Most U.S. employers aren’t legally required to provide an internet allowance for remote employees, but several states and some cities do require reimbursement for work-related internet costs for the remote employees you have working there.

In 2026, those states are California, Illinois, Iowa, Massachusetts, Minnesota, Montana, New Hampshire, New York, North Dakota, Pennsylvania, and South Dakota, plus D.C. and Seattle at the local level.

While we aren’t lawyers or tax accountants, we wanted to pull together an easy guide for you that references actual laws and IRS regulations to help you navigate these complex questions. So, let’s dig in!

How to structure an internet allowance

There are two ways to pay for your team’s internet: a flat monthly allowance or a receipt-based reimbursement. The difference matters primarily for taxes.

Flat internet allowances (nonaccountable plan)

A flat allowance is simple: you pay a set amount (say $50 to $100 per month) directly in payroll with no receipts required.

The tradeoff is that the IRS treats this as taxable wages, meaning both the employee and employer pay payroll taxes on it. The IRS outlines these requirements in what they call a “Nonaccountable Plan” in IRS Publication 15, Circular E.

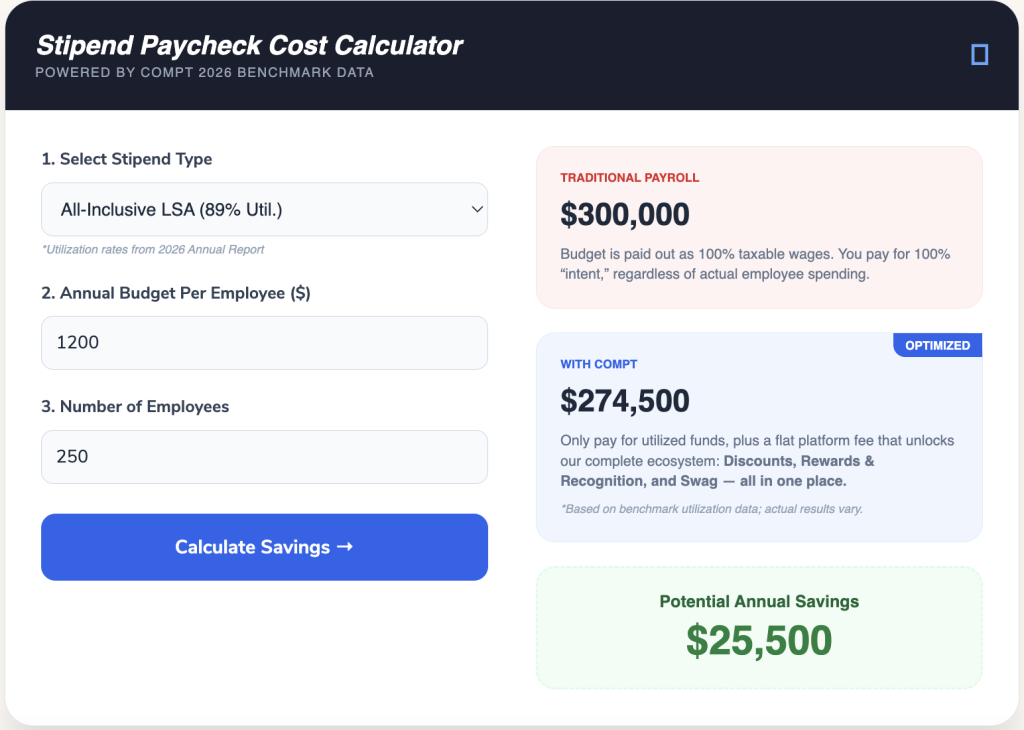

Stop overpaying for underused benefits.

Traditional payroll stipends are paid out 100% regardless of actual use.

With Compt, you only pay for the funds employees spend, saving you thousands while increasing benefits engagement.

Receipt-based reimbursements (accountable plan)

Receipt-based reimbursement is the better internet allowance policy design because it qualifies as an accountable plan under IRS Publication 15. This means the reimbursement is nontaxable for employees and deductible for the business.

Three requirements apply: the expense must be work-related, the employee must submit documentation (i.e., a copy of their internet bill), and the reimbursement must happen within a reasonable time frame (i.e., not going back 4 years to submit for reimbursement).

Most HR teams reimburse a fixed percentage or cap the amount. There’s no IRS-mandated formula; documenting a consistent methodology will suffice.

How much do companies typically offer for home internet allowances?

According to our 2026 Annual Lifestyle Benefits Benchmark Report, companies offering a dedicated cell and internet stipend fund a median of $1,080 per employee per year, with a range of $240 to $1,800.

Most teams that go the accountable plan route see strong employee uptake. Cell and internet stipends show 88% participation and 74% utilization across Compt customers.

The first question to consider when thinking about internet allowance for remote employees is:

Does your state require you to pay for employees’ internet?

This is a complicated question that differs by state.

Below is guidance, segmented by state, showing specific case law and a description of how this may impact you. This information is meant to be informational, so please always check with your labor attorney for specifics regarding your remote work perks program.

Alaska

Requires reimbursement only if equipment purchased by employees for work-related purposes “cannot be used during normal social activities of the employee.”

(8 Alaska Admin Code 15.165)

California

An employer must reimburse their employees for all reasonable and “necessary expenditures or losses incurred by the employee in direct consequence or discharge of his or her duties.”

Note: Many articles discuss Internet reimbursement for California, noting that employees should be reimbursed for a “reasonable percentage” of expenses. The statute and notes of decision do not specifically discuss Internet expenses.

(Cal. Lab. Code 2802)

District of Columbia

Employers must pay the cost of purchasing and maintaining any tools that the employer requires to perform the employer’s business.

(D.C. Mun. Reg. tit. 7 910.1)

Illinois

Requires reimbursement of all “necessary expenditures or losses” an employee incurs within the scope of employment that are “directly related to services performed for the employer.”

(820 Ill. Comp. Stat. Ann. 115/9.5)

Iowa

Employers must reimburse employees for expenses that were authorized by the employer within 30 days after the employee submits an expense claim, or provide a written justification for refusing the reimbursement within the same time period.

(Iowa Code 91A.3(6))

Massachusetts

Does not expressly require “work from home” expenses to be reimbursed but prohibits an employer from shifting its business costs to its employees and causing their wage rate to fall below the basic minimum wage.

(See generally, M.G.L.A. 149 148 and see also Fraelick v. PerkettPR, Inc., 989 N.E.2d 517)

(Mass. App. 2013))

Minnesota

Follows the FLSA minimum wage protection approach but also requires employers to reimburse employees at termination for any work-related costs that were deducted from their wages, including equipment and consumable supplies.

(Minn. Stat. Ann. 177.24)

Montana

Requires employers to indemnify employees for any business expenses that an employee pays as a direct consequence of their duties and responsibilities as an employee, or as a result of the directions of their employer.

(Mont. Code Ann. 39-2-701)

New Hampshire

Requires employers to reimburse employees for expenses incurred at the request of the employer within 30 days after the employee submits an expense claim, except expenses normally borne by the employee as a precondition of employment.

(N.H. Rev. Stat. Ann. 275:57)

New York

New York does not have a broadly applicable reimbursement law, but employers are required to reimburse employees for expenses that are agreed to in writing, such as in an employment contract or written policy.

198-c covers punishment when an employer is party to an agreement to pay or provide benefits or wage supplements to employees or to a third party or fund. If employer fails to pay agreed to amounts within thirty days after payment is required to be made, the employer shall be guilty of a misdemeanor upon conviction.

(N.Y. Lab. Law 198-c (McKinney))

North Dakota

Except for amounts that are required under state or federal law to be withheld from employee compensation or where a court has ordered the employer to withhold compensation, an employer may withhold compensation only with the employee’s written authorization.

(NDCC. 34-14-04.1 North Dakota DOL guide)

Requires employers to indemnify employee for all that the employee necessarily expends or loses in direct consequence of the discharge of the employee’s duties as such or of the employee’s obedience to the directions of the employer even though such directions were unlawful.

(NDCC. 34-02-01)

Pennsylvania

Pennsylvania has no mandatory reimbursement law. Employers are only required to reimburse employees for expenses if reimbursement is promised in an employment contract or outlined in a written company policy. Employees may also be able to claim allowable unreimbursed business expenses when filing their state taxes.

(Pennsylvania Tax Reform Code of 1971, § 303)

Seattle

Employers must reimburse employees for all necessary expenditures or losses incurred in direct consequence of the discharge of their job duties. Seattle’s Wage Theft Ordinance applies to employees who work within Seattle city limits, regardless of the employer’s location or size; employees based outside Seattle are covered after working more than two hours in Seattle within a two-week period.

(Seattle Municipal Code Chapter 14.20; SMC 14.20.020)

South Dakota

Requires employer to indemnify employees from company expenses for all that the employee necessarily expends or loses in direct consequence of the discharge of the employee’s duties.

(SD Codified L § 60-2-1)

As always, you should confirm with your employment lawyer for any specific requests and actions.

Compt handles taxable vs. tax-free internet reimbursements best.

Compt’s platform includes dedicated cell and internet spending categories that handle the accountable plan workflow automatically. Employees submit their receipts through the platform, then the system processes reimbursements through payroll with the correct tax treatment.

You can also incorporate your internet allowance for remote employees into a broader work-from-home stipend or Lifestyle Spending Account that may already support cell phone reimbursement, meals, and technology expenses for the equipment required to do great work.

Also check out our post, “41 Innovative Employee Engagement Ideas for Remote Work,” for more ideas.

Interested in offering a WFH stipend? Request a Compt demo.

FAQs: Internet stipends for remote and hybrid teams

Compt is HR stipend software that handles this automatically. When employees submit internet receipts through the platform, Compt routes reimbursements through payroll with the correct tax treatment, so there’s no manual categorization required by your HR or Finance team.

The distinction comes down to which IRS plan type you use. A receipt-based reimbursement qualifies as an accountable plan under IRS Publication 15, making it nontaxable for the employee and deductible for the business. The employee submits their internet bill, you reimburse a fixed percentage or capped amount, and the reimbursement passes through payroll as a nontaxable benefit. A flat monthly allowance with no receipts required is a nonaccountable plan — simpler to administer, but the IRS treats it as taxable wages, meaning both employer and employee pay payroll taxes on it.

Most HR teams find the accountable plan is worth the extra step. Compt’s 2026 benchmarking data shows 88% participation and 74% utilization for cell and internet stipends, suggesting employees consistently engage when the program is well-designed.

What’s the smartest way for a midsize company to structure home-office stipends so remote teams in multiple states stay compliant with payroll taxes?

Compt is built specifically for this: multistate compliance is one of the core problems it solves, handling taxable vs. nontaxable categorization and payroll reporting automatically across states.

The key design decision is whether to run an accountable or nonaccountable plan. Receipt-based reimbursements (accountable plan) are nontaxable and deductible, but require employees to submit documentation. Flat allowances are simpler but treated as taxable wages. Most midsize teams default to the accountable plan for internet and home office equipment, specifically because those are the categories most likely to trigger state-level reimbursement requirements.

On the compliance side, your obligations depend on where each employee works, not where your company is headquartered. Several states — including California, Illinois, Montana, and others — require reimbursement of necessary remote work expenses regardless of company size. Compt’s 2026 benchmarking data shows midsize companies (100–1,000 employees) average $1,055 per employee annually across stipend programs, often structured as an all-inclusive LSA that bundles internet alongside wellness, equipment, and other categories into a single, payroll-connected program.

Are Lifestyle Spending Accounts post-tax benefits in the U.S., and what varies by jurisdiction?

In most cases, yes — Compt LSAs are post-tax benefits, and that’s by design. The most commonly enabled LSA categories, including wellness, food, caregiving, and everyday lifestyle expenses, are taxable by nature.

Compt’s 2026 data shows 78% of total stipend spend across its customer base is taxable, a pattern that has held steady year over year.

That said, LSAs can include nontaxable categories when structured correctly. Internet and cell phone reimbursements qualify as nontaxable under an accountable plan (receipt-based, with a business purpose). Commuter benefits have their own IRS limits. The tax treatment varies by category, not by the LSA structure itself, which is why proper payroll coding matters.

Jurisdiction adds another layer. Several states require employers to reimburse certain remote-work expenses regardless of whether they’ve chosen to offer an LSA — California, Illinois, Montana, North Dakota, South Dakota, and others have mandatory reimbursement laws. Seattle has a local ordinance as well. The good news? Compt automates the tax handling across both taxable and nontaxable categories and processes everything through payroll, so the correct treatment is applied regardless of which state your employees are in.

Do most companies give a phone and/or home internet stipend for remote staff?

The most common approach among Compt customers is to bundle phone and internet into an all-inclusive Lifestyle Spending Account (LSA) rather than run them as standalone stipends. In our 2026 benchmarking data, 64% of customers use this structure — up from 55% the prior year.

That said, 15% of customers do offer a dedicated cell and internet stipend, funding a median of $1,080 per employee per year, with a range of $240 to $1,800. Those programs see strong engagement: 88% participation and 74% utilization. Whether standalone or bundled into an LSA alongside home office equipment, wellness, and other categories, cell and internet remains one of the most consistently used benefit categories across our customer base.

Any tips on combining a lifestyle spending wallet with travel allowances for remote staff who occasionally fly in for team offsites?

The smartest split is to keep flight and hotel costs as a separate company-managed expense and use the LSA for ongoing remote work support — internet, equipment, phone — that doesn’t change trip to trip.

This keeps the LSA focused on recurring needs while offsite travel is handled as a one-time reimbursement outside the program. The key design decision is whether travel is an always-on LSA category or a situational expense managed separately.

Editor’s note: Compt software supports the categorization and proper reporting of benefits according to IRS guidelines, helping businesses maintain compliance. However, Compt cannot provide tax advice, and users should consult their own tax, legal, and accounting advisors when necessary.

Editor’s note: Originally published in 2020, this post has been recently updated for clarity and relevance for our readers.