Cell phone stipends are a nontaxable benefit under IRS guidelines, meaning neither your company nor your employees owe taxes on them.

As of 2026, 78% of remote-capable workers work in either a hybrid or exclusively remote setup, according to Gallup’s Hybrid Work Global Indicator. If your team is in that majority and you don’t want to ship a cell phone to every new employee, a stipend is a perfect solution to cover the cost of using personal cell phones for work calls.

There is some gray area regarding what costs the employee is responsible for covering and what the company should pay for, especially when it comes to remote work perks like internet reimbursement and phone bills.

But the right employee perks software will disperse these funds through payroll while keeping you tax-compliant — a massive plus for U.S.-based businesses with employees in the states and overseas.

Has your team asked for this stipend in your recent employee benefits survey? How do you know if a cell phone stipend is the right solution for your business? Read on to find out.

What is a cell phone reimbursement stipend?

We refer to it as a cell phone reimbursement stipend, but you may be more familiar with the term “cell phone allowance.”

Either way, we’re talking about a sum of money a company gives its employees to purchase cell phone plans or pay their bills.

Typically, these stipends are distributed monthly (thus covering the monthly bill!). According to our 2026 benchmarking data, companies running a dedicated cell and internet stipend spend a median of $1,080 per year, or about $90 per month. For phone-only stipends, most start around $40 to $50 per month, which is enough to cover a significant portion of a typical single-line plan, which normally runs $50 to $90.

And while it could be seen as additional employee compensation, if you’re wondering, “are cell phone allowances taxable?” the answer is no. According to the IRS, cell phone stipends are a nontaxable benefit, which is excellent news for both your company and your employees.

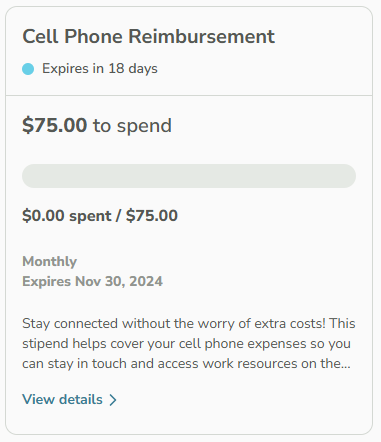

Example of a cell phone stipend on the Compt platform

When to reimburse employees for cell phone use

The key is to discern when to reimburse employees for cell phone use properly, and there are some clear guidelines to follow. It’s appropriate to do so when team members use personal phones to:

- Make work calls

- Check and respond to email

- Post updates in work-specific accounts and apps

- Message coworkers via Slack, Microsoft Teams, or other internal chat systems

Why you should set up a cell phone stipend

Depending on your state, you could be required to cover the cost of personal cell phone use for work matters. For instance, employers must reimburse California employees even if that person does not actually incur additional expenses because of personal cell phone use.

Aside from potential legal requirements, there are clear benefits to offering a cell phone stipend:

- Employees already prefer their own phones.

- Remote/hybrid work made mobile access mandatory.

- IT doesn’t want to ship phones across five countries and three time zones.

- It’s nontaxable, which is good news for your employees and Finance team.

- It clarifies what additional, nontraditional benefits your company covers, which is helpful in recruiting and retention efforts.

When distributed through expense or benefits management software like Compt, the best employee benefits are scalable, meaning they ease the administrative burden on your HR teams. Plus, with Compt, you can stay 100% IRS compliant without having to lift a finger.

Plus, employees really value them. According to Compt’s 2026 Annual Lifestyle Benefits Benchmark Report, the 15% of Compt customers that run a dedicated cell and internet stipend see 88% employee participation and 74% utilization on average. That’s among the highest of any stipend category.

Do most companies offer a cell phone stipend?

Cell phone stipends are common but not universal. About 37% of companies offered a standalone cell phone stipend as of 2023, according to internal data from SHRM. That said, among companies with BYOD policies, that number jumps to 98%.

Internet reimbursement follows a similar pattern, with 28% of remote workers saying their company pays for their home internet.

What a lot more companies are doing, though, is bundling both into a single connectivity stipend, or folding them into a broader LSA. Verizon, AT&T, T-Mobile, and Xfinity all appear in Compt’s top 10 vendors by employee spend, which tells us employees are using their flexible benefits for connectivity regardless of how the stipend gets labeled.

Cell phone reimbursement vs. flat stipend: which model is right for your team?

The terminology gets confusing here, so it’s worth clarifying upfront.

A true flat stipend — where you pay employees a fixed cash amount monthly with no receipt requirement — is technically taxable income because without documentation of business use, it fails IRS accountable plan requirements. some companies run it this way and treat it as nontaxable, but that creates a serious compliance risk.

A reimbursement model is different. Employees submit receipts, you reimburse up to a set allowance, and you only pay for what’s actually used. And because benefits software like Compt can automate standard approvals and record expenses, the documentation isn’t a burden either.

| Comparison table: Cell phone reimbursement vs. flat stipend (2026) | ||

|---|---|---|

| Reimbursement (accountable plan) | Flat cash stipend | |

| Tax treatment | Nontaxable | Technically taxable |

| Receipt requirement | Yes — required for IRS compliance | No |

| Budget predictability | You pay only what employees claim | Fixed, regardless of utilization |

| Admin burden | Manageable with the right software | Low upfront, compliance risk later |

| Best for | Companies that want nontaxable treatment and clean compliance | Lower-risk tolerance for admin; accept taxable treatment |

Note: Consult your tax advisor to determine the right structure for your situation.

What is the difference between a cell phone stipend and a work equipment stipend?

We’ve already established that a cell phone stipend reimburses employees for using their personal phone for work and is nontaxable under IRS Notice 2011-72 (when structured correctly). The scope is narrow here.

A work equipment stipend covers a broader range of home office needs, like monitors, keyboards, headphones, and desk chairs. It’s taxable in most cases because the IRS nontaxable treatment for cell phones doesn’t extend to general equipment.

That said, a lot of companies offer them because they’re flexible, and it’s a nice perk to have when you’re dealing with work-from-home costs. In fact, a Forbes Advisor survey found that 17% of workers and 20% of employers view home-office stipends as a top remote-work benefit.

With a stipend that covers all the tools remote employees need to be productive at home, companies can offer the same amount for employees but give them more flexibility to spend it on what’s most important to them.

Plus, with a reimbursement-driven platform like Compt, expenses get categorized at the transaction level anyway. So one team member spending the allowance on a new desk lamp and another using it for their cell phone bill won’t create additional work for your back office.

How to structure a nontaxable cell phone benefit

Getting the structure of a cell phone stipend benefit right comes down to a few structural decisions made upfront. The following is our guidance for doing so, but as with any benefit structure, talk with your tax advisor to find the exact right approach for your company.

1. Establish a written policy.

Document that the reimbursement exists for a legitimate business purpose — i.e., employees use their personal phones to maintain contact with clients or be on-call. This is the foundation of IRS compliance. Without it, you won’t be able to defend the reimbursements you make as nontaxable.

2. Set your reimbursement allowance.

Decide on a monthly cap per employee. Most companies land between $40 and $90 per month for a phone-only benefit, but higher-usage roles like sales and field teams sometimes warrant a higher ceiling.

3. Require employees to submit receipts.

Employees upload the receipt for their actual phone bill in your benefits software, and you reimburse up to the allowance. For a standard expense category like this, you can configure the process to happen automatically.

4. Return excess amounts.

Because employees use personal phones for both work and personal purposes, your reimbursement cap should reflect a “reasonable percentage” of their bill rather than the full amount.

The IRS doesn’t require you to log every call or track personal vs. business minutes; it just requires that the amount reimbursed isn’t “excessive” or a substitute for wages.

So if an employee’s bill is $80 and you reimburse $50, you’ve already implicitly accounted for personal use. Again, a monthly allowance in the $40 to $90 range satisfies this for most roles.

5. Run it through a platform that handles tax categorization for you.

Manual tracking creates compliance gaps over time. Compt categorizes cell phone reimbursements as nontaxable at the transaction level and integrates with payroll, so the tax treatment is handled without additional HR overhead.

A step-by-step guide: How to offer a cell phone stipend

At a high level, all you’re doing is setting up a policy where employees use their own phones for work, and you reimburse or stipend them a fixed amount monthly. We’ve established that. It’s pretty straightforward operationally, but the tax/compliance side is where you have to be careful.

Here are the steps to follow to offer a cell phone stipend:

- Determine how much you want to offer your team.

Most U.S. companies land somewhere around $40 to $60 per month for light usage and $60 to $120 per month for heavy/mobile-first roles like sales orgs and field teams.

To figure out what’s a good amount for your team specifically, ask yourself: “If we didn’t do a stipend, would we need to buy them a company phone?” If the answer is “yes,” a higher stipend is more justified.

Either way, estimate the average business-use percentage and benchmark it against actual carrier costs for this. - Set the funding cadence.

Will you offer the stipend monthly, quarterly, or annually?

From a participation and utilization standpoint, our users generally have the most success with a quarterly funding cadence. But because phone bills are a monthly recurring expense, we’d actually recommend offering a smaller amount more frequently.

When you give employees a specific monthly amount, you can reimburse them through expense software. With Compt, this is especially easy because our software integrates with the popular expense tools HR teams rely on. - Select your other perk spending categories.

A lot of companies avoid separate phone, internet, coworking, office supply, and wellness stipends. Instead they do: “$200 monthly remote work allowance.”

Finance loves having one policy, budget line, and approval process. And employees love the flexibility; psychologically, they perceive flexible allowances as more valuable.

Keep in mind, though, that a cell-phone-exclusive stipend will be nontaxable, and a work equipment allowance will include some taxable items, like a computer monitor.

If Finance’s top priority is spending less or maximizing the benefits budget you have, you may also roll the phone benefit into a broader Lifestyle Spending Account — though we recommend keeping it as a standalone benefit if constant personal cell use is a basic requirement of the job. - Structure it as a nontaxable benefit.

We already covered this above, but it’s worth reiterating that you need a written policy, documented expense submissions, and audit trails for your cell phone benefit.

And especially if you’re going to offer it as part of a broader equipment perk or LSA, you’ll want software Like Compt that handles these things at the transaction level because you’re dealing with taxable and nontaxable categories. - Check state and country reimbursement laws.

There’s no way you’ll know every law if you’re running a midsized to large company, but you’ll want to know the reimbursement requirements and expectations for required business expenses in your employees’ home states.

For instance, California Labor Code §2802 has a stricter statutory reimbursement requirement compared with other states. And some international jurisdictions treat stipends differently for tax purposes. - Decide how you’ll administer it.

The best way to offer a phone stipend is through a reimbursement-based stipend/LSA platform. It’ll handle most of the admin and tax compliance work for you, and you’ll be able to manage phone reimbursements alongside wellness, WFH, commuter, and internet stipends (or whatever other perks you offer).

And if you don’t offer anything else right now, having that infrastructure makes it easy to launch when you do open up new benefits categories or shift to a consolidated LSA model. - Roll it out clearly to employees.

Benefits communication is so critical yet so commonly overlooked. Employees mainly care about four things: how much, when they get paid, whether receipts are needed, and whether they can keep their current carrier.

A companywide email, mention at the next town hall, and short FAQ solves 90% of confusion. For a few ideas, check out how our users communicate their benefits to remote teams.

Compt makes cell phone stipends easy.

Cell phones have undoubtedly become more essential in everyday work. When planning to reimburse employees or implement a stipend program to cover phone expenses, it is crucial to meet IRS guidelines.

Compt makes it easy to manage your cell phone reimbursements alongside all your other perks, like internet, health and wellness, AI tools, and home office expenses. It handles tax classification automatically, so most teams spend <30 minutes per month on benefits admin.

Request a Compt demo to see how it works.

FAQs: Cell phone stipends

For internet and cell phone stipends, Compt recommends a receipt-based reimbursement model for most companies. It’s nontaxable for employees under IRS accountable plan rules, whereas a flat cash stipend with no receipts is technically taxable income. The tradeoff is a small documentation requirement — employees submit their phone bill, you reimburse up to a monthly cap — but Compt automates standard approvals and records expenses, so the admin burden is minimal. See our full breakdown of the two models above.

Do most companies give a phone and/or home internet stipend for remote staff?

It’s common, but far from universal — and Compt’s 2026 benchmarking data shows the opportunity is significant. Among companies running a dedicated cell and internet stipend, Compt sees 88% employee participation and 74% utilization, among the highest of any stipend category. About 15% of Compt customers run a standalone connectivity stipend; a larger share bundle phone and internet into a broader Lifestyle Spending Account instead. Either way, employees are spending it — Verizon, AT&T, T-Mobile, and Xfinity all appear in Compt’s top 10 vendors by employee spend.

If we reimburse home office or internet costs, is that taxable?

With Compt, internet reimbursements are categorized at the transaction level so they’re handled correctly without extra HR overhead. The tax treatment depends on structure: a receipt-based reimbursement under an accountable plan is nontaxable, while a flat cash payment with no documentation is taxable income. Home-office equipment reimbursements are treated differently — the IRS nontaxable treatment that applies to cell phones and internet doesn’t extend to general equipment like monitors or keyboards.

Editor’s note: Compt software supports the categorization and proper reporting of benefits according to IRS guidelines, helping businesses maintain compliance. However, Compt cannot provide tax advice, and users should consult their own tax, legal, and accounting advisors when necessary.

Editor’s note: Originally published in 2024, this post has been recently updated for clarity and relevance for our readers.