, employers can withhold up to $325 per month for employees’ transit expenses and a separate (i.e., additional) $325 per month for parking expenses on a pre-tax basis (for the 2025 tax year). Employees can access this money through a benefits card, prepaid pass, or reimbursement. See IRS Publication 15-B (2025) for more info.

Psst: Compt offers an easy way to offer commuter benefits to your employees through our platform. Learn more.

What are post-tax benefits?

Post-tax benefits are payroll deductions an employer sets aside after calculating payroll taxes. They reduce an employee’s net pay, not gross pay.

When employers deduct benefits from an employee’s paycheck on a post-tax basis, they (and their employees) pay more in income tax than they would with pre-tax benefits.

That’s because pre-tax benefits reduce the taxable income.

Some employees prefer post-tax benefits over pre-tax benefits that are tax-deferred rather than exempt. For example, someone who withdraws from a Roth 401(k) won’t need to pay taxes on the money when they withdraw it. All federal and state income taxes would have already been paid.

Types of Post-Tax Benefits

Although they don’t reduce an employee’s taxable income, post-tax payroll deductions give employees more control over their total compensation package. Many post-tax benefits allow employers to go above and beyond for their employees.

Post-Tax Retirement Contributions

Retirement accounts with after-tax deductions are great for employees who want to save up more money but don’t need the tax break that comes with pre-tax deductions.

There are three main types of post-tax retirement plans:

- Roth IRA: Employees pay income taxes on the money they contribute to a Roth IRA but not when they withdraw it.

- After-tax 401(k) options: Employees can save up pre-tax and after-tax money in the same account. After-tax 401(k) contributions happen after pre-tax payroll deductions and employer contributions, allowing employees to save more of their paycheck toward retirement.

- Roth 401(k): Employees contribute after payroll deductions, and the earnings grow tax-free (assuming no withdrawals before 59 1/2). The same limits that apply to a tax-deferred 401(k) apply to a Roth 401(k).

Note: Employees must specify post-tax contributions when they open their retirement plan accounts. Once saved in the account, these funds can’t be converted from pre-tax to post-tax.

Life Insurance

Company-sponsored life insurance policies allow employees to choose the coverage they want and make payments via payroll deduction on a post-tax basis. For employers, life insurance premiums are tax-deductible as business expenses.

Group-term life insurance is the most common type of employer-sponsored life insurance. Group-term life policies are pooled into a single policy and cover all employees in the group, offering death benefits for members who pass away while employed.

Employers offering group term coverage can deduct premiums paid on the first $50,000 of benefits per employee, but these deductions are made after tax.

Employee Stipends

A stipend is a lump-sum benefit an employer provides to cover the cost of meals, transportation, and other living expenses. It can range from $50 to over $200 monthly and helps employees pay for various out-of-pocket expenses.

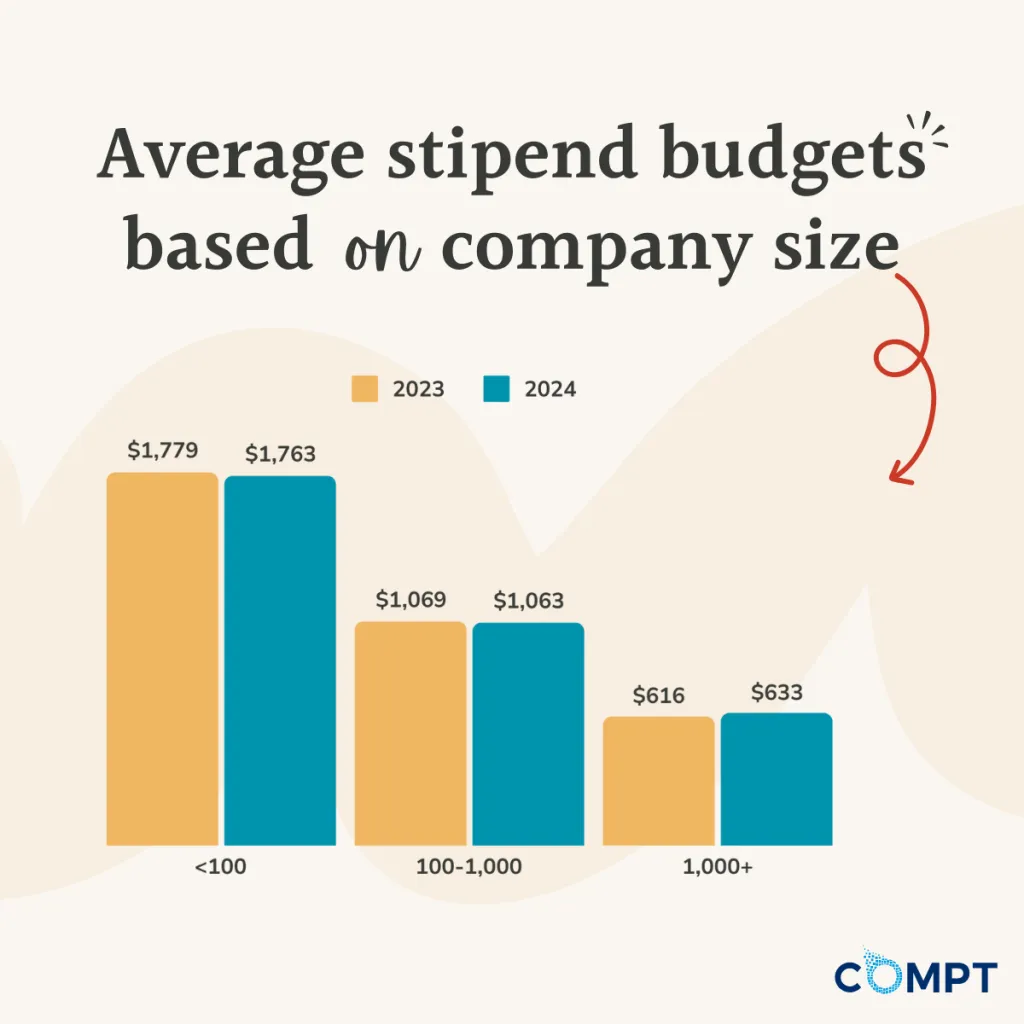

In our Lifestyle Benefits Benchmark Report, we saw these budgets range widely depending on company size, showing that no matter what your budget might be, there are tangible ways to support employees. Here’s a look at the latest findings:

Types of stipends include:

- Student loan repayment

- Career and professional development

- Relocation living expenses

- Meals and transportation

- Health and wellness

- Perk stipends

Note: Some stipends, for example, student loan repayment assistance, may be tax-exempt, so employees may be able to receive the fringe benefit tax-free (i.e. the reimbursement dollars are not considered taxable income).

Lifestyle Spending Accounts (LSAs)

A lifestyle spending account (LSA) is a post-tax benefit employers can offer to help employees manage A lifestyle spending account (LSA) is a post-tax benefit that’s growing in popularity — 38% are either planning to introduce LSAs (7%) or are considering adding them by 2025 (31%), indicating that by 2025, up to 45% of companies may offer LSAs.

Among Compt clients, 57% of all stipends already fall under the “LSA” category, according to our 2024 Mid-Year Lifestyle Benefits Report.

Employers can use an LSA offer to help employees manage healthcare, childcare, health and wellness, and education expenses (or anything else, really). They’re different from an HSA in that they’re designed for lifestyle benefits, not healthcare expenses and long-term savings. But they offer ultimate control over how and when employees use their benefits.

Employees can access funds in an LSA up to a certain dollar amount per year, and the account balance rolls over from one benefit year to the next. When employees spend money from LSAs, generally they pay income tax on them. Some benefits within an LSA can be considered tax-exempt according to the IRS.

Make tax compliance easy with Compt

We get it. Figuring out income tax deductions for employees is probably the hardest part of running payroll.

If you’re reading this thinking, “There’s no chance I’ll remember all these numbers, rules, details, and deadlines,” don’t worry. We do the heavy lifting for you. Our software is built for tax-compliance, taking all these rules and regulations under consideration so that you can adminster post-tax benefits to your people with ease.

We have 27 taxable and non-taxable categories, each with built-in (yes, you read that correctly) tax compliance.

We make sure you and your employees always get the most out of their lifestyle benefits – no guessing, no headaches. Schedule a demo with us to learn more.

Editor’s Notes: Compt software supports the categorization and proper reporting of benefits according to IRS guidelines, helping businesses maintain compliance. However, Compt cannot provide tax advice, and users should consult their own tax, legal, and accounting advisors when necessary.

Originally published in 2023, this post has been recently updated for clarity and relevance for our readers.