Elder care employee benefits are employer-sponsored programs that help employees support aging family members through financial assistance, time off, flexibility, and care navigation tools.

As population aging increases worldwide, many employees in today’s workforce are juggling elder care responsibilities alongside their daily work.

The World Health Organization reports that the current pace of population aging is much faster than in the past, with the number of people aged 80 years or older expected to triple from 2020 to 2050, reaching 426 million.

Caring for elder family members comes with a heavy burden, and the impact of this shows up at work in several ways:

- Productivity loss: 67% of family caregivers struggle to balance their jobs with caregiving duties.

- Turnover: 16% of caregivers stopped working entirely and 13% changed employers to meet caregiving responsibilities.

- Stalled careers: 27% of working caregivers reduced their hours from full-time to part-time, and 16% turned down a promotion. Women, who shoulder the majority (55%) of elder care responsibilities, are more likely than men to drop out of the workforce or become underemployed because of their caregiving responsibilities.

- Bottom-line business metrics: Caregiving can cost employers $6,410 per employee per year in productivity loss.

Today, the business case for supporting families and caregivers across life stages has never been stronger. As the price of essentials such as groceries and costs for healthcare and childcare rise, employers are prioritizing benefits that offset everyday living costs. This includes elder care benefits as a means of providing purposeful relief for employees and their families.

What are elder care employee benefits?

Elder care employee benefits are workplace programs that support employees caring for aging family members. They can include financial support for caregiving costs and flexible work options, so employees can balance elder care responsibilities without sacrificing their careers.

Common examples of elder care employee benefits include caregiving stipends or Lifestyle Spending Accounts (LSAs), backup care programs, paid caregiving leave, Dependent Care FSAs (DCAPs), patient advocacy services, and flexible work arrangements.

Elder care can be offered as a standalone benefit, but many employers include it under a broader family and caregiving category or consolidate it into an all-inclusive Lifestyle Spending Account (LSA).

According to Compt’s 2026 Annual Lifestyle Benefits Benchmark Report, 64% of Compt customers offered an all-inclusive LSA in 2025, while 4% of customers offered caregiving and family-specific category stipends.

This approach is targeted by design, as employers aim to provide ad hoc support for care responsibilities rather than to drive broad participation. For example, an elder care benefits stipend may go unused until an employee needs it to cover emergency travel or in-home support following an elder relative’s hospital stay. On the other hand, a working parent who is part of the sandwich generation may need help with daycare one month, then transportation support for their aging parents the next.

In either scenario, the advantage of broad benefit categories and LSAs is that they can adapt as needs change. This provides greater support for employees and reduces operational complexity for program administrators.

What type of elder care benefits should employers offer?

While the specific benefits you’ll offer depend on your workforce needs, organization size, budget, and program structure, there’s a clear market preference for flexible benefits across all categories, including elder care.

Whether looped into an all-inclusive LSA or a standalone family and caregiving stipend, examples of elder care employee benefits typically include:

- Health insurance that includes elder care coverage

- Caregiving leave that goes above and beyond the scope of FMLA

- Dependent Care Assistance Plans (DCAPs)

- Backup care

- Flexible work arrangements

- Patient advocacy services

- Financial assistance (e.g., a caregiving stipend or an all-inclusive LSA)

Your benefits will depend on the unique needs of your workforce, but it’s important to understand the nuance of each offering and how leading companies structure their elder care benefits for maximum impact. Let’s take a look.

Health insurance that includes elder care coverage

While offering health insurance remains a legal requirement for employers with more than 50 full-time equivalent (FTE) employees, the scope expands into elder care if your plan allows participants to claim aging parents as dependents. The result for your employees could mean significant tax breaks, but there are certain criteria that must be met to qualify.

Another example of health insurance flexing as elder care benefits is when your plan includes coverage for services like home health care, outpatient rehabilitation, nursing homes, assisted living facilities, and adult day services. Financial relief in the form of coverage for these services can be hugely beneficial for employees caring for aging relatives.

Caregiving leave above and beyond the scope of FMLA

Under the Family and Medical Leave Act (FMLA), eligible employees can take up to 12 weeks of unpaid leave per year to care for a family member with a serious health condition. It’s an important protection, but it has significant limitations:

- Leave is unpaid (depending on the state in which you live).

- “Family member” is narrowly defined as parent, child, or spouse. Other close family members, including grandparents and in-laws, are not included.

- It applies only to companies with 50+ employees within a 75-mile radius.

- It doesn’t cover many caregiving duties, such as accompanying a parent to medical appointments.

- It only addresses employees who stop working to provide care, not those who manage care while still working

Since FMLA requires you to offer 12 weeks of unpaid leave per calendar year, you could start to build your caregiving leave benefits by offering more than 12 weeks per calendar year and paying for a portion of that leave.

Another consideration is to extend the benefits to any aging family member who lives with an employee, regardless of relationship, or even to those who do not live with the employee if the employee is a primary caretaker for that individual.

Dependent Care Assistance Plans (DCAPs)

A DCAP — often administered as a dependent care FSA — allows employees to contribute pre-tax dollars up to the IRS annual limit ($5,000 per household, or $2,500 if married filing separately) to pay for qualifying dependent care expenses.

It lets your employees set aside pre-tax money for qualifying elder care expenses, and as an employer, you can decide whether to match those contributions.

There are a few caveats for DCAPs and elder care employee benefits:

- DCAP salary contributions can’t exceed $5,000 per year (or $2,500 for married couples filing separately).

- Funds for child care and elder care can be used together, but they must share the annual $5,000 limit.

- This is a use-it-or-lose-it benefit; unspent funds do not roll over.

DCAPs are a solid pre-tax option, but they’re limited in scope. For employees with more complex caregiving needs or those in the sandwich generation, the $5,000 cap can be a constraint.

DCAPs are best for employees who can benefit from pre-tax savings and have predictable dependent care costs.

Backup care

Employer-sponsored backup care, like the program offered by Bright Horizons, gives employees access to vetted, last-minute care options when their usual arrangements fall through.

This is particularly valuable for working caregivers who can’t predict when their loved one’s needs will spike. Some vendors offer backup care as a standalone product; others integrate it into a broader caregiver support platform.

Backup care directly addresses one of the most common reasons caregiving employees miss work unexpectedly, and can greatly reduce caregiver stress, burnout, and turnover.

Flexible work arrangements

Flexibility is often the most immediately impactful and lowest-cost benefit to offer. These options typically include:

- Remote or hybrid working

- Flexible start and end times

- Compressed work weeks

- Part-time arrangements during emergency caregiving periods

Flexibility alone won’t solve the financial and mental burden of elder care, but when paired with other financial support, it can reduce the number of burned-out employees ready to jump ship.

Patient advocacy services

Patient advocates are healthcare experts who work on behalf of individuals to help navigate the complexities of the healthcare system. This includes:

- Managing appointments

- Coordinating care across providers

- Disputing insurance denials

- Decoding medical bills

They offer specialized support across a range of needs, and unlike hospital-based case managers, private patient advocates work solely in the patient’s best interest. For employees supporting aging parents or family members with complex medical needs, that expertise can be invaluable.

Some employers now offer private patient advocacy services as an employee benefit through providers such as Umbra Health Advocacy, which connects families with professional patient advocates who help navigate senior care, medical billing issues, insurance challenges, and transitions between care settings. Organizations can choose to fully cover these services, subsidize them, or provide employees access to discounted corporate rates.

For elder care in particular, these services can be especially accessible: Medicare covers certain patient advocacy services for eligible beneficiaries, and Umbra is one of the few providers offering Medicare-covered patient advocacy nationwide. That makes this a relatively low-cost, high-impact benefit employers can offer to support caregiving employees and their families.

Elder care stipends and Lifestyle Spending Accounts (LSAs)

For employers seeking greater flexibility, an elder care stipend embedded in an all-inclusive Lifestyle Spending Account offers a broader, more adaptable approach.

Unlike DCAPs, LSAs are employer-funded benefits without statutory IRS contribution caps. Instead, they are funded by the employer and are reimbursed through payroll with the appropriate tax treatment. LSAs can be designed to cover a wide range of caregiver expenses, including professional care services, transportation, respite care, or home modifications.

When evaluating platforms to administer these programs, HR teams should look for reimbursement-first workflows, policy controls, audit trails, exports or GL mapping for finance teams, and global readiness when managing elder care stipends alongside other benefits.

This is where employer-funded programs are increasingly headed. Compt’s 2026 Annual Lifestyle Benefits Benchmark Report found that the median annual funding across all company sizes for family and caregiving stipends is $2,500 per employee, with most programs ranging from $1,000 to $12,000 per year, depending on company size and structure.

Table: Select stipend funding ranges and trends, 2025–2026

| Stipend Category | Minimum | Median | Maximum |

|---|---|---|---|

| Family and Caregiving | $1,000 | $2,500 | $12,000 |

| All-Inclusive LSA | $50 | $1,200 | $33,000 |

| Professional Development | $50 | $800 | $10,000 |

| Wellness | $12 | $735 | $36,000 |

| Office Equipment | $100 | $250 | $2,400 |

Benchmarking data also shows that when elder care is folded into a broader family care benefit LSA rather than siloed as a standalone benefit, utilization rates tend to be significantly higher among Compt customers: 89% for all-inclusive LSAs compared to 46% for standalone caregiving and family stipends.

The key is designing benefits strategies that allow employees to engage more readily with a single, flexible benefit they can apply to their real lives, rather than navigating multiple fragmented programs.

Elder care stipends and LSAs are best for employers who want flexibility across caregiving needs and simpler administration.

How midmarket companies are bundling family care benefits today

Midmarket companies (typically 100–1,000 employees) are increasingly moving away from standalone elder care benefits and toward consolidated family care benefit programs and LSAs.

In practice, companies are refining existing programs to include child care, elder care, and general well-being with a well-defined family care or caregiving category. This gives employees the flexibility to spend where their needs actually are, and provides a few advantages to HR and Finance teams:

- Simpler administration and consolidated reporting

- Higher utilization rates because employees aren’t forced to choose between siloed benefits

- Easier to scale as workforce demographics shift

- More equitable across employee life stages — parents of young children and adult children caring for aging parents benefit from the same program

According to Compt’s 2026 Annual Lifestyle Benefits Benchmarking Report, midsize companies allocate $1,000–$1,200 per employee per year when offering family and caregiving as a standalone benefit, compared to $60–$12,000 per employee per year when bundling an all-inclusive LSA.

Here’s a step-by-step guide to building family and elder care benefits that match your organization’s priorities as well as employees’ lives.

1. Gather workforce data to identify employees’ real needs.

To find the right balance of family care and elder care benefits for your team, start by confirming that elder care support aligns with your workforce’s needs and your organization’s employee engagement and retention goals.

From there, review your employee’s demographic information. The U.S. Bureau of Labor Statistics (BLS) reports that of the 38.2 million people aged 15 and older providing unpaid elder care:

- Individuals ages 55 to 64 (24%) and 45 to 54 (19%) were the most likely to provide elder care, followed by those ages 65 and over (17%).

- The majority of these folks (55%) are women.

- Most (86%) of elder care providers who are parents are employed, and 72% are employed full-time.

This data shows that if you have employees aged 45 and over on your team, then you likely have caregivers. However, the best way to get the most accurate information is to conduct an employee benefits survey that asks about caregiving needs.

Questions like how many hours employees spend per week on caregiving, whether they also care for young children, and whether family members live with them can help you get a clear picture to inform benefits design.

2. Determine whether you’ll embed elder care benefits within a family care stipend or LSA.

Use your demographic and benefits survey data to inform how you’ll structure your elder care benefits (inside a broader family and caregiving stipend or an all-inclusive LSA).

LSAs are quickly becoming the norm, with 64% of Compt customers offering an all-inclusive LSA, and participation among active users reaching 93%.

With a model that allows employees to allocate funds across multiple caregiving or lifestyle categories, it’s easy to align your funding level with your intended outcome.

3. Set your budget and funding cadence

Today, 73% of employees have some form of caregiving responsibility. While many of those are likely childcare responsibilities, your employee benefits survey results should show you exactly how many folks are willing to disclose (and subsequently ask for assistance with) their elder care needs.

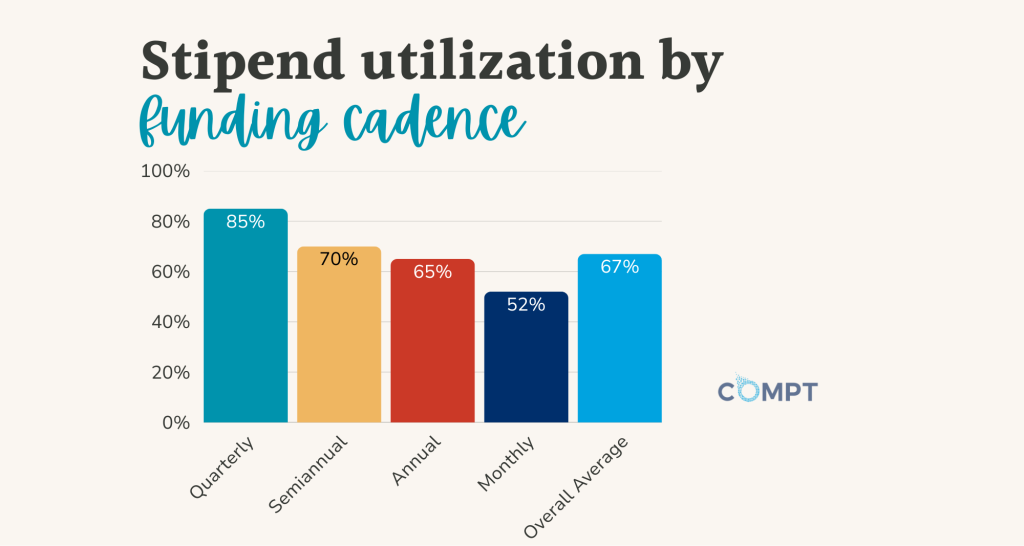

Use this information to set your budget and inform your funding cadence. Surprisingly, benefits strategies tend to focus on how much to offer, and sometimes skip the fact that when the money is offered is just as important:

- Quarterly-funded programs reached 85% utilization, compared to 52% for monthly funding and 65% for annual funding.

4. Identify which elder care, family, or caregiving expenses you’ll cover.

Whether you’ve chosen to offer elder care as part of a broader family and caregiving employee benefit or bundle it within an LSA, you’ll need to determine which expenses are covered. These might include patient advocates, backup care, transportation costs, meals, groceries, and more, depending on the needs of your employees.

5. Launch your elder care employee benefits.

Now you’re ready to implement your program manually or use a stipend or reimbursement platform like Compt!

If you plan to manage stipends manually, be sure to establish clear steps for collecting receipts, reviewing expenses, calculating taxes, and tracking balances.

With Compt, you can save time on administrative tasks while gaining real-time visibility into spending, seamless payroll integration, global currency support, and more. Compt also offers:

- 100% tax compliance: IRS and local tax rules are built in.

- No prefunding: You only pay for actual employee purchases.

- Personalization: Employees can choose what matters most to them, including childcare, elder care, wellness, and family planning, to name a few available stipends.

From here, encourage employees to use their elder care benefits. Try announcing the program with your internal communications team and highlight some of the data and labor statistics mentioned in this guide. Bonus points if you can tie this into real stories from some of your employees who will be impacted by this new offering.

Modernizing elder care employee benefits with Compt

Elder care employee benefits are a strategic investment in the retention, productivity, and well-being of the workforce, especially as population aging accelerates.

The companies that get this right aren’t necessarily offering the most expensive programs; they’re consolidating existing offerings into flexible, all-inclusive LSAs structured around how caregiving actually works. These programs are funded at a level that reflects their workforce’s real needs, and administered through platforms that make it easy for employees to access support without friction.

If you’re ready to evaluate what that looks like for your organization, start by assessing your current benefits against the ones outlined in this guide.

And if you’re looking for a platform that makes it easy to design and manage family and elder care benefits in one place, request a demo of Compt.

FAQs: Elder care employee benefits

Elder care employee benefits are employer-sponsored programs that support employees who are caring for aging family members. These benefits can include caregiving stipends or LSAs, paid caregiving leave, backup care services, flexible work arrangements, and access to elder care resources or counseling. Their goal is to help employees manage caregiving responsibilities without sacrificing their careers or financial stability.

How are midmarket companies bundling family care reimbursements into their broader employee benefits strategy?

Many midmarket companies bundle child care, elder care, and broader family support into a single flexible benefit program. This is often delivered through a LSA with a defined family care or caregiving category. Consolidating these benefits improves utilization, simplifies administration, and allows employees to spend benefit dollars on the type of care they actually need.

What are the best platforms for elder care Lifestyle Spending Accounts?

The best platforms for elder care Lifestyle Spending Accounts allow HR teams to define eligible caregiving expenses, set funding levels, and administer reimbursements in a tax-compliant way. Key features typically include reimbursement workflows, policy controls, payroll integration, audit trails, and reporting for HR and Finance teams. Compt is designed to manage these flexible benefits programs and support caregiving stipends alongside other lifestyle benefits. Learn more or book a demo here.

I need an employee benefits program that lets caregivers spend on elder care expenses. What are my options?

Employers typically choose between three approaches. A Dependent Care FSA (DCAP) allows employees to contribute pre-tax dollars up to $5,000 annually for qualifying care expenses. Employer-funded caregiving stipends reimburse approved elder care expenses. LSAs provide the most flexibility because employers define the funding level and eligible caregiving expenses, with reimbursements processed through payroll using the appropriate tax treatment.

Which platform would you recommend for managing caregiver and elder care benefits?

Organizations that want to manage caregiver and elder care benefits in one system typically use a flexible benefits administration platform such as Compt. These platforms allow HR teams to define eligible caregiving expenses, set funding levels, track utilization, and integrate reimbursements with payroll. Compt is designed specifically for managing lifestyle benefits, caregiving stipends, and LSAs in a single platform with built-in compliance controls.

How much do companies typically fund elder care benefits?

According to Compt’s 2026 Annual Lifestyle Benefits Benchmark Report, the median funding for family and caregiving stipends is $2,500 per employee per year. Most programs range from $1,000 to $12,000 annually depending on company size and program structure. Many organizations now include elder care within broader family care benefits or LSAs rather than offering it as a standalone stipend.

Editor’s note: Originally published in 2024, this post has been recently updated for clarity and relevance for our readers.