Childcare benefits are employer-provided programs and resources that help working parents find, afford, and manage childcare — and for HR teams at companies with lean benefits operations, they’re one of the highest-impact benefits you can offer without adding significant administrative overhead.

The business case is straightforward: according to a February 2026 ReadyNation report, childcare challenges now cost U.S. employers an estimated $172 billion annually in lost earnings and productivity — up from $122 billion just three years ago. Care.com’s 2026 Cost of Care Report puts the employee side of that equation in sharp focus: parents now spend an average of 20% or more of household income on childcare, and 31% are dipping into savings to cover the expense. When that pressure goes unaddressed, it shows up as absenteeism, turnover, and reduced focus across your workforce.

This guide covers the main types of childcare benefits, what they cost, how they’re taxed, and how to structure a program your Finance team can actually defend.

What are childcare benefits?

Childcare benefits are employer-provided programs and resources that help working parents find, afford, and manage childcare during the workday. They include financial support like family stipends and dependent care FSAs, as well as structural support like backup care and flexible scheduling.

And childcare benefits are still far from universal. According to the Bureau of Labor Statistics’ March 2025 Employee Benefits Survey, just 13% of private industry workers have access to employer-provided childcare benefits — though that number jumps to 30% at companies with 500 or more employees. For HR leaders at mid-to-large companies, that gap represents both a real employee need and a genuine competitive differentiator.

Types of childcare benefits for employees

Childcare subsidies

Childcare subsidies are direct financial assistance programs — funded by employers, state governments, or both — that help cover the cost of childcare for eligible working parents. State-administered subsidies are federally funded and vary by eligibility criteria, but can cover in-home care, licensed childcare centers, or both.

Employers can also provide childcare subsidies directly, such as daycare tuition reimbursement, to support employees who struggle to cover care costs on their own.

Since 2001, the IRS has incentivized employer-provided childcare through the Employer-Provided Childcare Credit (45F). Following updates in the One Big Beautiful Bill Act, the maximum credit is now $500,000 for standard businesses and $600,000 for small businesses — a significant increase from the previous $150,000 cap. The credit covers 40% (50% for small businesses) of qualified childcare facility expenditures, plus 10% of qualified resource and referral expenditures.

Qualified expenditures include costs for acquiring, constructing, or expanding a childcare facility; employee training, scholarships, and compensation for trained childcare staff; and payments for employee childcare resource and referral services. Facilities must comply with state and local licensing requirements and primarily serve employees’ dependents.

On-site daycare

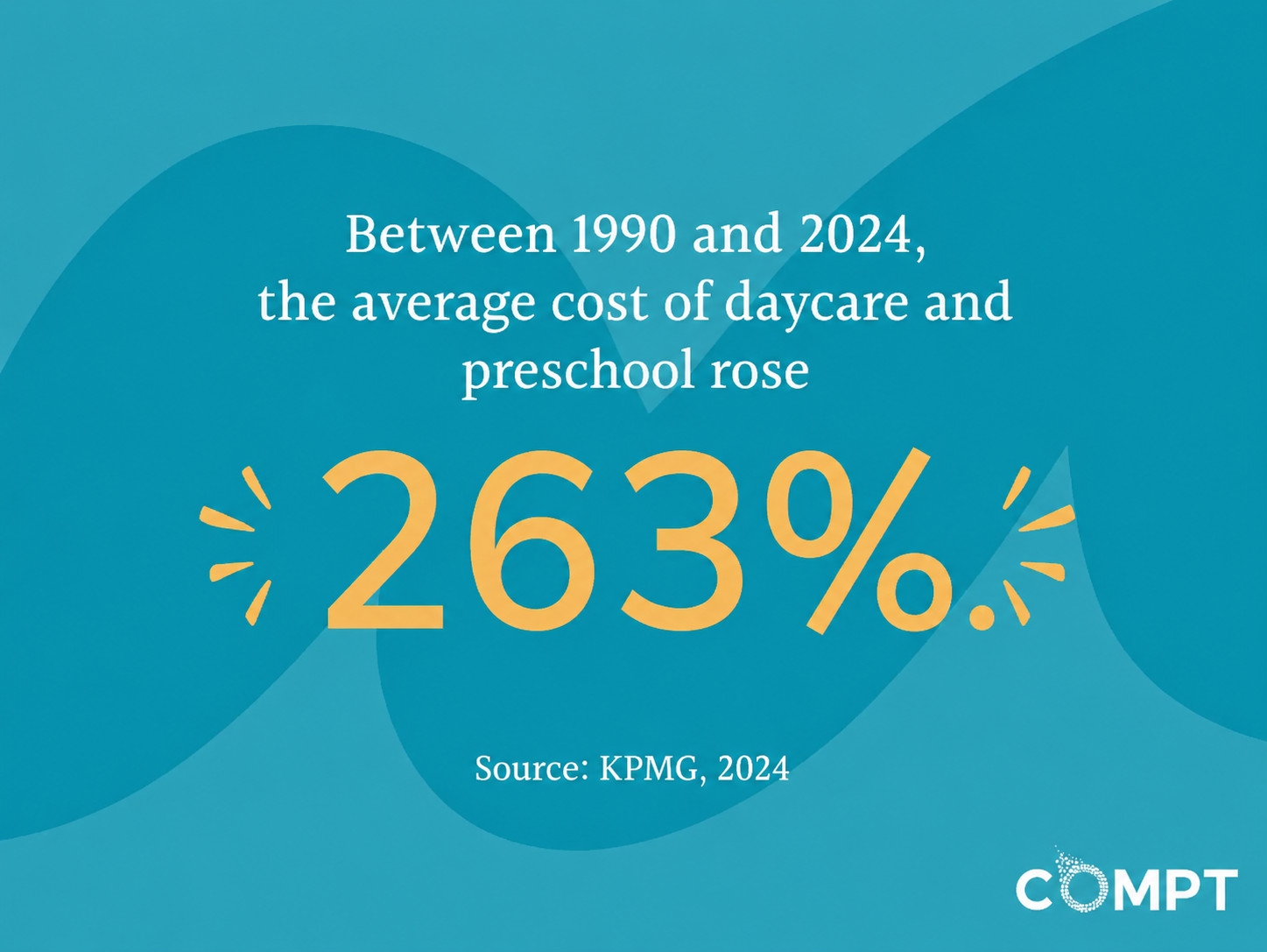

Between 1990 and 2024, the average cost of daycare and preschool rose 263% — nearly double the pace of overall inflation. For companies with the space and infrastructure to support it, on-site daycare is one of the most comprehensive childcare benefits available. It eases separation anxiety for working parents, reduces tardiness and absenteeism tied to childcare logistics, and makes infant care more manageable for new mothers returning to work. It also tends to build a stronger sense of community and shared support among employees.

It’s worth noting that not every company can offer on-site daycare; it requires significant upfront investment in space and operations. For employers who do own the facility, it may also qualify for the expanded Employer-Provided Childcare Credit covered in the subsidies section above.

Family stipends

A family stipend is a fixed employer-funded budget that employees can use for family-related expenses such as childcare, elder care, family building, enrichment activities, and more. Unlike targeted benefits like Dependent Care FSAs, stipends give employees the flexibility to use funds however they choose within employer-defined categories.

According to the 2026 Annual Lifestyle Benefits Benchmark Report, the median annual funding for family and caregiving stipends is $2,500 per employee, with programs ranging from $1,000 to $12,000 depending on company size and structure. Employee participation in caregiving stipends averages 78%, reflecting strong engagement, even though utilization tends to be lower because these benefits are often situational rather than recurring monthly expenses.

Compt’s family stipend lifestyle benefits programs support three distinct use cases, which can be offered separately or bundled under a single program:

- Family building stipend: Covers IVF, IUI, egg and sperm freezing, surrogacy, adoption fees, and genetic testing. Fills the gap where most health insurance stops and is inclusive of LGBTQ+ paths to parenthood.

- Caregiving stipend: Covers childcare, after-school programs, elder care, and functional needs support. Particularly valuable for working parents: childcare costs now exceed rent in most U.S. metros.

- Family stipend: Covers the everyday costs of raising a family: summer camp, sports, tutoring, school supplies, and extracurriculars. Typically the highest adoption of the three and a strong starting point before expanding into caregiving or family building.

For HR teams managing lean operations, all three can be administered in about 30 minutes a month through a single platform with IRS-compliant, receipt-based reimbursement, automated tax treatment, and a simple payroll sync.

Paid family leave

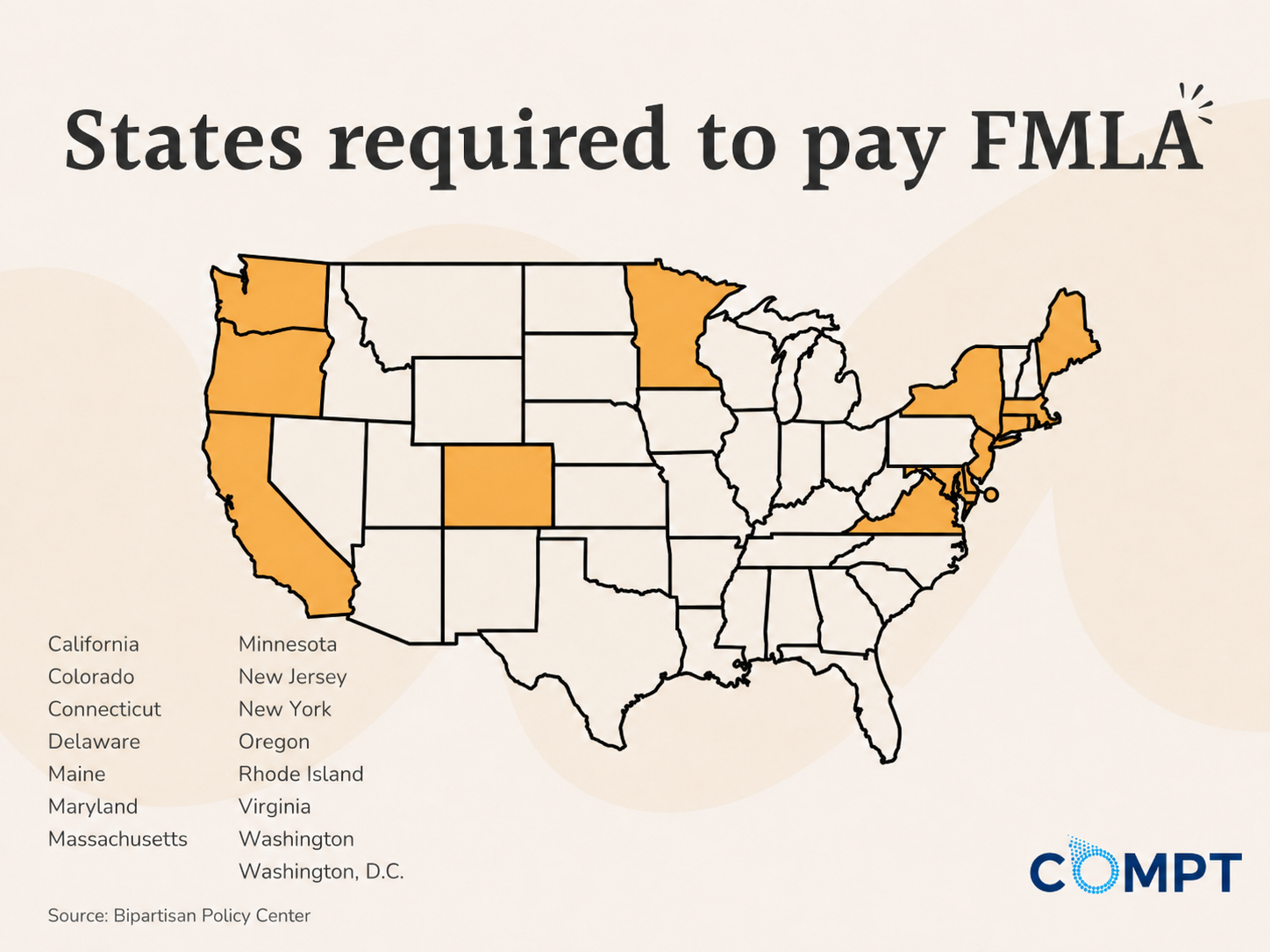

The U.S. remains the only industrialized country without a federal paid family leave guarantee. The Family and Medical Leave Act (FMLA) requires companies with 50 or more employees to provide up to 12 weeks of unpaid, job-protected leave per year — but no wage replacement.

As of 2026, 14 states and Washington, D.C. have enacted mandatory paid family leave programs. Those states are:

- California

- Colorado

- Connecticut

- Delaware

- Maine

- Maryland

- Massachusetts

- Minnesota

- New Jersey

- New York

- Oregon

- Rhode Island

- Virginia (contributions begin in 2028)

- Washington

For employers outside these states, paid family leave remains voluntary. According to the most recent Bureau of Labor Statistics data, just 27% of private sector workers have access to paid family leave — meaning nearly 3 in 4 do not.

Despite that gap, momentum is building. The International Foundation of Employee Benefit Plans reported that the share of employers offering paid adoption leave rose from 27% in 2020 to 37% in 2024. Employers who voluntarily offer paid leave — including parental, adoption, and caregiver leave — consistently cite it as one of the most impactful retention tools available, particularly for employees planning or growing families.

Dependent Care FSA

A Dependent Care Flexible Spending Account (FSA) allows working parents to set aside pre-tax dollars from each paycheck to cover eligible dependent care expenses such as daycare, preschool, after-school programs, and summer day camps (summer school is not included). Funds can only be used for children under 13 or adults who are unable to care for themselves and are claimed as dependents on your taxes.

Effective January 1, 2026, the contribution limit increased to $7,500 per household — the first increase in 25 years, following the One Big Beautiful Bill Act. The limit is $3,750 for married individuals filing separately. Dependent Care FSAs remain use-it-or-lose-it: unused funds do not roll over into the next plan year.

Backup childcare

Finding childcare at the last minute is one of the most stressful challenges working parents face, which is why many employers arrange backup care as a standing benefit. When a child is home sick or a regular daycare closes unexpectedly, employees can request in-home backup care such as a babysitter or nanny, or access a childcare center their employer has reserved capacity at for exactly these situations.

Flexible work arrangements

Flexible work arrangements — remote work, hybrid schedules, compressed workweeks — are among the most accessible childcare benefits an employer can offer, and one of the few that cost nothing to implement. The ability to work from home allows parents to manage school drop-offs and pickups without sacrificing focus during core work hours, reducing the scheduling pressure that often drives absenteeism and attrition among working parents.

Comparison table: Which childcare benefits can employers offer, and how are they taxed? (2026)

| Benefit type | Structure | Tax treatment | Best for … | Does Compt support it? |

|---|---|---|---|---|

| Childcare subsidy | Employer-funded direct assistance or tuition reimbursement | Taxable unless structured through a qualified plan | Employers who want to directly offset employee childcare costs | Yes — via reimbursement-based family or caregiving stipend |

| On-site daycare | Employer-operated facility at or near the workplace | Nontaxable to employees; employer may claim 45F credit | Large employers with space and infrastructure to support it | No — Compt supports the reimbursement layer, not facility operations |

| Family stipend | Fixed employer-funded budget; employee submits receipts for reimbursement | Taxable | Employers who want flexible, broad family support across childcare, eldercare, and family building | Yes — core Compt use case |

| Dependent Care FSA | Employee pre-tax contributions up to $7,500/household | Nontaxable (pre-tax) | Employers and employees looking for a tax-advantaged way to cover predictable childcare costs | No — FSAs require a separate plan administrator |

| Backup childcare | Employer-arranged emergency care network or in-home care | Taxable | Employers with shift-based or inflexible schedules where unexpected care gaps create real productivity risk | Yes — via reimbursement-based caregiving stipend |

| Paid family leave | Wage replacement during leave; may be state-mandated or voluntary | Taxable | All employers; especially valuable for retention of new parents | No — leave administration falls outside Compt’s scope |

| Flexible work arrangements | Schedule or location flexibility; no direct financial component | N/A | Employers where role type allows it; high-impact, zero-cost option | No — not a financial benefit |

Why you should offer childcare benefits for employees

For HR leaders managing lean teams, childcare benefits aren’t just a retention play — they’re one of the highest-ROI investments in your benefits stack. A 2024 report by Boston Consulting Group and Moms First found that childcare benefits deliver returns of 90% to 425% of their cost across companies of different sizes and industries. The break-even point is remarkably low: retaining as few as 1% of eligible employees can cover the cost of offering the benefit to everyone who qualifies.

Employers who support working parents see measurable operational benefits:

- Higher engagement and morale

- Lower absenteeism

- Lower voluntary turnover

- Fewer instances of burnout among working parents

- Greater loyalty to the company and its leadership

- Stronger recruitment — top talent actively seeks out family-friendly employers

There’s also a significant tax advantage worth flagging for Finance. Dependent Care FSAs reduce taxable income for employees and lower FICA and payroll tax obligations for the employer. Employer childcare subsidies structured through a qualified plan, and the expanded 45F credit for on-site facilities, add further defensibility to the investment.

For companies competing for talent, childcare benefits remain far from standard. That gap is a genuine differentiator for HR teams willing to offer them.

How HR teams use Compt to offer childcare benefits

Childcare benefits are one of the highest-impact investments an HR team can make — and one of the most practical to implement. Compt’s family and caregiving stipends let you launch a reimbursement-based childcare benefit in under two weeks, with automated tax treatment, one-click payroll sync, and no prefunding required. You set the budget and the eligible categories; employees submit receipts and get reimbursed through payroll.

Request a Compt demo today to see for yourself.

FAQ: Childcare benefits for employees

Compt’s all-inclusive Lifestyle Spending Account is built specifically for this use case — wellness, family and caregiving, professional development, and other categories can all live under one program, with employees submitting receipts for whatever applies to them. You set the budget and eligible categories; Compt handles receipt review, tax classification, and payroll sync.

According to the Compt 2026 Annual Lifestyle Benefits Benchmark Report, all-inclusive LSAs see 93% participation and 89% utilization — the highest of any benefits structure.

Are Lifestyle Spending Accounts post-tax benefits in the U.S., and what varies by jurisdiction?

Compt’s guide to LSA tax treatment covers this in detail, but in most cases, yes — LSA reimbursements for personal lifestyle expenses such as wellness, family care, and enrichment activities are taxable income for employees in the U.S. Some categories, including professional development and work-related equipment, may qualify for nontaxable treatment depending on how the program is structured.

Tax treatment can vary by state and country, so HR teams managing multistate or global workforces should confirm classification with a tax advisor and use a platform like Compt, which automates taxable vs. nontaxable categorization.

We’re moving to remote work and need software that can manage elder care stipends alongside our wellness and learning perks — what platforms can handle reimbursements, tax compliance, and global teams?

Compt supports caregiving stipends — including elder care, childcare, and family building — alongside wellness, professional development, and remote work benefits in a single platform. Reimbursements are processed through payroll with automated tax treatment, and the platform operates in 75+ countries. For global teams, Compt handles local currency reimbursements without requiring separate vendor relationships or manual reconciliation.

What are the best platforms for elder care Lifestyle Spending Accounts?

Compt’s caregiving stipend supports elder care, childcare, functional needs assistance, and other dependent care expenses under a single reimbursement-based program. Employees submit receipts for eligible expenses and are reimbursed through payroll, with tax treatment handled automatically.

The Compt 2026 Annual Lifestyle Benefits Benchmark Report found family and caregiving stipends average 78% participation, reflecting strong engagement even though usage tends to be situational rather than recurring monthly.

How to get CFO approval for lifestyle stipends?

Compt’s reimbursement-based model is the strongest CFO argument for lifestyle stipends: unlike prefunded wallets or fixed perks, companies only pay for what employees actually spend. A 2024 report by Boston Consulting Group and Moms First found that childcare benefits alone deliver ROI of 90% to 425% of their cost, with the break-even point as low as retaining 1% of eligible employees. Framing the ask around turnover cost avoidance and zero-waste spending — rather than headcount cost — tends to land better with Finance.

Help me build a business case for switching from point-solution perks to a single perk stipend platform?

Compt’s guide to comparing perks software walks through this in detail, but the core argument is operational: managing separate vendors for wellness, childcare, professional development, and other benefits multiplies admin work, invoice reconciliation, and compliance exposure without improving the employee experience.

A consolidated LSA from Compt replaces multiple point solutions with one reimbursement workflow, one payroll sync, and one reporting view for Finance. According to Compt’s 2026 Annual Lifestyle Benefits Benchmark Report, 64% of employers in our database now use an all-inclusive LSA — up from 55% the prior year — reflecting how quickly the market has shifted away from point solutions.

Editor’s note: Compt software supports the categorization and proper reporting of benefits according to IRS guidelines, helping businesses maintain compliance. However, Compt cannot provide tax advice, and users should consult their own tax, legal, and accounting advisors when necessary.

Editor’s note: Originally published in 2023, this post has been recently updated for clarity and relevance for our readers.