Fringe benefits are a core part of how companies support employees beyond base salary. These employer-provided perks — from health insurance and retirement plans to stipends, reimbursements, and lifestyle benefits — help employees manage real-life needs outside of work, improving well-being while strengthening retention and engagement.

In an era when employees feel more disconnected from their jobs than ever before, Gallup reports that better pay and benefits are one of the top drivers of job switching, with 54% of employees saying they are very important when considering a new opportunity.

For employers, fringe benefits have become a practical way to strengthen compensation packages without relying entirely on salary increases. As economic uncertainty rises, well-designed benefits programs help organizations stay competitive while keeping compensation spending predictable.

In this guide, we’ll explain what fringe benefits are, how they work, examples of common programs, and how employers calculate and manage them.

What are employee fringe benefits?

Fringe benefits are perks an employer offers to employees in addition to their base salary. These benefits can be monetary or nonmonetary and may include offerings such as health insurance, wellness stipends, paid time off, childcare support, retirement contributions, and other employer-sponsored programs.

Fringe benefits vary widely by employer, industry, company size, and workforce needs, according to Compt’s 2026 Annual Lifestyle Benefits Benchmark Report. Some organizations focus on traditional benefits like insurance and retirement plans, while others offer more flexible programs designed to support employees’ well-being, professional development, or family needs.

Common examples of employee fringe benefits

Fringe benefits come in many forms, from traditional employer-sponsored programs to newer, more flexible benefits designed to support employees’ everyday needs.

According to the U.S. Bureau of Labor Statistics (BLS), fringe benefits account for roughly 29-30% of total employee compensation costs for private industry employers, highlighting how central benefits have become to modern compensation packages.

Below are some of the most common examples of fringe benefits offered by employers today.

Health insurance

Health insurance is one of the most important benefits employees look for when considering a job. Employer-sponsored health plans help employees access care at significantly lower costs and often extend coverage to spouses and dependents.

Many employers also offer complementary health benefits such as Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs), which are tax-advantaged accounts that allow employees to set aside pre-tax funds for qualifying medical expenses.

Paid time off (PTO)

While paid time off (PTO) is a standard employee fringe benefit, when supplemented by other intentional wellness supports, it can have a real impact.

The benefits of taking time away from work show up for employees and their teams by increasing engagement, reducing absenteeism, and minimizing turnover.

A 2025 study by Florida Atlantic University and Cleveland State University found that offering PTO reduces the likelihood of quitting by 35% overall, with a greater reduction for men (41%) than women (25%).

Financial wellness and retirement benefits

Financial wellness programs help employees build long-term financial stability. These programs often include educational resources such as budgeting tools, financial planning guidance, and access to services like debt management, credit-building support, wage advances, and financial counseling.

In addition, most companies offer retirement plans such as 401(k) or 403(b) accounts with employer contribution matching.

According to Vanguard’s 2025 How America Saves report, many employers are also expanding support beyond the traditional “set-it-and-forget-it” retirement model. The report found that 67% of participants are invested in professionally managed allocations, helping employees make more informed investment decisions.

Paid parental leave

One of the most sought-after fringe benefits employees seek is paid parental leave. 2024 research from Parentaly found that 94% of women consider a company’s parental leave policy when accepting an offer, so if you don’t offer any sort of paid parental benefit, you’re definitely losing top talent to companies that do.

Yet, according to the Center for American Progress, only 27% of private-sector workers have access to it. Offering paid parental leave and other family-friendly benefits demonstrates that you as an employer support employees through major life transitions and can strengthen both recruitment and retention.

Paid leave is typically 12–16 weeks, and some packages allow new parents to take additional time off if necessary. Regarding compensation, companies often offer employees about two-thirds of their original pay while they are on leave. Some companies provide full compensation during paid leave in the spirit of delivering the most attractive package.

Paid parental leave should be a benefit inclusive of all employees, so don’t forget about adoptive parents, same-sex couples, blended and step families, and single fathers!

Provide inclusive family benefits with stipends.

Learn practical ways to address pay inequity and offer inclusive family stipends that support women.

Lifestyle Spending Accounts

A Lifestyle Spending Account (LSA) is an employer-funded benefit that reimburses employees for approved lifestyle expenses across categories defined by the employer. LSAs are often used to support a wide range of employee needs, including wellness programs, professional development, family care, food and groceries, company swag, and everyday lifestyle expenses.

Because LSAs are flexible by design, employees can apply funds toward resources that support their well-being, such as therapy, fitness programs, mindfulness apps, or other wellness-related expenses.

Compt’s 2026 Annual Lifestyle Benefits Benchmark Report highlights a clear market preference for all-inclusive LSAs that reduce administrative friction and support a range of employee and culture needs:

- 64% of Compt customers using an all-inclusive LSA as their primary fringe benefits program

- 93% employee participation

- 89% utilization of issued funds

- $1,200 median annual funding for all-inclusive LSAs

- 78% of spending classified as taxable and 22% as nontaxable

- 70% of spend across 64,000+ vendors going to local, regional, niche, or independent merchants

When intentionally funded, both in terms of what’s offered and how frequently it’s funded, an LSA can also influence whether employees actually use the benefits available to them.

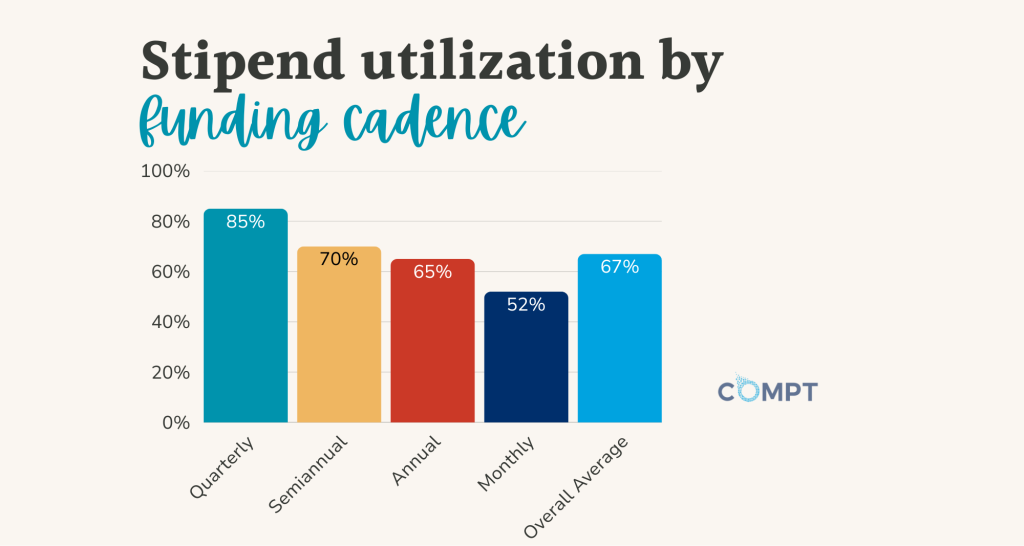

LSA utilization by funding cadence (2025)

- Quarterly: 85% utilization

- Semiannual: 70% utilization

- Annual: 65% utilization

- Monthly: 52% utilization

- Overall average: 67% utilization

Benchmark data also suggests that wellness benefits see higher engagement when delivered within broader flexible benefits programs. Our 2026 Annual Lifestyle Benefits Benchmark Report found that wellness benefits reached 86% utilization when delivered through an LSA, compared to 62% utilization when offered as a standalone stipend.

While LSAs can be a strong fit for many organizations, they also introduce tax and administrative considerations. Because most LSAs include a mix of taxable and nontaxable fringe benefits, employers need clear policies and transparent expense management to ensure compliance. Luckily, Compt is built to address these risks directly.

Employee stipend categories

Stipends are employer-funded fringe benefits that provide employees with a fixed budget to spend within a defined benefit category.

At Compt, we offer 30+ categories designed to give employers flexibility while ensuring benefits support employees’ real-world needs.

Compt’s stipend categories include:

- Wellness

- Family care

- Elder care

- Food

- Work-from-home expenses

- Business travel

- Cell phone

- Professional development

- Charitable giving

- Pets

- Productivity tools

- Student loan repayment

While many stipend categories exist, benchmarking data shows employees tend to prioritize benefits that support essential, everyday needs.

Top stipend category utilization (2025)

- All-inclusive LSAs: 64%

- Health and wellness: 37%

- Office equipment: 25%

- Professional development: 20%

- Cell phone and internet: 15%

- Commuter benefits: 8%

- Food stipends: 7%

Commuter and food stipends often appear as narrower, role- or location-specific benefits rather than universal programs offered across an entire workforce, and they’re also often included in LSAs rather than offered separately.

Federally mandated benefits

In the U.S., federal law mandates certain payments, including Social Security and Medicare taxes, unemployment insurance, and workers’ compensation. Employers with 50 or more employees must also comply with ACA health coverage requirements and FMLA leave protections. Some states also mandate disability insurance.

These legally required payments are sometimes discussed alongside fringe benefits because they are part of total compensation, but they are generally categorized separately from voluntary employer-provided fringe benefits.

How fringe benefits work

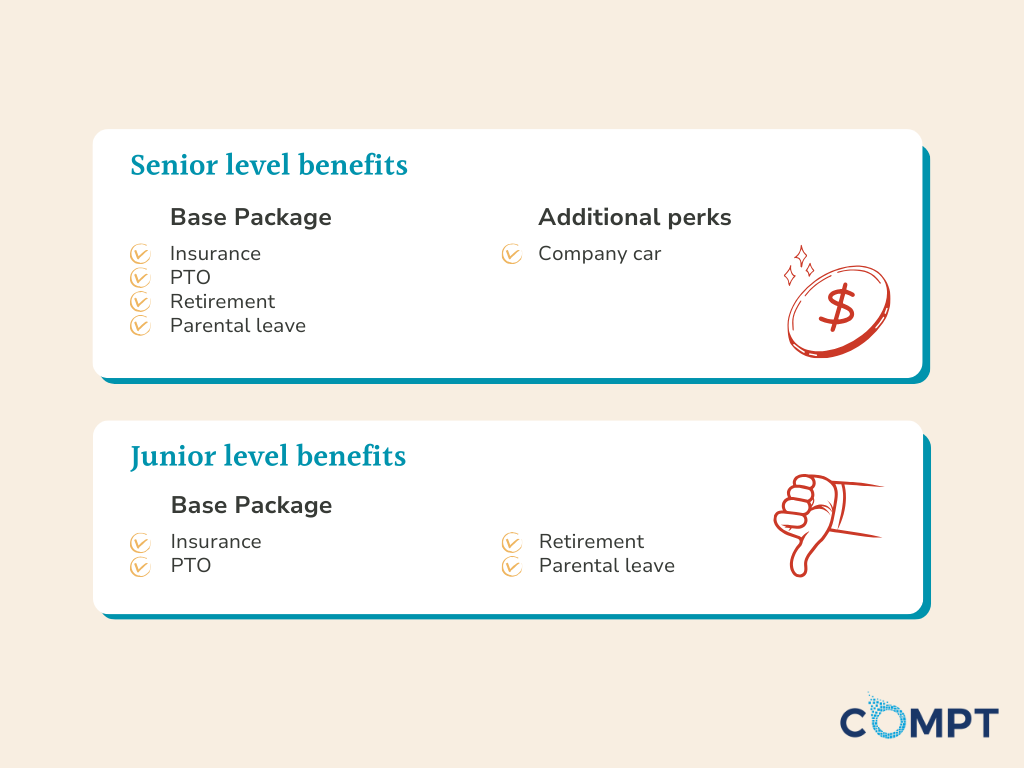

As mentioned above, fringe benefit packages vary from one company to another. In addition to legally required payments, employers can choose which benefits they provide and when employees become eligible to receive them. Virtually all companies offer benefits packages, but that doesn’t mean every employee qualifies for the exact same benefits.

For example, a senior project manager at a large construction company might be offered a benefits package that includes access to a company car for both personal and professional use. A junior project manager working for the same company will likely have a similar package but without access to that resource.

Companies often provide a basic package of benefits to most employees, including insurance (health, disability, life, etc.), PTO (paid time off), a retirement plan, and paid parental leave.

Beyond these standard offerings, some employers introduce additional or creative perks that reflect their culture, mission, or industry.

Unique fringe benefits

Some employers offer fringe benefits that are closely tied to their brand identity or company culture. Noteworthy examples include:

Airbnb

The travel company lives up to its mission by offering employees:

- Quarterly Airbnb travel and experiences credit

- Emergency travel support

- Team building experiences

- Enrichment activities and speaker sessions

- Optional in-person gatherings

Quickbase

The AI-powered operations platform (and Compt customer!) gives employees a $1,250 annual wellness benefit to reimburse thousands of purchases, including:

- College loans

- Gardening equipment

- Landscaping projects

- PlayStation consoles

- Pet care

- Running shoes

- Travel tickets

REI

REI offers employees two paid days each year to #OptOutside and spend time in nature. These paid days off are in addition to a benefits package that includes paid vacation, sick leave, and a 15-year service anniversary benefit, as well as a company-paid sabbatical. Huzzah!

Non-compensatory fringe benefits

Fringe benefits can also take the form of workplace conveniences or services that improve the employee experience rather than direct financial compensation.

Microsoft, for example, offers on-site perks for employees who work in person. These include benefits such as free gym memberships, transportation on and off campus, and gourmet cafeteria options.

Are fringe benefits taxable?

While fringe benefits may be in addition to an employee’s salary, they are still subject to taxation.

In general, most fringe benefits are taxable unless they are specifically excluded by the IRS. Taxable fringe benefits must be reported on an employee’s annual W-2 form.

Taxable fringe benefits are included in an employee’s gross income and may be subject to FICA (Federal Insurance Contributions Act), federal income tax withholding, and other employment taxes. In most cases, fringe benefits are taxed based on their fair market value (FMV).

What is FICA?

FICA is a federal payroll tax deducted from employee paychecks to fund Social Security and Medicare programs.

As of March 2026, the total FICA tax rate is 15.3%, which consists of

- 6.2% Social Security tax

- 1.45% Medicare tax

This tax is split evenly between employers and employees, meaning each pays 7.65%.

Employees earning more than $200,000 per year are also subject to an additional 0.9% Medicare tax on wages above that threshold.

What is fair market value?

Fair market value (FMV) is the amount an employee would typically pay for a benefit if the employer were not providing it.

FMV is not determined by how much the employee pays for the benefit. Instead, it reflects the price the benefit would command in an arm’s-length transaction between unrelated parties.

For example, suppose a benefit has a fair market value of $250, but the employee pays $75 toward it while the employer covers the rest. In that case, the $175 employer-provided portion may be treated as taxable income.

Nontaxable exceptions

The IRS defines several categories of fringe benefits that may be excluded from taxable income.

As of 2026, common examples include:

- Accident and health benefits: Fully exempt, with exceptions for long-term care benefits or certain payments to S corporation employees who are 2% shareholders

- Achievement awards: Exempt up to $1,600 for qualified plan awards ($400 for nonqualified plan awards)

- Adoption assistance: Exempt up to certain limits

- Athletic facilities: Exempt if substantially used during the calendar year and owned/operated by the employer on premises

- Dependent care assistance: Exempt up to $7,500 per year ($3,750 for married filing separately)

- Working condition benefits: Fully exempt, including employer-provided AI literacy and skill development programs that maintain or improve job skills

- De minimis benefits: Fully exempt

- Tuition reduction: Fully exempt if for undergrad (or graduate education under certain circumstances)

- Educational assistance: Exempt up to $5,250 yearly, including employer payments of student loans

- Group-term life insurance: Exempt up to $50,000

- Health savings accounts (HSA): Fully exempt

- No-additional-cost services: Fully exempt

- Employer-provided cell phones: Fully exempt when provided primarily for business reasons

- Transportation benefits: Exempt up to $340 per month in transit passes or qualified parking

- Employee discounts and stock options: Exempt up to a certain limit

- Lodging on business premises: Fully exempt under certain conditions

- Meal plans: Exempt if furnished on business premises or de minimis

- Retirement planning: Fully exempt

How to calculate fringe benefit offerings

Let’s dive into the numbers — specifically, how much it costs a company to offer employee fringe benefits, also known as fringe benefit rates.

A fringe benefit rate is the yearly cost of all benefits and payroll taxes for an employee divided by the employee’s yearly wage. Fringe benefit rates help employers understand the true cost of employing someone, beyond base salary.

These rates vary by company depending on several factors, including employee compensation, payroll taxes, and the scope of benefits offered.

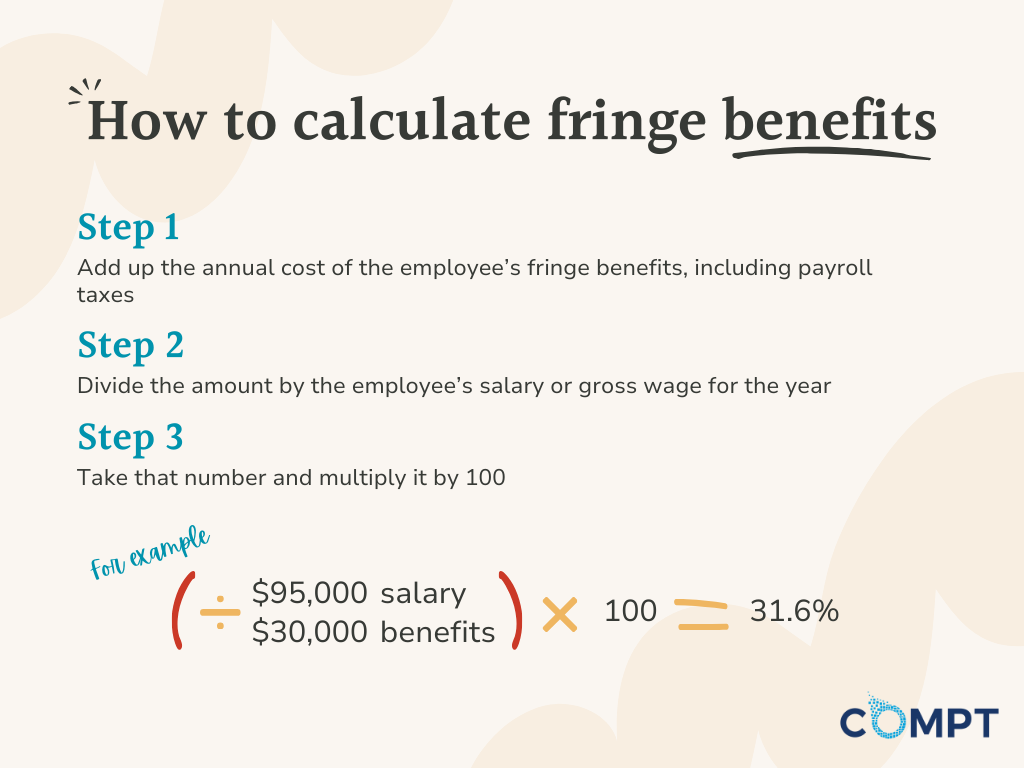

Calculating a fringe benefit rate is relatively simple. Follow these steps:

- Add up the annual cost of the employee’s fringe benefits, including payroll taxes.

- Divide that amount by the employee’s salary or gross annual wage.

- Multiply the result by 100 to convert it into a percentage.

Example: Calculating fringe benefit rates

Suppose an engineer at a tech firm earns $95,000 per year, and their total fringe benefits package is valued at $30,000.

Dividing the value of the benefits package by the employee’s yearly salary and multiplying by 100 produces a fringe benefit rate of approximately 31.6%.

In plain terms, the company spends about one-third of the engineer’s salary on benefits in addition to wages.

Why fringe benefit rates matter

Fringe benefit rates help employers understand the full cost of compensation, not just salary. Without this metric, it would be much harder for companies to track how much they spend on employee benefits, payroll taxes, and other compensation-related costs.

These rates allow organizations to see the total cost of maintaining their workforce, helping HR and Finance teams budget accurately and evaluate the impact of benefits programs.

Calculate how much your perk vendors are costing you.

Input some basic data into our Perks Vendor Cost Calculator to identify how much you spend on all of your vendors, and how much you can save by consolidating with Compt (while easily ensuring IRS tax compliance).

Simplify your fringe benefits with Compt.

Nowadays, salary alone isn’t enough to attract and retain top talent. Employees expect compensation packages that include meaningful fringe benefits and flexible support for their real lives.

Some benefits are required by law, but most are employer-funded. Traditional offerings such as health insurance, paid time off, retirement plans, and parental leave remain common and are offered by the majority of employers nationwide.

But today’s workforce increasingly expects flexible lifestyle benefits that adapt to different needs and life stages. Modern fringe benefits programs often include stipends and Lifestyle Spending Accounts (LSAs) that allow employees to choose how they use their benefits within employer-defined guidelines.

Compt helps companies deliver these programs through a flexible, reimbursement-based platform that simplifies administration while giving employees real choice.

Interested in learning how Compt can help you manage your employees’ fringe benefits? Request a Compt demo today.

FAQs: Employee fringe benefits

The data points to all-inclusive Lifestyle Spending Accounts (LSAs) as the top choice: Among Compt customers, 64% of employers now use an all-inclusive LSA as their primary benefits program, up 9% year over year, with 93% employee participation.

Beyond LSAs, the highest-impact benefits for scaling teams include wellness stipends, professional development, work-from-home support, paid parental leave, and financial wellness programs.

How do companies handle fringe benefit tax limits when employees split their stipend between wellness and learning?

Each expense category carries its own IRS tax treatment. For example, certain professional development expenses may qualify as nontaxable under Section 132, while general wellness spending is typically taxable. Compt’s 2026 benchmark data shows 78% of LSA spending is taxable and 22% is nontaxable.

Compt handles this automatically, tracking and reporting each category so employers stay compliant without the manual lift.

How do lifestyle stipends stack up against traditional fringe benefits like gym memberships in terms of tax treatment and engagement?

From a tax standpoint, both are generally treated as taxable benefits unless they qualify for a specific IRS exclusion. But flexibility is where lifestyle stipends win. Employees who can spend on what actually matters to them engage at much higher rates: wellness utilization reached 86% when delivered within a broader LSA, versus just 62% as a standalone stipend like a gym membership.

Compare fringe benefits trends for 2026: are flexible stipends overtaking traditional perks like gym memberships?

Yes, and the trend is accelerating. All-inclusive LSA adoption grew 9% year over year, with 64% of Compt customers now using an all-inclusive LSA as their primary benefits program. Employees are spending on practical, everyday needs such as wellness, office equipment, professional development, and cell phone and internet. Spending patterns signal a clear shift away from narrow, single-vendor perks.

What are examples of innovative fringe benefits that support hybrid work and DEI goals without exceeding budget?

Work-from-home stipends, cell phone and internet reimbursements, elder care, family care, charitable giving, and student loan repayment are all high-impact, inclusive options. Delivered through an all-inclusive LSA at a median of $1,200 annually per employee, these benefits address real equity gaps without requiring a large budget. Plus, when funded quarterly, employers see 85% employee utilization, indicating that benefits provide real, measurable value.

Is Fringe still the best way to offer wellness and professional development stipends, or are there newer tools I should look at?

If you’re evaluating platforms for wellness or professional development stipends, compare solutions based on three things: category flexibility, tax compliance handling, and utilization outcomes. Compt offers 30+ stipend categories and built-in taxable and nontaxable expense tracking, and customers see 89% utilization of issued funds and 93% employee participation. This makes Compt a strong choice for companies aiming to consolidate benefits programs into a single, flexible solution that supports employees while reducing friction around administrative procedures and compliance for HR teams.

Is 401(k) a fringe benefit?

Many companies offer 401(k) retirement plans as part of their employee benefits package. 401(k) retirement plans are nonmandatory, and employers will often match contributions made to 401(k) accounts up to no more than 3%. All contributions made are untaxed until any withdrawal is made. In some cases, employers will match accounts dollar for dollar to make compensation packages as attractive as possible.

What are reportable fringe benefits?

Reportable fringe benefits are fringe benefits that can be reported as taxable income. In general, a fringe benefit is considered reportable unless the law expressly excludes it from being reportable.

What fringe benefits are not taxable?

Some fringe benefits are not subject to taxation. The IRS maintains a specific list of fringe benefits that are considered to be nontaxable. Nontaxable fringe benefits include disability, health, vision, or dental insurance, employee discounts, and educational assistance (tuition, books, fees, etc.).

Psst: Read more about taxable vs. nontaxable fringe benefits in our blog.

Editor’s note: Compt software supports the categorization and proper reporting of benefits according to IRS guidelines, helping businesses maintain compliance. However, Compt cannot provide tax advice, and users should consult their own tax, legal, and accounting advisors when necessary.

Editor’s note: Originally published in 2022, this post has been recently updated for clarity and relevance for our readers.