When it comes to company benefits, health savings accounts (HSAs) are typically known as the gold standard for health expense management.

- They’re tax-advantaged.

- Employers and employees can contribute.

- They stay with the employee, even if they leave the company.

Sounds good, right? But there’s a saying I’m pretty fond of:

What got us here won’t get us there.

And I think this is true of employers who are putting all their eggs in the more traditional benefits basket. They’re ignoring glaring realities:

- Employee demand from their employer to support them in all walks of life has changed. In fact, according to Mercer’s 2024 Global Talent Trends worth over $200,000.

You have the option to invest your contributions.

After reaching a certain balance, you can choose to invest a portion of your HSA funds for potential long-term growth. This makes them not just a short-term healthcare solution but also a long-term investment vehicle that can help fund healthcare in retirement.

And it actually works — HSA investment assets grew 20% during the first half of 2023.

There’s flexibility in how you use your funds.

Once you turn 65, you can withdraw HSA funds for non-medical expenses without facing a penalty (though the withdrawal will be taxed like regular income). And, unlike 401(k)s or IRAs, HSAs do not require mandatory withdrawals at age 72.

Where HSAs fall short

While they’re a fantastic solution to the ever-increasing healthcare costs in the US (and they do offer some flexibility compared to alternatives), they aren’t accessible to everyone on your team.

They also aren’t what your employees want for the kind of spending LSAs cover, like commuting, family care, and home office equipment.

An HDHP is a prerequisite for enrollment.

To open an HSA, you have to be enrolled in an HDHP, which requires you to pay a substantial amount out-of-pocket before your insurance kicks in. Employees on this plan can find healthcare costs more unpredictable and potentially unaffordable without significant savings or a high income.

Managing them is complicated.

Managing an HSA requires diligent record-keeping and an understanding of the IRS’s rules. You need to track your contributions, withdrawals, and receipts for eligible expenses to ensure compliance. Mistakes, like using funds for non-qualified expenses, can result in hefty penalties (20% before age 65) and taxes.

Psst: Learn more about taxable vs. non-taxable reimbursements.

They aren’t ideal for employees with chronic illnesses.

Ongoing medical conditions that require frequent doctor visits or prescriptions are challenging with an HSA. Since you have to meet the high deductible first, those without enough money will struggle to cover necessary treatments. The structure leaves some users facing medical debt rather than reaping the tax benefits.

Fees and account costs add up.

Depending on the provider, some HSAs charge maintenance or transaction fees. While they might seem tiny, they can add up, especially for those who aren’t able to maintain higher balances.

There are contribution limitations.

Contribution limits are set by the IRS and they aren’t enough to cover high medical costs for employees with serious health issues. At 65, after enrolling in Medicare, you can’t contribute to your HSA anymore, either (though you can still use the funds for medical expenses).

How LSAs fill in the gaps

Unlike an HSA, an LSA doesn’t facilitate long-term savings. When one of your employees leaves your company, they lose access to the LSA funds. It also isn’t meant to replace or compete with benefits like health coverage or 401(k)s.

LSAs are intentionally broader. Unlike HSAs, which are tied to healthcare expenses, they encompass things like gym memberships, financial coaching, daycare, pet care, and even home office equipment to address the varying needs of a diverse workforce.

Check out Compt’s Resource Library for our comprehensive Stipend Guides!

They meet employees where they are. Some of your team members might need access to mental health treatment, while financial resources or self-care make more sense for others. By allowing employees to choose how they use these funds, LSAs foster greater satisfaction and engagement at work . That’s why 85% of employees participate in LSA programs, on average.

Cut the red tape with LSAs. Unlike an HSA, which you have to fund first and then use for eligible expenses, LSAs require no upfront funding. Employers choose how much budget is available for LSAs, and it’s not funded until employees access and spend their LSA balance. Because of this, LSAs are available immediately for employees to use.

Provide meaningful benefits without dramatically increasing costs. Unlike salary raises or bonuses, LSA contributions are customizable and controllable. You can set annual spending caps, add or remove categories to accommodate your team’s changing needs, and even repurpose existing incentives/benefits to fund them.

We can help: Ready to offer LSAs to your people? Get in touch with Compt today.

Common misconceptions about LSAs (and the truth behind them)

As more and more companies adopt this model to complement traditional benefits, we’ve seen a few misconceptions here and there.

Let’s set the record straight.

Myth #1: “Regulatory complexity makes LSAs a challenge.”

LSAs are not automatically tax-advantaged in the way HSAs are (though there are still some components, like student loan repayment and commuter benefits, that aren’t taxable).

These are considered taxable income, so both the employer and employee have to pay their normal taxes.

It also means there’s actually far less red tape involved with implementation and management compared to other kinds of benefits.

Your team members can access LSAs without committing to a high-deductible health plan or any other insurance plan. And they can use them to cover a broad range of expenses, like counseling, home workout equipment, or childcare costs.

Myth #2: “Managing a budget for LSAs is complicated and risky.”

The flexibility LSAs offer makes them easier to budget for because there are more opportunities for savings and cost reduction. Major enterprises or local small businesses can use LSAs to structure a lifestyle benefits plan to meet your budget and employee needs.

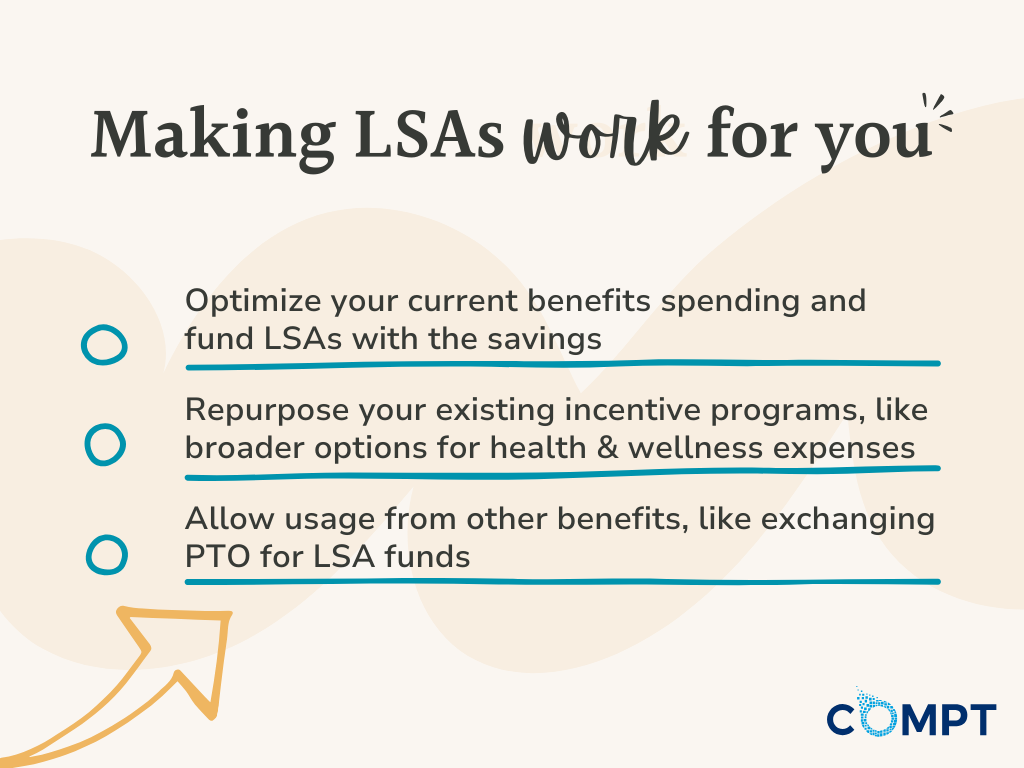

Even without making room in your budget, you could…

- Optimize your current benefits spending and fund LSAs with the savings. For example, by looking at rarely used benefits in categories that an LSA could easily cover. Or, by reallocating the budget from other perks that don’t align with your team’s preferences.

- Repurpose your existing incentive programs. If you already have some sort of well-being incentive, you can incorporate that into an LSA model that offers broader options for health and wellness expenses.

- Allow usage from other benefits. You might allow team members to exchange their unused PTO at the end of the year for LSA funds or use a portion of their bonus to contribute to their LSA balance.

Whatever you do, proper planning and clear guidelines can effectively control LSA spending. By setting fixed stipend amounts and clearly defining eligible expenses, you can eliminate the risk of overspending (or spending on the wrong things).

Myth #3: “LSA flexibility leads to a higher risk of misuse.”

While it’s true employees can spend LSA money on a wide array of expenses, there are limitations.

Through a software like Compt, employers can choose which categories or vendors to allow for spending, and they can apply controls like requiring itemized receipts for purchases.

You can further mitigate the risk by clearly communicating what’s an acceptable use of funds with your employees.

Myth #4: It is tough to make LSAs fair and equitable for all employees.

LSAs are actually one of the most inclusive employee benefits out there. Each team member gets to use their stipend on what they value most, and there’s no prerequisite (e.g., an HDHP) to receive them.

This means you can offer them to all your full-time employees, and they each get a personalized experience with the same budget. It also means you can better support diversity and inclusion goals by offering a range of benefits catering to their unique needs, regardless of demographics.

Ready to offer LSAs? Now’s the time…

Whether you have a global, local, or hybrid team, Compt’s stipend reimbursement platform makes it easy to set up a lifestyle spending account program that’s flexible enough to meet your team’s diverse needs but structured enough to align with your company’s goals and policies. Eliminate the ‘LSAs vs’ HSAs’ debate once and for all!

It also integrates with your accounting system, so you can handle tax compliance, and finance teams don’t have to bear the burden of constantly tracking and reporting usage.